What if your "diversified" portfolio is actually just a cluttered drawer of mismatched financial tools? Many Singaporeans find themselves holding a collection of products rather than a unified strategy. It's easy to feel uneasy as you watch T-bill yields drop to 1.5% and wonder how global shifts affect your local assets. If you're worried about market drawdowns hitting your retirement timeline, you're not alone. A professional investment portfolio review Singapore can help you turn that uncertainty into a clear, strategic roadmap for your future.

We'll show you exactly how to realign your assets with your 2026 goals through a professional audit. You'll learn how a financial consultant can help you optimise tax efficiency using your SRS and CPF accounts. We'll also explore how frameworks like i12 investments provide the stability you need to grow your wealth with confidence. It's time to stop guessing and start building a portfolio that works as hard as you do. Let's look at how to transform your financial "collection" into a high-performing wealth engine.

Key Takeaways

- Understand why 2026 economic shifts, such as easing inflation, require a fresh look at your current assets.

- Learn how a professional investment portfolio review Singapore helps you stress-test your CPF, SRS, and private holdings against potential market shocks.

- Discover how the i12 investments framework provides a structured approach to gaining diversified global exposure.

- Identify common pitfalls like over-concentration in local property and ensure your wealth protection remains robust.

- See how partnering with a financial consultant shifts your focus from buying products to following a unified strategic roadmap.

Why an Investment Portfolio Review in Singapore is Essential for 2026

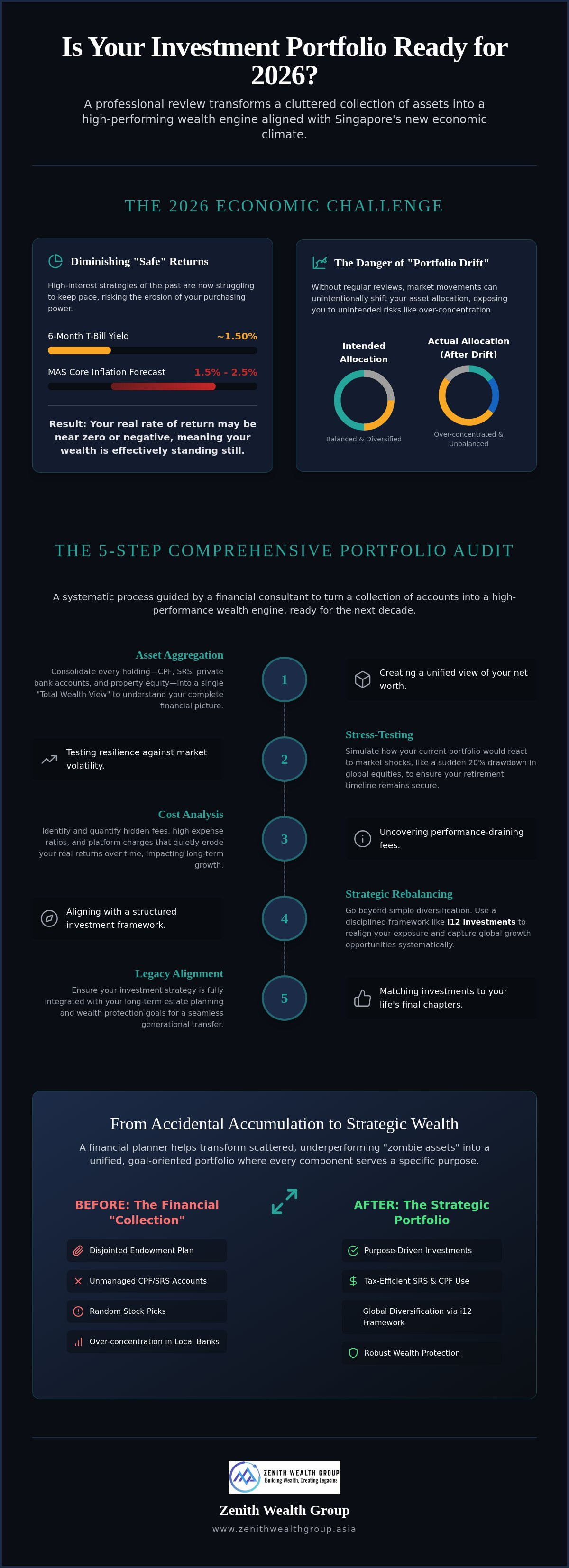

The financial environment moves fast. What worked for your savings in 2023 might be holding you back in 2026. Back then, high interest rates made cash and T-bills an easy win. Today, with 6-month T-bill yields sitting around 1.50%, that "safe" strategy is barely keeping pace with the MAS inflation forecast of 1.5% to 2.5%. This shift is exactly why an investment portfolio review Singapore is no longer optional; it's a necessity for wealth preservation. If you don't adjust your sails, you'll likely find your retirement timeline drifting further away.

Many investors suffer from "portfolio drift." This happens when your asset allocation shifts over time without you noticing. Perhaps your Singapore bank stocks or REITs have become a larger portion of your net worth than you intended. Without a regular audit, you're following an outdated map. A financial consultant can help you apply the principles of Modern Portfolio Theory to ensure your risk levels match your current life stage, not your past one. It's about being proactive rather than reactive to global trade shifts and exchange rate volatility.

The 2026 Economic Backdrop for SG Investors

The current climate is defined by cooling inflation and shifting central bank policies. While lower rates can boost REIT valuations, they also squeeze the margins of local banks. If your portfolio is heavily weighted toward the "Big Three" local banks, you might be exposed to more sector-specific risk than you realize. Inflation still erodes your purchasing power. If your real rate of return isn't exceeding the core inflation rate of 1.4%, you're effectively standing still. To counter this, many are turning to the i12 investments framework. It provides a structured, disciplined response to market volatility, moving beyond simple diversification into true strategic allocation.

From Accidental Accumulation to Strategic Wealth

Most people don't build a portfolio; they collect one. You might have a random endowment plan from a decade ago, a few stocks recommended by a friend, and your CPF accounts. These "zombie" assets often sit in your account without a clear purpose. The cost of inaction is high. Every dollar sitting in an underperforming asset is a dollar not working toward your retirement. A review helps you see these fragments as a single engine. A financial planner ensures every component, from your SRS contributions to global equities, serves a specific goal. Don't let your wealth grow by accident. If you're ready to move from a collection of products to a unified plan, start your strategic review today.

The 5-Step Framework for a Comprehensive Portfolio Audit

Performing a thorough investment portfolio review Singapore requires a systematic approach. It's not just about looking at your bank statements. It's about understanding how every component of your wealth interacts. You need a process that turns a collection of accounts into a high-performance wealth engine. Follow this five-step framework to ensure your strategy is ready for the second half of the decade.

- Step 1: Asset Aggregation. Bring together every account, from your CPF and SRS to your private bank holdings and property equity.

- Step 2: Stress-Testing. Simulate how your current holdings react to market shocks, such as a sudden 20% drawdown in global equities.

- Step 3: Cost Analysis. Identify hidden fees, high expense ratios, and platform charges that quietly erode your real returns.

- Step 4: Rebalancing. Use the i12 investments methodology to realign your exposure with global growth opportunities.

- Step 5: Legacy Alignment. Ensure your investment strategy matches your estate planning and wealth protection targets.

Consolidating Your Singaporean Asset Base

Most Singaporeans have wealth scattered across different buckets. You likely have a CPF Ordinary Account earning 2.5% and a Special Account at 4%. You might also have an SRS account used for tax relief. When you apply a professional investment management lens, you see these as part of one ecosystem. Total Wealth View is the combined perspective of your liquid cash, tradable securities, and illiquid assets like property or CPF LIFE. Seeing the full picture helps you avoid doubling down on the same risks across different accounts. If you're unsure how these pieces fit together, a financial planner can help you map out your entire net worth.

Stress-Testing for the Modern Era

Your portfolio might look good during a bull market, but how does it behave when things go wrong? Just as the Monetary Authority of Singapore prioritizes resilience in official foreign reserves management, your personal wealth needs a safety buffer. A 20% market drawdown shouldn't derail your retirement timeline. We look at liquidity to ensure you don't have to sell assets at a loss during an emergency. This level of simulation is complex. It's why many choose to connect with a professional to run these scenarios. A financial consultant provides the objective data you need to stay calm when volatility strikes. Don't wait for a market crash to find out if your strategy is robust.

Integrating i12 Investments into Your Strategic Wealth Plan

Once you've completed your investment portfolio review Singapore, the next step is implementation. This is where the i12 investments framework comes into play. It isn't just a list of stocks. It's a core philosophy built on the idea that wealth needs both a solid foundation and the agility to capture growth. While simple index tracking has its place, it often leaves Singaporean families over-exposed to local sectors or trailing behind during rapid market shifts. The i12 approach provides a more nuanced way to manage your money.

We use a "Core and Satellite" structure. Your core holdings provide the stability needed for long-term endurance. These are often global leaders with proven track records. The satellite portion allows for targeted exposure to high-growth areas. This balance ensures you aren't just betting on the status quo but actively participating in the future of the global economy. It's a disciplined way to ensure your portfolio doesn't just grow, but stays resilient.

The Anatomy of an i12 Investments Strategy

Success in 2026 requires moving beyond the traditional Singaporean "home bias." While local banks like DBS or OCBC are stable, relying on them for your entire growth engine is risky. The i12 investments framework pushes your boundaries into global technology and healthcare sectors. These areas often provide the innovation-led returns that local property markets can't match. We also look at geography. By balancing holdings across the US and China, you can better manage the trade tensions that often impact local asset valuations. This regional diversification acts as a shield during localized downturns.

Customising i12 for Your Life Stage

Your strategy must evolve as you do. For young professionals, i12 investments focuses on aggressive capital appreciation. You have time on your side, so we lean into growth-oriented satellites. For pre-retirees, the focus shifts. We move toward income generation and protecting the capital you've spent decades building. This is a critical part of how retirement planning singapore works in practice. It's about ensuring your "core" is large enough to sustain your lifestyle without forcing you to sell assets during a market dip. A financial consultant can help you calibrate these weights to match your specific timeline and risk tolerance.

Avoiding the 'Home Bias' and Other Common Portfolio Mistakes

Familiarity feels safe, but it's often a trap for your wealth. Many investors in Singapore fall into the habit of over-allocating to what they see every day. A comprehensive investment portfolio review Singapore often uncovers a heavy lean toward local bank stocks and residential property. While these assets have served many well in the past, relying on them too heavily creates a structural weakness in your strategy. You're betting your entire future on a single, small geography.

Investing without a safety net is another frequent error. Some view insurance as a separate expense rather than a core component of their wealth strategy. This is a mistake. Without adequate wealth protection, a single health crisis or legal issue can wipe out years of disciplined investing. Don't let the "Sunk Cost" fallacy keep you tied to underperforming legacy policies either. If a plan no longer fits your 2026 goals, it's time to pivot. A financial planner can help you identify these "zombie" policies and redirect those funds into more productive frameworks like i12 investments.

Diversifying Beyond the Little Red Dot

Global diversification is often called the only "free lunch" in the investing world. It allows you to capture growth in sectors that don't exist in Singapore, like global AI development or innovative biotech. Research indicates that over-concentrating in local markets, or 'Home Bias', can reduce long-term returns by up to 2% annually when compared to a more balanced global approach. You also have to manage currency risk. While a strong SGD is great for purchasing power, it can impact your returns on foreign holdings. Using the i12 investments framework helps you navigate these shifts by balancing geographical exposure with currency considerations. This is why an investment portfolio review Singapore must look beyond our borders to find true resilience.

The Intersection of Investment and Legacy

Your portfolio doesn't exist in a vacuum; it's the engine for your family's future. This is why your review must include legacy planning. It's not enough to grow your wealth; you must ensure it reaches the right people. Check your CPF nominations and private account beneficiaries regularly. Simple administrative oversights can lead to lengthy legal delays for your loved ones. A financial consultant acts as a partner to ensure your investment strategy and estate plans are perfectly aligned. They provide the emotional discipline needed to stay the course while ensuring your transition of wealth is seamless. Ready to fix the gaps in your strategy? Contact us to audit your current holdings and build a more robust plan.

Optimising Your Future: How a Financial Consultant Refines Your Strategy

A professional investment portfolio review Singapore is about more than just numbers on a screen. It's the difference between buying a product and building a future. In the past, the industry often felt like a series of disconnected transactions. Today, the shift toward comprehensive planning and fee-based advice puts your goals first. Your financial consultant acts as a strategic partner, not just a salesperson. This relationship ensures your wealth is managed with your specific retirement or legacy targets at the center of every decision.

Market volatility is inevitable. When global markets dip, it's easy to make emotional decisions that damage your long-term returns. This is where professional guidance becomes invaluable. A financial planner provides the emotional discipline needed to stay the course. They help you look past the daily headlines and focus on the robust frameworks like i12 investments that you've put in place. It's about having a steady hand on the wheel when the economic weather gets rough. You don't have to navigate these shifts alone.

The Value of Independent-Minded Advice

As authorized representatives of finexis advisory, we offer a broader range of solutions than a single-bank representative could. We aren't tied to one set of proprietary products. Instead, we use professional tools and calculators to solve complex problems like education funding. We also help you establish a regular review cadence. For most families, an annual check-in is sufficient. However, if your life situation changes quickly, a quarterly pulse check might be better. This ensures your strategy stays as dynamic as the 2026 market itself.

Ready to Secure Your 2026 Roadmap?

Starting your first professional review is simple. You'll need to gather your latest CPF statements, SRS account details, and any private insurance or investment documents. We'll help you set realistic expectations for growth. While everyone wants high returns, we prioritize wealth preservation and tax efficiency too. Don't let another year pass with an unoptimised "collection" of assets. It's time to turn those fragments into a unified plan. You can connect with a financial consultant at Zenith Wealth to start your investment portfolio review Singapore today. Let's build a roadmap that actually gets you where you want to go.

Build Your Future on a Solid Strategic Foundation

Your wealth shouldn't be left to chance. By addressing the portfolio drift we've discussed and moving beyond the familiar safety of local bank stocks, you're securing a more resilient future. A professional investment portfolio review Singapore is the first step toward turning those fragmented assets into a unified wealth engine. We've explored how a holistic approach, combined with the i12 investments framework, provides the global reach necessary for the 2026 market. It's about moving from accidental accumulation to a disciplined, goal-oriented strategy.

As authorised representatives of finexis advisory, we bring a 5-pillar wealth approach to every conversation. Our goal is to serve as your proactive partner, helping you navigate market volatility with quiet confidence. Don't let your retirement timeline be dictated by market drawdowns or stagnant yields. It's time to take control of your financial roadmap and build a strategy that grows alongside you. We invite you to start this conversation and discover the difference that strategic, human-centered planning makes for your generational wealth.

Book Your 2026 Portfolio Strategy Session with Zenith Wealth

Frequently Asked Questions

How often should I conduct an investment portfolio review in Singapore?

You should conduct an investment portfolio review Singapore at least once a year. Regular check-ins ensure your strategy stays aligned with shifting market conditions, such as the cooling inflation and lower interest rates seen in 2026. Major life events like marriage, a career change, or receiving an inheritance also trigger the need for an immediate review. This proactive approach helps you catch "portfolio drift" before it impacts your long-term wealth goals.

Is it better to use a robo-advisor or a financial consultant for my review?

A financial consultant offers a personalized, holistic view that robo-advisors simply cannot match. While robos use algorithms for basic asset allocation, a consultant integrates complex factors like legacy planning and tax efficiency into your plan. They provide the emotional discipline needed during market volatility. This human touch is vital when navigating sophisticated frameworks like i12 investments to ensure every part of your financial life works together seamlessly.

How do I incorporate my CPF and SRS accounts into a portfolio review?

Treat your CPF and SRS accounts as core components of your total asset allocation rather than separate buckets. During a review, we analyze your CPF Ordinary Account and Special Account balances alongside private investments to avoid over-concentration in local sectors. Optimizing your SRS contributions can also provide significant tax relief while funding your future. A unified view prevents you from taking too much or too little risk across your entire wealth ecosystem.

What are the common fees associated with a professional investment review?

Professional review fees vary depending on the complexity of your holdings and the specific level of service you require. Many modern firms are transitioning from commission-based models to transparent, fee-based strategic planning. This shift ensures your financial planner prioritizes your long-term goals over specific product sales. Always ask for a clear breakdown of platform fees, fund management costs, and advisory charges before you begin your review session.

Can a portfolio review help me reduce my income tax in Singapore?

Yes, a strategic investment portfolio review Singapore can help lower your tax bill through targeted retirement contributions. By maximizing your Supplementary Retirement Scheme (SRS) contributions and making voluntary CPF top-ups, you can reduce your chargeable income. For the Year of Assessment 2026, resident tax rates are progressive and go up to 24%. A consultant helps you navigate these brackets to keep more of your wealth working for you.

How does the i12 investments framework differ from traditional asset allocation?

The i12 investments framework moves beyond simple asset diversification by using a structured core-satellite approach. Traditional allocation often relies on static percentages of stocks and bonds that may not adapt to global shifts. In contrast, i12 focuses on capturing growth through targeted satellites while maintaining a resilient, stable core. This approach allows for more agility in the 2026 economy, helping you navigate sector-specific shifts that traditional models often overlook.

What should I do if my portfolio review reveals a significant shortfall in my retirement goals?

Don't panic if a review reveals a shortfall; use the data as a catalyst for immediate adjustment. You might need to recalibrate your retirement age, increase your monthly contributions, or shift toward higher-growth assets within the i12 investments framework. A financial consultant helps you run "what-if" scenarios to find a viable path forward. Identifying a gap early gives you the time needed to make meaningful changes to your roadmap.

Is a portfolio review necessary if I only invest in low-risk Singapore Savings Bonds?

A review is essential even if you only hold low-risk assets like Singapore Savings Bonds. While SSBs are secure, their 10-year average return of 2.06% might not beat inflation or meet your specific long-term needs. A review helps you evaluate the opportunity cost of being too conservative with your capital. It ensures you have the right balance of safety and growth to protect your purchasing power over several decades.