Did you know it's possible to withdraw a total of $400,000 from your Supplementary Retirement Scheme account without paying a single cent in tax? For many, the fear of a 5% penalty for an early srs withdrawal or confusion over the 10-year window makes the process feel like a minefield. You've worked hard to build your savings. It's only natural to feel protective over your retirement nest egg.

Our financial planners are here to help you master the 10-year withdrawal strategy. We'll show you how to minimize taxes and maximize your income through expert planning. This guide provides a clear 10-year schedule to ensure your withdrawals stay tax-free. You'll also learn how to integrate these funds seamlessly with your i12 investments portfolio for a stress-free transition. Let's build a retirement plan that works for you.

Key Takeaways

- Understand how the 10-year window and statutory retirement age impact your penalty-free access to funds.

- Master the 50% tax concession to plan an srs withdrawal strategy that can potentially net you $400,000 tax-free.

- Follow a simple audit process to determine your personal annual withdrawal threshold based on other income sources.

- Navigate the specific holding periods and withholding tax regulations required for foreigners and expats.

- Sync your staggered payouts with your i12 investments to create a reliable income stream before CPF LIFE begins.

Understanding the SRS Withdrawal Rules and the 10-Year Window

The Supplementary Retirement Scheme (SRS) isn't just a tax relief tool. It's a strategic pillar for your future. While the Central Provident Fund (CPF) provides a mandatory foundation, the SRS allows for voluntary flexibility. You've likely spent years contributing to lower your tax bracket. Now, you need to understand the withdrawal phase. This is where your planning either pays off or costs you. Most people think of it as a simple bank account. It's actually a 10-year tax optimization project.

The 10-Year Withdrawal Clock Explained

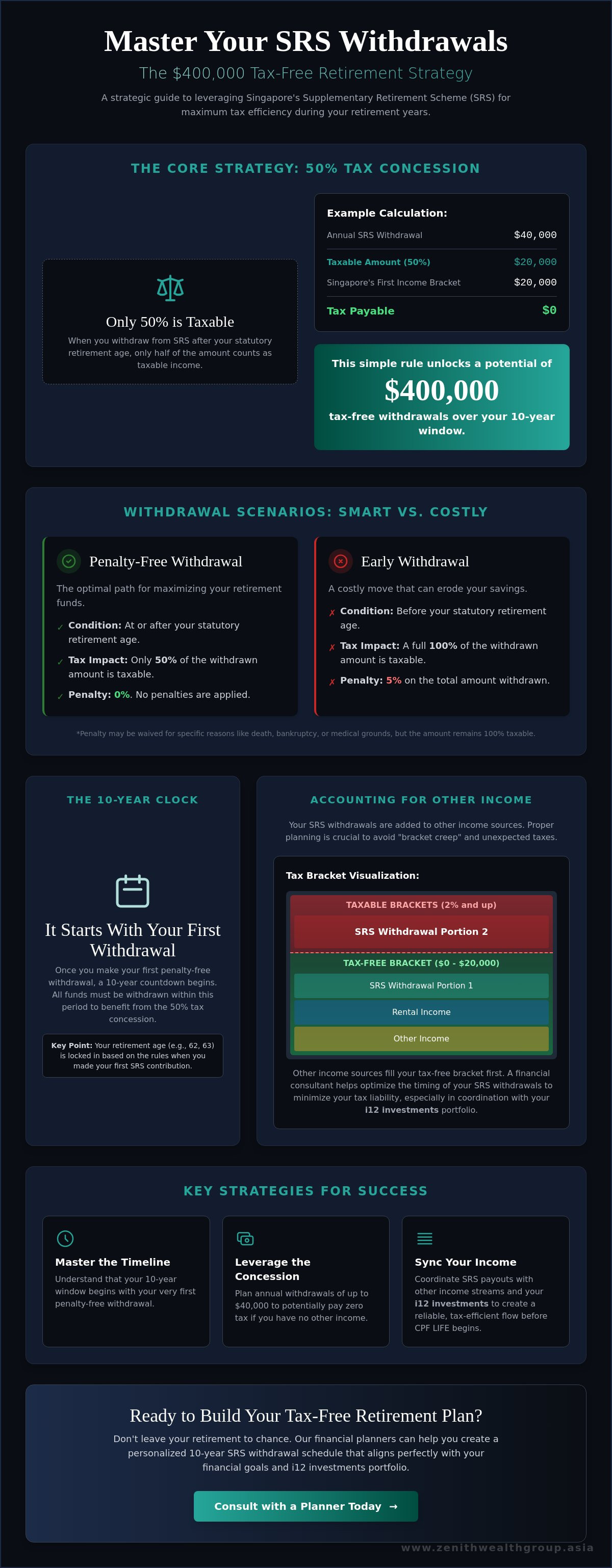

Timing is everything. Your 10-year withdrawal window begins the moment you make your first penalty-free srs withdrawal. This window consists of ten consecutive years. You don't have to empty the account immediately. Instead, you can stagger payments to keep your taxable income low. As of May 2026, the prescribed retirement age is 63. However, the law is changing. It's set to increase to 64 starting 1 July 2026. Your specific penalty-free age is locked in based on when you made your very first contribution. If you opened your account years ago, your age might be 62. If you start today, it's 63. Don't let these shifting dates catch you off guard.

You shouldn't start withdrawals until you truly need the income. Once that first dollar leaves the account after your prescribed age, the clock starts ticking. It doesn't stop, even if you skip a year. This makes the initial date of withdrawal one of the most important decisions in your retirement timeline. It requires a clear view of your projected expenses and other income sources.

Penalty-Free vs. Early Withdrawal Scenarios

Don't rush to pull funds early. If you withdraw before your prescribed age, the consequences are heavy. You'll face a 5% penalty on the withdrawn amount. Worse, 100% of that withdrawal becomes taxable income. This can easily push you into a higher tax bracket and wipe out years of tax savings. There are limited exceptions to this rule where the 5% penalty is waived:

- Withdrawals made on medical grounds

- Withdrawals due to bankruptcy

- Withdrawals following the death of the account holder

Even in these cases, the money is still fully taxable. A financial planner can help you avoid these pitfalls. They ensure your cash flow needs are met without triggering unnecessary fees. You have choices in how you receive your money. You can take cash or opt for an investment-in-kind withdrawal. This means transferring your stocks or units directly to your personal account without selling them first. This is particularly useful for your i12 investments. It allows your assets to continue growing while you fulfill the withdrawal requirements. Managing these moving parts requires precision. Our team at Zenith Wealth Group is ready to guide you. Reach out to a financial consultant to sync your SRS strategy with your broader portfolio. Visit our contact page to start the conversation.

Calculating Your Tax-Free Sweet Spot: The 50% Concession

The 50% tax concession is the most powerful feature of the Supplementary Retirement Scheme. It effectively doubles the value of your tax-free threshold during your golden years. When you make an srs withdrawal at or after your prescribed retirement age, only half of the amount is considered taxable income. This benefit is designed to reward long-term savers. It allows you to stretch your savings further than a standard savings account ever could. Understanding the official SRS withdrawal tax rules is the first step to keeping your hard-earned money in your pocket.

The Math Behind the 50% Tax Concession

Let's look at the numbers. In Singapore, the first $20,000 of your total annual income is taxed at 0%. Because of the 50% concession, you can withdraw $40,000 from your SRS account each year. The tax authorities only see $20,000 of that. If you have no other income, your tax bill stays at zero. Over a 10-year period, this adds up to $400,000 in tax-free liquidity.

What if you need more? If you withdraw $80,000 in a single year, only $40,000 is taxable. Based on the 2026 tax brackets, you would pay 0% on the first $20,000. You would then pay 2% on the next $10,000 ($200) and 3.5% on the final $10,000 ($350). You receive a massive $80,000 payout but only pay $550 in tax. That is an effective tax rate of just 0.68%. This math makes the scheme an incredible tool for wealth preservation.

Accounting for Other Income Sources

Your "sweet spot" isn't a fixed number for everyone. It changes based on your total financial picture. If you still earn a salary or receive rental income from a property, that income fills up your lower tax brackets first. This is where "bracket creep" becomes a risk. If your rental income already hits $20,000, every dollar from your srs withdrawal will be taxed at the prevailing rates, starting from the 2% bracket or higher.

This is why holistic planning is essential. You must coordinate your withdrawals with the rest of your portfolio, including your i12 investments. Some assets provide capital gains which are generally tax-free, while others provide taxable yield. Balancing these helps you stay within the lowest possible tax bracket. A financial planner can run a personalized tax simulation to find your exact limit. Don't leave your tax bill to chance. You can connect with a financial consultant to audit your various income streams and optimize your 10-year schedule. We'll help you ensure your withdrawal strategy fits perfectly with your lifestyle needs.

How to Stagger SRS Withdrawals for Maximum Tax Efficiency

Execution is where your strategy meets reality. To maximize your tax savings, you need a blueprint that spans a full decade. Staggering your srs withdrawal isn't just about taking money out. It's about timing. Don't leave it to the last minute. Start with a clear, five-step process to ensure every dollar is optimized.

- Step 1: Audit your total SRS balance. Calculate your projected needs over the next 10 years. If your balance is $400,000, a $40,000 annual withdrawal is the baseline for zero tax, assuming no other income.

- Step 2: Determine your annual threshold. Factor in rental income, part-time work, or dividends. If you earn $10,000 elsewhere, your tax-free SRS limit drops to $20,000 per year since only 50% of the withdrawal is taxable.

- Step 3: Choose your method. Decide between cash or "withdrawal-in-kind". You can move shares directly without selling them.

- Step 4: Execute the transfer. Move your funds or assets to your personal brokerage or i12 investments account. Ensure the bank processes the request within the correct tax year.

- Step 5: Schedule an annual review. Meet with your financial consultant every December. Tax laws and your personal income levels can change. Adjust your next withdrawal accordingly.

The Advantage of Withdrawal-in-Kind

Selling during a market downturn is a retiree's nightmare. Withdrawal-in-kind allows you to move your i12 investments without selling them. You avoid unnecessary transaction fees and stay invested in the market. For tax purposes, the withdrawal value is based on the closing price of the assets on the day of the transfer. This ensures your 10-year clock keeps running without forcing you to exit the market at the wrong time. It's a seamless way to maintain your portfolio's growth potential while meeting statutory requirements.

Re-investing Your SRS Proceeds

Your money shouldn't sit idle once it leaves the SRS environment. The goal is to shift funds into higher-yield i12 investments that align with your long-term needs. Maintaining your asset allocation is vital during this drawdown phase. You can use these proceeds to fund specific Retirement Planning Singapore goals, such as wealth protection or legacy planning. It's about keeping your capital working for you even as you start to spend it. If you're unsure how to re-allocate these funds, connect with a financial planner for a personalized portfolio review. We can help you bridge the gap between your SRS savings and your broader investment strategy.

Special Circumstances: Foreigners, Expats, and Medical Grounds

Foreigners and expats face a unique set of rules that differ significantly from those for Singapore Citizens. If you're not a Permanent Resident, your srs withdrawal journey has different milestones. You don't necessarily have to wait until the statutory retirement age to access your funds without a penalty. However, you must navigate withholding tax and specific holding periods to protect your i12 investments from unnecessary costs. Understanding these nuances is the difference between a smooth exit and a tax headache.

When a non-resident makes a withdrawal, the bank is required to withhold tax. This is typically 15% or the prevailing non-resident rate. It often feels like a steep price to pay. Here's a professional tip: you can often claim some of this back. If your actual tax liability based on resident tax rates is lower than the withheld amount, you can file a tax return to request a refund. This requires careful documentation and a clear understanding of your tax residency status during the year of withdrawal. It's a proactive step that many expats overlook.

The Expat SRS Withdrawal Roadmap

Timing your departure from Singapore is a strategic move. Foreigners have a special "Lump Sum" option that isn't available to locals in the same way. If you've held your SRS account for at least 10 years from the date of your first contribution, you can withdraw the entire balance at once. In this scenario, the 5% early withdrawal penalty is waived. Only 50% of that lump sum will be subject to withholding tax. This is a massive advantage if you're planning to move to a lower-tax jurisdiction or need a clean break from the Singapore system. For a deeper dive into these rules, read our SRS Account for Foreigners guide.

Emergency Withdrawals and Terminal Illness

Life can be unpredictable. The government acknowledges this through specific penalty waivers for medical grounds. If you face physical or mental incapacity or a terminal illness, you can access your SRS funds early. In the case of terminal illness, the 5% penalty is waived. While the research indicates that the withdrawn amount remains fully taxable in many early exception cases, the ability to access liquidity during a crisis is vital. It allows you to reallocate funds to immediate care or wealth protection needs.

Planning for the unthinkable is part of a robust retirement strategy. If an account holder passes away, a "deemed withdrawal" occurs. The entire SRS balance is treated as if it were withdrawn on the date of death. This can create a sudden, large tax bill for your estate. This is why Legacy Planning is so important. It ensures your i12 investments and remaining SRS funds are distributed to your loved ones according to your wishes, with minimal tax friction. Don't leave your family to guess your intentions. You can speak with a financial consultant today to build a contingency plan that covers every scenario.

Integrating SRS into Your Holistic Retirement Plan

Retirement is a multi-layered journey. It's not just about one account or a single payout date. You need a strategy that synchronizes the three pillars of Singapore's retirement system: CPF LIFE, your Supplementary Retirement Scheme, and your private investments. Each serves a distinct purpose. Your CPF LIFE provides a lifelong floor. Your private i12 investments offer growth and flexibility. Your srs withdrawal strategy acts as the vital bridge between the two.

Many retirees choose to stop working before their CPF LIFE payouts begin at age 65. This creates an income gap. If your prescribed retirement age allows, starting your srs withdrawal at age 63 or 64 can provide a steady "salary" during those early years. It ensures you don't have to dip into your long-term capital too early. By staggering these payments over a decade, you maintain a smooth cash flow while keeping your tax liability at zero. This coordination turns a simple savings plan into a robust retirement engine.

Managing these moving parts is complex. A financial planner helps you visualize how these different income streams flow together. They ensure your asset allocation remains balanced even as you draw down your funds. Our goal is to keep your i12 investments working for you while you enjoy the fruits of your labor. This proactive approach prevents accidental tax traps and maximizes your net wealth.

Balancing SRS and CPF LIFE

Coordinating your 10-year window with your CPF start date is essential. You want to avoid a situation where a large SRS payout coincides with other taxable income, pushing you into a higher bracket. This is also the time to ensure your Wealth Protection remains intact. As you transition from accumulating wealth to spending it, safeguarding your remaining assets becomes a top priority. We'll help you manage your cash flow so your lifestyle stays consistent throughout your golden years.

Next Steps: Your SRS Review

Your strategy shouldn't be static. We recommend a full review at age 55 when your CPF accounts are restructured. You should review it again at age 62, just before your withdrawal window typically opens. These sessions allow you to run a personalized simulation of your 10-year plan. You can Contact a Zenith Wealth Group financial consultant today to start your review. We're ready to help you navigate the 2026 rules and build a plan that lasts. Let's start the conversation and secure your future together.

Take Control of Your Future Income

Mastering your srs withdrawal is about more than just tax savings. It's about creating a sustainable lifestyle that lasts. You now understand how to leverage the 50% tax concession and the 10-year staggering strategy. By coordinating these payouts with your CPF LIFE and i12 investments, you ensure your retirement salary remains robust and tax-efficient. Every decision you make today protects the wealth you've spent decades building.

Our team at Zenith Wealth Group consists of authorized representatives of finexis advisory. We specialize in boutique, personalized retirement roadmaps that simplify complex regulations. As experts in i12 investments strategies, we help you transition from accumulation to a smooth drawdown phase with confidence. Don't leave your tax-free threshold to chance. It's time to put your plan into action.

Plan your tax-free SRS withdrawal with a Zenith financial consultant. We're ready to help you navigate the path ahead. Your dream retirement is within reach.

Frequently Asked Questions

Can I withdraw my SRS funds in the form of shares or only cash?

You can choose to withdraw your funds as cash or through an "investment-in-kind" transfer. This allows you to move your i12 investments directly to your personal brokerage account without selling them first. It's a great way to avoid transaction fees or selling when market prices are low. Your financial planner can help you value these assets correctly for tax reporting purposes.

What is the best age to start my SRS withdrawal in Singapore?

The best age depends on your personal cash flow needs and other taxable income sources. Most people start at their prescribed retirement age, which is currently 63 for many account holders. Starting later allows your investments more time to grow. However, you must finish all withdrawals within 10 years of your first one. A personalized simulation can help you find your specific "sweet spot."

How much tax will I pay if I withdraw my SRS before age 63?

Withdrawing before your prescribed age triggers a 5% penalty on the total amount. Additionally, 100% of the withdrawal is treated as taxable income rather than the usual 50%. This can significantly increase your tax bill and reduce your retirement savings. It's best to wait until your statutory age unless you meet specific medical or bankruptcy criteria for a penalty waiver.

Does the 10-year withdrawal period have to be consecutive?

Yes, the 10-year srs withdrawal window is strictly consecutive. The clock starts the moment you make your first penalty-free withdrawal. Even if you don't take any money out in the following years, the window continues to close. This makes the timing of your very first withdrawal a critical part of your long-term strategy to ensure you don't run out of time.

What happens to my SRS account balance if I pass away?

Your account balance is subject to a "deemed withdrawal" on the date of death. The full amount is treated as taxable income for that year. This could result in a large tax liability for your estate. Proper legacy planning is vital to ensure your beneficiaries receive as much of your i12 investments as possible without being burdened by a sudden tax bill.

Can I still contribute to my SRS account after I start making withdrawals?

You cannot make any further contributions once you begin penalty-free withdrawals from your account. The scheme is designed for the accumulation phase to end when the withdrawal phase begins. If you still have a high income and need tax relief, talk to a financial consultant about other wealth protection strategies before you trigger that first withdrawal.

How do foreigners claim back withholding tax on SRS withdrawals?

Foreigners can claim a refund by filing an Individual Income Tax Return in the following year. While banks withhold tax at 15% or the non-resident rate, your actual tax might be lower if you qualify for resident rates. Keeping clear records of your srs withdrawal and residency status is essential for a successful claim with the tax authorities.

Is it better to withdraw SRS as a lump sum or stagger it?

Staggering is generally superior for tax efficiency. By spreading withdrawals over 10 years, you can stay within the 0% tax bracket for the first $20,000 of taxable income. A lump sum withdrawal often pushes you into much higher tax brackets. This could result in paying thousands of dollars in taxes that could have been avoided with a steady 10-year plan.