What if your CPF wasn't just a mandatory savings account, but the most powerful engine in your wealth strategy? With the 2026 Ordinary Wage ceiling now at $8,000, maximizing CPF for retirement in Singapore has become a more complex, yet rewarding, puzzle to solve. Many people feel a sense of unease as they watch the Enhanced Retirement Sum climb to $440,800. It's natural to worry about outliving your savings in an expensive city, especially with shifting limits and rising healthcare costs.

We understand these concerns. You want a retirement that feels like a reward, not a budget constraint. This guide promises to clear the confusion. You'll discover expert strategies to optimize your accounts and integrate them with private assets like i12 investments for a secure future. We provide a clear roadmap for your top-ups and show you how a financial planner helps you build a diversified portfolio. Let's explore how to turn these 2026 updates into your greatest financial advantage.

Key Takeaways

- Navigate the 2026 shift in Enhanced Retirement Sum (ERS) limits to ensure your savings stay ahead of rising costs.

- Master the "January 1st" rule and strategic OA-to-SA transfers to lock in higher interest rates early in your career.

- Develop a life-stage roadmap for maximizing CPF for retirement in Singapore, tailored for every decade of your working life.

- Learn to integrate CPF LIFE as a secure income floor while using i12 investments as a growth engine for your portfolio.

- Understand how a financial planner provides the bespoke advice needed to bridge the gap between government schemes and private wealth.

The 2026 Landscape: Why Maximizing CPF for Retirement in Singapore is Changing

The rules for your golden years are shifting. In 2026, the strategy for maximizing CPF for retirement in Singapore is no longer a "set and forget" task. It's a multi-layered approach. You need to look at cash top-ups, account transfers, and precise timing. The Central Provident Fund (CPF) system remains your foundation, but the floor is moving higher. Maximization now requires a proactive stance to ensure your savings don't just exist, but actively thrive.

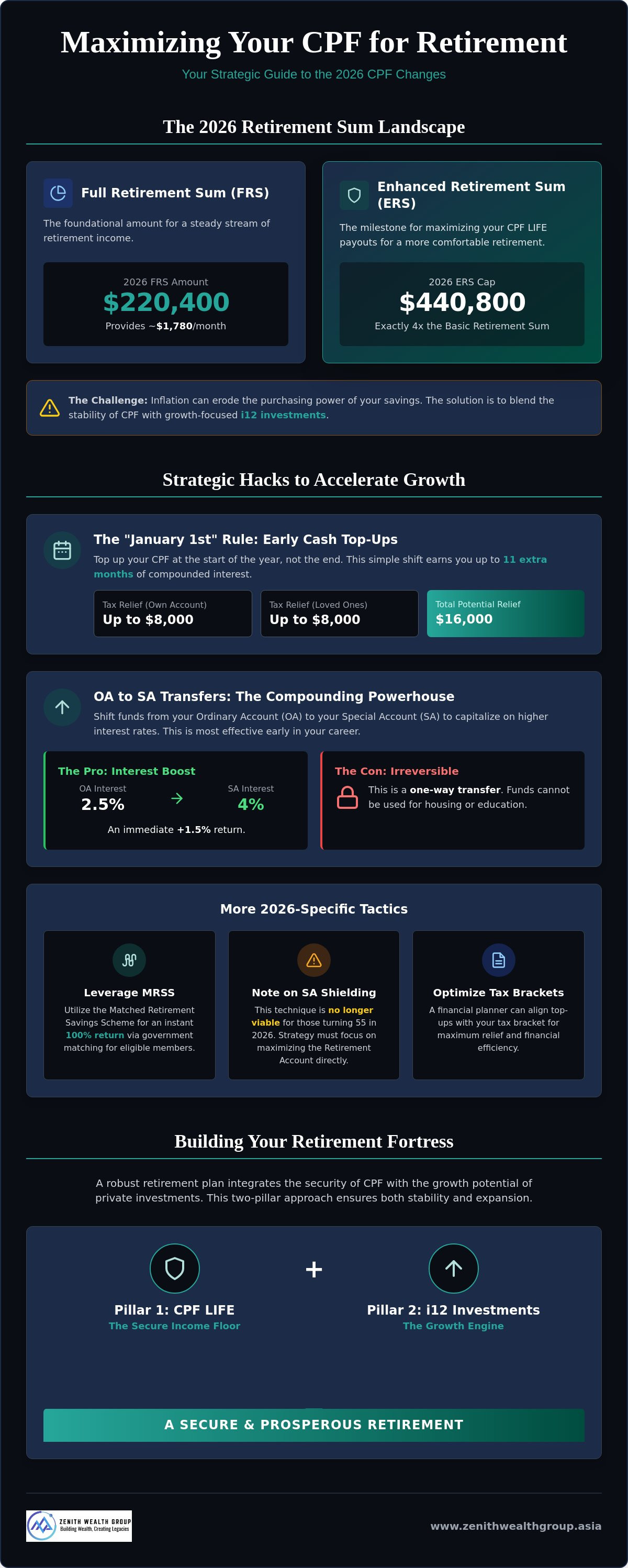

For those turning 55 in 2026, the Full Retirement Sum (FRS) sits at $220,400. While this provides a steady stream of income, relying solely on the FRS might leave you short. A monthly payout of approximately $1,780 is a start. However, maintaining a middle-class lifestyle in an expensive city requires more. This is where the Enhanced Retirement Sum (ERS) becomes vital. Navigating these regulatory shifts isn't easy. That's why a financial planner is your best ally in translating policy into a personal roadmap.

The 2026 ERS Milestone

The 2026 ERS cap has jumped to $440,800. This is a significant milestone for high-income earners. It's exactly four times the Basic Retirement Sum of $110,200. Why does this matter? Every dollar you move into your Retirement Account (RA) up to this limit increases your future CPF LIFE monthly payouts. It's the most reliable way to secure a higher "paycheck" for life. At Zenith Wealth, our financial planner team helps you project these figures accurately. We ensure you don't just hit the minimums, but reach the maximum potential of your accounts.

Inflation and the Purchasing Power of CPF LIFE

Relying on the 4% interest rate in your Special Account or Retirement Account is a safe bet, but it's not a complete one. Inflation can erode your purchasing power over decades. To build a true "Retirement Fortress," you need to augment your CPF savings. This means combining the stability of government schemes with the growth potential of i12 investments. By blending these, you create a portfolio that handles both safety and expansion. It's about ensuring your money grows faster than the cost of your morning coffee or medical bills. We help you bridge the gap between guaranteed payouts and the lifestyle you actually want to lead.

Strategic CPF Hacks to Accelerate Your Nest Egg Growth

Smart moves today create a smoother tomorrow. When it comes to maximizing CPF for retirement in Singapore, the difference between a comfortable life and a constrained one often lies in the timing of your actions. You don't need a massive windfall to see results. Instead, focus on consistent, tactical adjustments that leverage the way interest is calculated. Small shifts in how you handle your contributions can lead to six-figure differences over a twenty-year horizon. It's about being proactive rather than reactive.

The Power of Early Cash Top-Ups

Timing is everything. Most people wait until December to make cash top-ups for tax relief. This is a missed opportunity. By topping up on January 1st, you earn up to 11 extra months of interest compared to a year-end contribution. Over a decade, this "January 1st" rule can significantly boost your compound interest. You can receive tax relief of up to $8,000 for top-ups to your own account and another $8,000 for loved ones. The Retirement Sum Topping-Up Scheme (RSTU) serves as a powerful, tax-efficient growth engine for your future.

A financial consultant can help you determine the exact amount to top up without compromising your current cash flow. This ensures you hit the $16,000 tax relief cap while maintaining enough liquidity for private opportunities like i12 investments. For more details on building this momentum, check out the official CPF retirement planning guide. It provides a solid foundation for these cash-based strategies.

OA to SA Transfers: The Pros and Cons

The math is simple but the decision is permanent. Moving funds from your Ordinary Account (OA) at 2.5% to your Special Account (SA) at 4% creates an immediate 1.5% interest jump. This is a popular hack for younger workers with a long compounding runway. However, remember that this is a one-way street. Once money enters your SA, you can't move it back to your OA for housing or education. Most experts suggest stopping these transfers once you approach the Full Retirement Sum (FRS) to maintain some flexibility for property needs.

Beyond these steps, consider these 2026-specific tactics:

- Leverage the MRSS: If you have family members with lower balances, use the Matched Retirement Savings Scheme. The government matches dollar-for-dollar top-ups for eligible members, providing an instant 100% return.

- Evaluate SA Shielding: Be aware that for those turning 55 in 2026, the traditional "SA Shielding" technique is no longer viable due to the closure of the Special Account for older members. Strategy must now shift toward maximizing the Retirement Account directly.

- Optimize Tax Brackets: Don't just top up for the sake of it. Work with a financial planner to align your contributions with your highest tax brackets for maximum efficiency.

Your CPF isn't a standalone silo. It works best when integrated with a broader wealth plan. If you're unsure how these hacks fit into your specific situation, reach out for a personalized strategy session to align your accounts with your long-term goals.

Integrating CPF LIFE with i12 Investments for a Holistic Portfolio

Think of your retirement as a building. CPF LIFE is the foundation. It's the "safe floor" that ensures you always have a roof over your head. It acts like the ultra-stable bond component of your portfolio. However, a foundation isn't a complete house. To stay ahead of Singapore's persistent inflation, you need a growth engine. This is where maximizing CPF for retirement in Singapore meets the agility of private wealth strategies. You need both the guarantee of the government and the potential of the markets.

Some people ask why they should bother with private assets when CPF offers a guaranteed 4% interest rate. The answer is simple: liquidity and upside. CPF is a rigid system. Your funds are locked away until specific age milestones. While this protects you from spending impulses, it prevents you from reacting to market opportunities or personal emergencies. By integrating i12 investments into your plan, you gain the freedom to access capital when you need it most. You aren't just saving for a distant future; you're building a flexible life today.

The i12 Investment Advantage

i12 investments provide a level of global diversification that the CPF system simply cannot match. While your CPF accounts are essentially tied to the Singaporean economy, private portfolios can tap into global technology, healthcare, and emerging markets. This exposure is vital for long-term capital appreciation. Professional management ensures your portfolio is rebalanced and optimized for the 2026 economic climate. For a deeper look at these strategies, explore our guide on Strategic Investment Management in 2026.

Liquidity vs. Longevity: Finding the Balance

Finding the right balance between CPF and private cash is a personal journey. A common framework involves securing your Basic or Full Retirement Sum first, then funneling excess cash into more liquid vehicles. A financial planner can help you determine your "liquidity ratio." This ensures you have enough cash for the next five years while your CPF handles your life after 65. Many clients use the Supplementary Retirement Scheme (SRS) as a bridge. It offers immediate tax relief while allowing you to invest in private assets. Check out our detailed article on Mastering the SRS Account to see how it complements your CPF strategy.

Ready to see how these pieces fit together for your specific situation? Our team is eager to start a conversation. You can connect with us here to begin building your holistic roadmap.

A Financial Planner’s Roadmap: Maximizing CPF by Life Stage

Your age dictates your strategy. What works in your 20s won't be enough in your 50s. Maximizing CPF for retirement in Singapore is about evolving your approach as your career and income levels progress. It's not a static process. By tailoring your actions to your current life stage, you ensure that every dollar works as hard as possible for your future self. Here is how you should look at your roadmap over the decades.

- The 20s and 30s: Time is your greatest asset. Focus on the "Compounding Runway." Start moving funds from your Ordinary Account (OA) to your Special Account (SA) early. This locks in the 4% rate. It's a long-term play that turns modest contributions into a significant nest egg.

- The 40s: Your income is likely reaching its peak. This is the prime decade for tax optimization. Maximize your $8,000 top-ups for yourself and your loved ones. This reduces your taxable income while building your core retirement savings.

- The 65+: You don't have to take your payouts immediately. Deferring your CPF LIFE payouts can increase your monthly income by up to 7% for every year you wait, up to age 70. This is a powerful way to hedge against longevity risk.

The Critical Decade: Ages 45 to 55

This is the final sprint. For those in this bracket in 2026, the landscape is particularly unique. You must optimize your Special Account before you hit the age 55 milestone. With the 2026 closure of the Special Account for members aged 55 and above, your window to maximize that 4% interest environment is closing. Reaching the Enhanced Retirement Sum (ERS) of $440,800 before age 55 ensures you maximize your future monthly payouts from day one. Our team can help you project these final years to ensure no opportunity is missed.

To Withdraw or Not to Withdraw at Age 55?

The psychological trap of a lump-sum withdrawal is real. It's tempting to take the cash for immediate desires. However, leaving that money in your CPF accounts allows it to continue earning high, risk-free interest. Before you make a decision, consult a financial planner to determine your actual cash flow needs versus your long-term growth goals. We often find that a balanced approach is best. This involves keeping your CPF foundation intact while using i12 investments for your more liquid, growth-oriented needs. If you're approaching this milestone, contact us today for a bespoke roadmap tailored to your specific 2026 goals.

Partnering with Zenith Wealth for a Secure 2026 Retirement

Retirement planning isn't just about spreadsheets. While the CPF portal provides the data, it doesn't offer the context of your life. At Zenith Wealth, our financial planners look beyond the numbers. We focus on maximizing CPF for retirement in Singapore by aligning your accounts with your personal values and long-term vision. It's about creating a roadmap that feels like you. We don't believe in one-size-fits-all solutions. Instead, we offer a boutique experience that prioritizes human interaction alongside professional advisory services.

Our approach blends human-centric advice with modern professional standards. We believe that your financial journey should be as unique as your thumbprint. As authorized representatives of finexis advisory, our team has access to a wide range of solutions. This independence allows us to prioritize your interests above all else. We select the best products to suit your specific needs. Whether it's optimizing your RA account or managing your i12 investments, our priority is your progress. We act as your modern professional guide, steering you through the complexities of the 2026 regulations.

Preparing for your golden years is a conversation, not just a calculation. We're here to listen, guide, and grow with you. We value personal connection over institutional coldness. You aren't just a client number to us; you're a partner. Our communication is steady and expectant. We move logically from high-level goals to specific actions. This ensures your path to retirement is unobstructed by complex syntax or unnecessary fluff.

Beyond the Calculator: Tailored Strategic Insights

A standard calculator can't tell you how a sudden market shift or a family emergency will impact your lifestyle. That's why we offer a personalized "Retirement Stress Test." We look at how your plan holds up under various scenarios. We also ensure that your CPF strategy doesn't exist in a vacuum. We integrate legacy planning and education funding into your broader wealth roadmap. This holistic view ensures that your wealth protection and retirement goals are perfectly synced. For a deeper dive into these topics, check out The Complete Guide to Retirement Planning in Singapore (2026 Edition).

Start Your Journey Today

We invite you to experience a different kind of advisory. Our boutique firm maintains an open-door policy that encourages immediate connection. We want to hear your story. Start your journey today by booking a discovery session with us. It's a low-pressure way to see how we can help you navigate the 2026 landscape with confidence. Our team is proactive and eager to engage. Contact our financial planners to start the conversation. We're ready to grow alongside you!

Secure Your Financial Future for 2026 and Beyond

The 2026 landscape brings new challenges, but it also offers fresh opportunities for those who act early. By understanding the shift in ERS limits and applying strategic timing, you're already ahead of the curve. True success in maximizing CPF for retirement in Singapore requires more than just hitting government targets. Build a diversified portfolio that pairs your CPF LIFE payouts with the growth potential of i12 investments. This ensures your savings outpace inflation and provide the lifestyle you deserve.

You don't have to navigate these changes alone. As authorized representatives of finexis advisory, we specialize in seamless i12 investment integration. We provide boutique, human-centric financial guidance that puts your goals first. It's time to turn your retirement plan into a clear, actionable roadmap. Secure your 2026 retirement roadmap with a Zenith financial planner today.

Your golden years should be a time of celebration, not stress. Let's start the conversation and build a future you're excited to live. We're ready to help you grow.

Frequently Asked Questions

Is it better to top up CPF or invest in the Supplementary Retirement Scheme (SRS) in 2026?

The choice depends on your tax bracket and liquidity needs. CPF top-ups offer a guaranteed 4% interest in your Special or Retirement Account, which is hard to beat for risk-free returns. However, the SRS is excellent for high-income earners who want to reduce their taxable income while investing in private assets like i12 investments. A financial planner can help you balance both to ensure you don't lock away too much cash.

Can I still use my CPF Ordinary Account for housing if I transfer it to my Special Account?

No, you cannot move funds back once they are transferred. Moving money from your OA to your SA is a one-way street designed to boost your long-term interest. While this is a powerful move for maximizing CPF for retirement in Singapore, you must ensure you have enough remaining in your OA or cash reserves to cover your mortgage. Always calculate your housing buffer before committing to a transfer.

What is the maximum tax relief I can get from CPF top-ups in 2026?

You can enjoy a maximum tax relief of $16,000 per year through the Retirement Sum Topping-Up Scheme. This is split into $8,000 for top-ups to your own accounts and another $8,000 for top-ups to eligible family members. It's one of the most efficient ways to grow your nest egg while lowering your tax bill. Make sure to complete these top-ups early in the year to maximize your interest gains.

How much do I need in my CPF to receive $3,000 a month in retirement?

To reach a $3,000 monthly payout, you'll likely need to exceed the 2026 Enhanced Retirement Sum of $440,800. Since the Full Retirement Sum of $220,400 provides roughly $1,780 a month, hitting the ERS is the best way to get closer to your goal. For many, the gap between the ERS payout and a $3,000 target is best filled using private wealth strategies and i12 investments.

What happens to my CPF savings if I pass away before the payout age?

Your CPF savings are distributed to your nominees in cash if you have made a CPF nomination. If you haven't made one, the Public Trustee's Office distributes the funds according to Singapore's intestacy laws. It's important to know that CPF savings are not covered by a will. We recommend reviewing your nomination every few years to ensure it reflects your current life situation and legacy goals.

Can foreigners or PRs maximize CPF for retirement in the same way as citizens?

Permanent Residents can maximize their CPF in the same way as citizens once they reach their third year of PR status. Foreigners generally don't have CPF accounts unless they were part of older schemes. For PRs, maximizing CPF for retirement in Singapore involves the same top-up and transfer strategies discussed in this guide. If you're a PR, starting these habits early is vital for long-term stability.

Is the Enhanced Retirement Sum (ERS) mandatory to achieve?

No, the ERS is entirely optional. It's the maximum amount you can choose to keep in your Retirement Account to receive higher CPF LIFE payouts. You only need to meet the Full Retirement Sum, or the Basic Retirement Sum if you own a property with a sufficient lease. The ERS is simply a tool for those who want to maximize their guaranteed monthly income during their golden years.

How does i12 investments complement my CPF LIFE payouts?

i12 investments act as the growth engine that CPF LIFE lacks. While CPF LIFE provides a stable, guaranteed floor for your basic needs, private investments offer the potential for higher returns and capital appreciation. This combination helps you combat inflation and maintain your purchasing power. By blending the two, you create a diversified portfolio that offers both safety and the flexibility to enjoy your retirement fully.