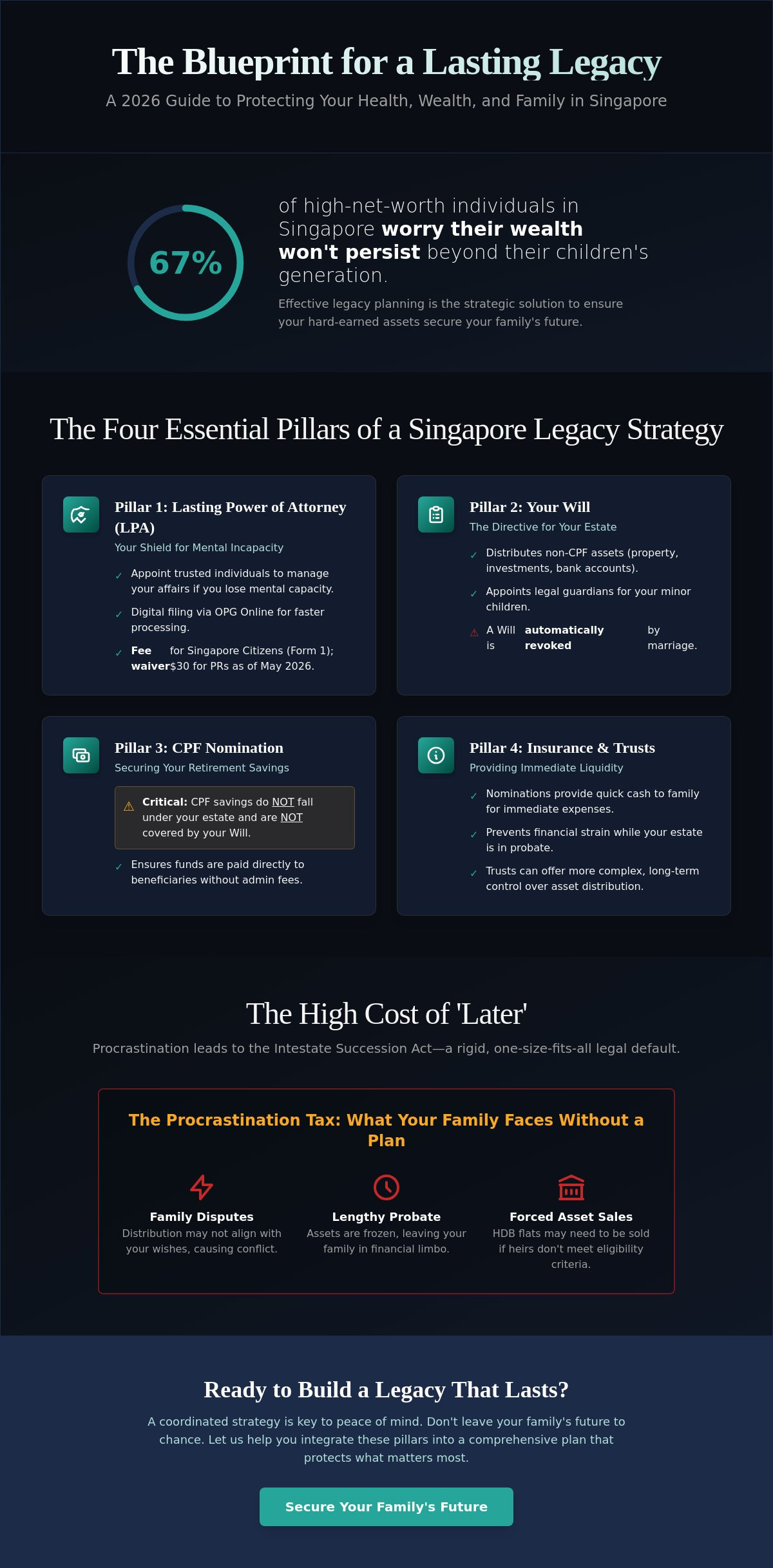

Did you know that 67% of high-net-worth individuals in Singapore worry their wealth won't persist beyond their children's generation? It's a staggering figure from a recent Sun Life survey. You've spent years building your assets, but the thought of family disputes or confusion over CPF nominations can keep you up at night. Effective legacy planning is much more than just a legal checklist. It's a strategic financial move that ensures your hard work benefits the people you love most without unnecessary friction.

We know how overwhelming it feels to balance Wills, Lasting Powers of Attorney, and trust structures. You want a clear path forward that protects your health and your wealth. This 2026 guide is here to help you secure that future. We'll show you how to integrate legal frameworks with smart financial advisory to minimize hurdles for your heirs. By the end, you'll have a clear roadmap for asset distribution and the peace of mind that your family is truly protected.

Key Takeaways

- Learn why legacy planning in 2026 goes beyond a simple Will to include your health, values, and mental incapacity protection.

- Identify the four essential pillars of a robust Singapore estate strategy, from the LPA to managing non-CPF assets and guardianship.

- Understand the hidden risks of DIY planning and why a strategy-first approach is vital to avoid conflicting nominations across your assets.

- Discover how to link your legacy with retirement and wealth protection to ensure your family's inheritance isn't lost to medical bills.

- Gain a clear roadmap to minimize legal hurdles for your heirs and achieve total peace of mind for your family's future.

Defining Legacy Planning: More Than Just a Will in 2026

Many people think legacy planning is a luxury reserved for the ultra-wealthy. That's a myth we need to bust right now. In 2026, legacy planning has evolved into a holistic strategy for everyone. It's about your health, your wealth, and the values you want to pass on. While a Will is a great start, it's only one piece of a much larger puzzle. Modern planning is life-stage-based. It accounts for your needs today while preparing for the future of your loved ones. We're seeing a shift where families focus on financial literacy for their heirs as much as the assets themselves. It’s no longer just about the transfer of cash; it's about the transfer of wisdom and stability.

The Shift from Distribution to Preservation

Traditional Estate planning often focuses solely on what happens after you're gone. Modern legacy planning starts while you're still very much here. It protects your assets during your lifetime, especially if you face mental incapacity. By the end of 2025, over 405,000 Singapore citizens had already registered a Lasting Power of Attorney (LPA). This isn't just about money. It's about making sure someone you trust can manage your affairs if you can't. Since the Ministry of Social and Family Development made LPA Form 1 free for Singapore Citizens, there's no reason to wait. This document ensures your wealth isn't locked away when you need it most. While estate planning deals with distribution, legacy building focuses on long-term preservation and impact.

Why "Later" is the Biggest Risk to Your Family

Procrastination is the silent enemy of a secure future. If you pass away without a clear plan, the Intestate Succession Act takes over. This legal default follows a strict hierarchy involving your spouse, children, and parents. It might not align with your wishes at all. For example, your HDB flat inheritance is subject to specific eligibility rules that can override your intentions. Heirs must meet HDB's criteria, or the property might have to be sold. This is the kind of complexity that catches families off guard. We call this the "procrastination tax." Beyond the financial cost, the emotional toll on your family is massive. Leaving them with a legal mess to untangle adds grief to an already difficult time. Proactive planning ensures your voice is heard, even when you aren't there to speak. It’s about clarity and care. If you're ready to start the conversation, reach out to our team today. We're here to help you build something that lasts.

The Four Essential Pillars of a Singapore Legacy Strategy

Successful legacy planning isn't a one-and-done task. It's a coordinated system of legal and financial tools that work together to protect your interests. Many Singaporeans mistake a Will for a complete plan, but that's only part of the story. A truly robust strategy covers your wealth, your health, and your retirement savings through four distinct pillars. You can manage several of these through the MyLegacy@LifeSG portal, which streamlines the process for modern families. By treating these elements as a unified strategy, you ensure no gaps are left for legal hurdles or family disputes to fill.

Legal Frameworks: LPA and Wills

The Lasting Power of Attorney (LPA) is your proactive shield for your autonomy. It allows you to appoint trusted individuals to make decisions on your behalf if you lose mental capacity. As of May 1, 2026, Singapore Citizens still enjoy a fee waiver for LPA Form 1, while Permanent Residents pay $30. The entire filing process is now digital via the Office of the Public Guardian Online system. This makes it faster and more accessible than ever to secure your future care and property management.

Your Will handles the distribution of your non-CPF assets, like private property, bank accounts, and investments. It also identifies guardians for your minor children. A Will isn't static. You must update it after major life events like marriage, which automatically revokes an existing Will in Singapore. For added security, you can register your Will's location with the Singapore Academy of Law Wills Registry for a $50 fee. This ensures your executors can find the document when it's needed most.

Financial Directives: CPF and Insurance

Don't assume your Will covers everything. Your CPF savings are a major exception. Because CPF funds don't form part of your estate, they aren't distributed according to your Will. You must make a specific CPF nomination to ensure these funds reach your beneficiaries quickly and without the cost of administration fees. To see how your savings might impact your heirs, use the CPF Retirement Sum Calculator 2026 to plan your expected payouts and legacies.

Insurance nominations and trusts provide another layer of protection. They offer immediate liquidity, providing your family with cash for funeral expenses or estate costs while your other assets are in probate. This prevents your loved ones from facing financial strain during an already difficult time. If you want to see how these pillars fit into your specific situation, start a conversation with our team. We'll help you build a plan that's as unique as your family.

Finally, consider Advance Care Planning (ACP). This pillar focuses on your medical preferences and end-of-life care. While the LPA deals with legal and financial power, the ACP records your personal values and healthcare wishes. Together, these four pillars create a safety net that protects your dignity and your family's harmony.

Professional Advisory vs. DIY: Navigating the Complexities

Filling out a form is not a strategy. It's the difference between having a map and knowing how to navigate the road. Many people fall into the "Document-First" trap. They think a quick digital filing equals a secure future. While government portals make the paperwork accessible, they don't provide the advisory needed to protect your wealth. Effective legacy planning requires a "Strategy-First" approach. This means looking at how your assets, legal documents, and family goals interact before you sign anything. You need to know how one decision affects another across your entire portfolio.

One of the biggest risks of a DIY approach is conflicting nominations. You might name a beneficiary in your Will, but if that asset is held in joint tenancy or has a specific insurance nomination, the Will might be ignored. These legal overlaps are exactly where family disputes begin. A professional helps you map out every asset class. They ensure your wishes are legally enforceable and financially sound. This coordination is what prevents legal hurdles for your heirs later on. It turns a collection of papers into a shield for your family.

The Limitations of Government Portals

Portals like MyLegacy are fantastic for efficiency. They're a great starting point for filing an LPA or checking your CPF status. However, a portal cannot account for complex family dynamics. It won't tell you if your plan is tax-efficient. It also won't help you understand how your strategy might be affected by future market volatility. Professional advisory includes "stress-testing" your strategy. We look at different scenarios to ensure your legacy remains intact regardless of economic shifts. A portal is a functional tool, but it isn't a guide for your life's work.

How Financial Consultants Bridge the Strategy Gap

Think of a financial consultant as the architect of your wealth roadmap. We don't just sell products. We coordinate the entire structure. We work alongside legal professionals to ensure your financial directives match your legal documents. As your career grows and your assets increase, your plan needs to evolve. We provide that ongoing relationship. This ensures your strategy is always up to date and relevant to your current life stage. Independent advice is vital when choosing the right legacy products for your specific needs. If you're ready to move beyond basic forms, let's start a conversation about your unique goals. Professional advice turns a pile of documents into a lasting legacy.

Integrating Legacy with Retirement and Wealth Protection

Your legacy isn't a separate box to check. It's the finish line of a comprehensive retirement plan. Think of it as a relay race. Your retirement is the final leg and your legacy is the handoff. Without a solid strategy, you risk running out of steam before you can pass the baton. In 2026, inflation continues to eat into the real value of cash savings. This means the inheritance you plan to leave today might buy significantly less in twenty years. Effective legacy planning accounts for this by ensuring your assets grow at a rate that outpaces rising costs.

A major threat to your family's inheritance is the cost of care. Robust wealth protection acts as a shield. It ensures that medical bills or long-term care costs don't drain the estate you've worked so hard to build. We also look at the synergy between tax-advantaged tools like Supplementary Retirement Scheme (SRS) accounts. These aren't just for tax relief today. They can be part of a strategic transfer of wealth that maximizes what your heirs actually receive.

Legacy Planning as a Part of Retirement Strategy

Every retiree faces the "Spend vs. Leave" dilemma. Do you enjoy your wealth now or save it for the next generation? We help you find that balance. Your CPF LIFE payouts provide a lifelong floor for your expenses, but they also impact what's left behind. By understanding how annuities and structured payouts work, you can enjoy your retirement comfort without sacrificing your children’s inheritance. It's about living well today while knowing the future is secure.

Hedging Wealth for the Next Generation

In 2026, a resilient legacy portfolio needs to look beyond local borders. We often discuss the role of gold and global assets to hedge against market shifts. Diversifying across different regions and asset classes protects your wealth from being tied to the performance of a single economy. Global investment management sustains wealth across decades and generations. It’s a proactive way to maintain your family's purchasing power. If you want to see how these pieces fit into your overall roadmap, reach out for a personal consultation. Let's make sure your hard work goes exactly where you intended.

Partnering with Zenith Wealth Group for a Secure Tomorrow

Choosing a partner for your legacy planning is a deeply personal decision. At Zenith Wealth Group, we act as your modern professional guide. We aren't a distant corporate entity; we're an attentive team eager to start a conversation with you. As authorised representatives of finexis advisory Pte Ltd, we bring professional integrity to every roadmap we build. We avoid the heavy, jargon-filled atmosphere of traditional firms. Instead, we offer a friendly, open-door policy. This human-centric approach ensures your values stay at the heart of your financial strategy. We believe that securing wealth is just as much about the people as it is about the assets.

The first steps in creating your personalised roadmap are simpler than you think. We don't start with complex paperwork. We start with your goals. We look at your current life stage, your family structure, and your vision for the future. This proactive engagement helps us identify gaps before they become problems. We want to understand what matters to you before we talk about numbers. It's about building a foundation of trust that lasts for generations.

The Zenith Advantage: Independent Advice

Our status as independent advisors gives you a distinct edge. We aren't limited to a narrow list of products. This independence allows us to scan the market and find the best fit for your specific needs. It's a level of flexibility you won't find at many large institutions. We focus heavily on serving parents and pre-retirees. These groups face unique challenges, from education funding to wealth preservation. Our commitment to professional integrity means we use transparent vocabulary. You'll always understand exactly what we're recommending and why. There's no hidden syntax or unnecessary complexity here. We prioritize clarity over everything else.

Start Your Conversation Today

We invite you to move from anticipation to action. It's easy to keep legacy planning on the back burner, but the best time to start is now. A friendly consultation is the first step toward total peace of mind. We've seen how a single 20-minute conversation can prevent years of family uncertainty and legal hurdles. It's about setting clear expectations for your heirs and securing your own future care. Don't let the procrastination tax drain your hard-earned assets. Take the lead and Contact Zenith Wealth Group today. We're ready to engage and grow alongside you. Let's ensure your tomorrow is as secure as it is bright.

Take the Lead on Your Family’s Future

You've seen that a secure future requires more than just a standard Will. It's about aligning your CPF nominations, LPA, and investment portfolio into a single, cohesive strategy. Professional legacy planning ensures your wishes are legally sound and financially protected against inflation or market shifts. By moving beyond a DIY approach, you remove the burden of uncertainty from your loved ones. You've worked hard to build your wealth; now it's time to ensure it stays protected.

At Zenith Wealth Group, we're ready to help you navigate these complexities. As authorised representatives of finexis advisory Pte Ltd, we specialize in the nuances of Singapore's estate and retirement laws. We don't believe in cold, institutional processes. Our human-centric advisory approach puts your family's values first. A quick conversation can provide the clarity you need to move forward with confidence.

Secure your family’s future with a personalised legacy consultation. Let's start building your secure tomorrow today.

Frequently Asked Questions

What is the difference between estate planning and legacy planning?

Estate planning focuses primarily on the legal distribution of your assets after you pass away. Legacy planning is a more holistic approach that includes your healthcare preferences, personal values, and active wealth protection while you're still alive. It's a life-stage strategy designed to ensure your family’s stability and your own autonomy across every decade.

Do I need a lawyer or a financial consultant for legacy planning in Singapore?

You often benefit from both to ensure a seamless strategy. A financial consultant acts as the architect of your roadmap, coordinating your retirement funds, insurance, and investments. A lawyer provides the specific legal drafting for complex Wills or trusts. Working with a consultant first helps you define the strategy before you commit to the legal paperwork.

Can I change my legacy plan after it has been filed digitally?

Yes, you can update your digital filings as your life circumstances change. Systems like the Office of the Public Guardian (OPG) and MyLegacy allow you to revise your documents to reflect new wishes or beneficiaries. It's vital to keep these records current so they don't conflict with your actual intentions as your wealth grows.

How does a CPF nomination work if I already have a Will?

Your CPF nomination always takes precedence over your Will for your CPF savings. These funds don't form part of your estate and aren't distributed through the probate process. This separate system ensures your beneficiaries receive your retirement savings quickly and without the burden of legal administration fees. Always keep both documents updated to avoid confusion.

What happens to my assets if I lose mental capacity without an LPA?

Your family will have to apply to the court for a Deputyship order to manage your affairs. This process is often slow, expensive, and emotionally draining for your loved ones. Without an LPA, your bank accounts could be frozen, making it difficult for your family to pay for your medical care or daily expenses. An LPA keeps you in control by choosing your decision-makers in advance.

Is legacy planning only for those with significant property or investments?

No, legacy planning is essential for anyone who wants to protect their family and their own dignity. Even if you only have a modest savings account or a HDB flat, a plan prevents legal hurdles and family disputes. It's about ensuring your wishes are respected and that your loved ones aren't left with a complex legal mess to untangle.

How often should I review my legacy plan in Singapore?

Review your strategy every three to five years or whenever you experience a major life event. Events like marriage, divorce, or the birth of a child significantly change your legal requirements. For example, marriage in Singapore automatically revokes any Will you previously made. Regular reviews ensure your roadmap always aligns with your current family situation and financial goals.