What if you could legally shield S$35,700 of your annual income from the taxman while building a portable nest egg? Many expats view the Supplementary Retirement Scheme as a black box, fearing their funds will be locked away forever. It's a valid concern. You want to lower your current tax bill, but you need to know if an srs account for foreigners is actually worth it if you might relocate in five or ten years.

We understand that Singapore tax laws feel complex. It's frustrating to watch your salary shrink under high tax brackets while missing out on the CPF benefits available to locals. This guide simplifies everything. We'll show you how to use the SRS as a high-yield tax arbitrage tool to save up to S$7,854 this year alone. You'll get a clear breakdown of the 2026 contribution limits, the 10-year holding rule, and the smartest withdrawal strategies for your eventual move abroad. Let's get started.

Key Takeaways

- Maximize your yearly tax relief by utilizing the S$35,700 contribution cap available to expats.

- Master the 10-year holding rule to unlock flexible withdrawal options before the statutory retirement age.

- Avoid the 0.05% idle interest trap by investing your srs account for foreigners into growth-oriented assets.

- Plan a tax-efficient exit strategy to ensure 50% of your retirement withdrawals remain tax-free.

- Partner with a professional guide to build a portable retirement nest egg that works wherever your career takes you.

What is the Supplementary Retirement Scheme (SRS) for Foreigners?

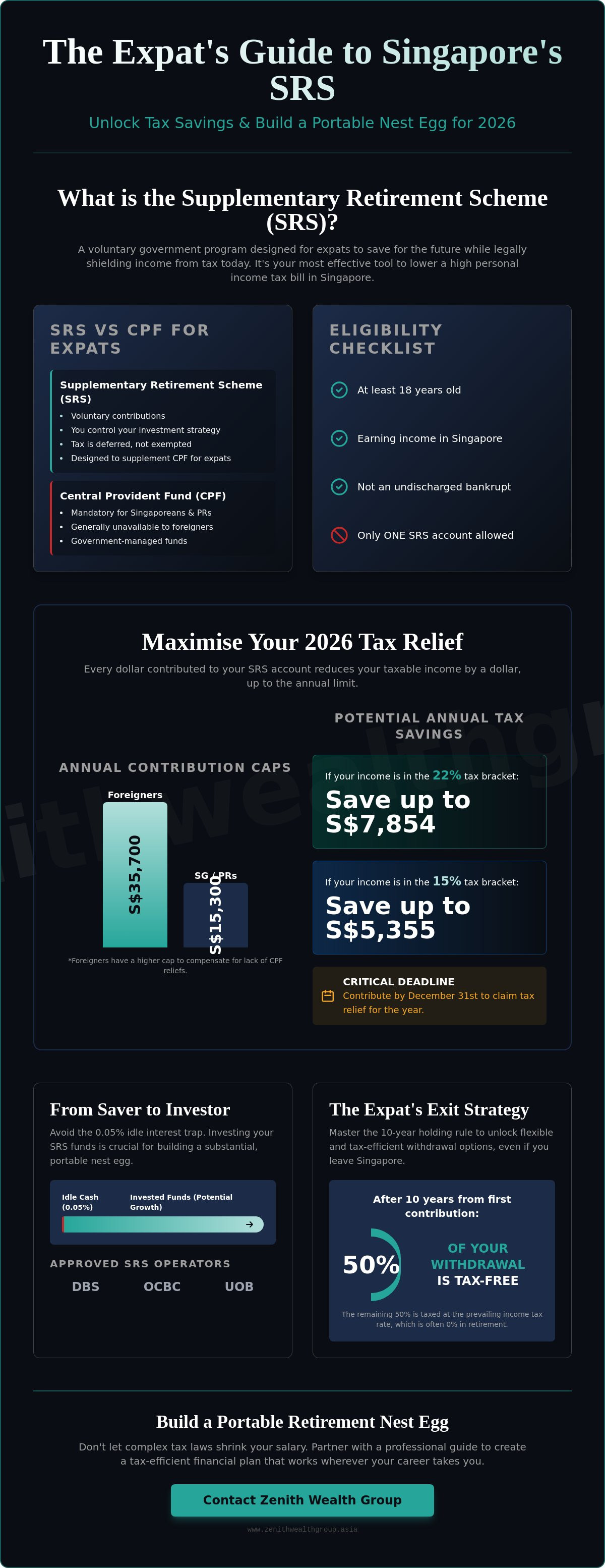

The Supplementary Retirement Scheme (SRS) is a voluntary program designed by the Singapore government to help you save for the future while paying less tax today. For most expats, an srs account for foreigners is the single most effective way to lower a high personal income tax bill. Since you don't have access to the Central Provident Fund (CPF), the SRS fills that gap. It's essentially a tax deferment tool. You reduce your tax burden now during your high-earning years and pay a much lower rate later when you withdraw the funds.

The 2026 tax relief benefits are significant. For every dollar you contribute, you receive a dollar-for-dollar reduction in your taxable income. If you contribute the maximum amount allowed for foreigners, you could see a substantial drop in your tax bracket. This isn't a complex loophole; it's a government-backed incentive to encourage long-term financial planning. You can start this process by opening an account with one of the three approved SRS operators: DBS, OCBC, or UOB. These banks act as the custodians for your funds, but they don't dictate how you use them.

Key Differences Between SRS and CPF for Expats

Foreigners are generally ineligible for CPF, which is the mandatory savings system for Singapore Citizens and PRs. This makes the SRS vital for your long-term security. While CPF is a mandatory, government-directed system, SRS is entirely voluntary. You decide when to contribute and how much. Crucially, you also control the investment strategy. Your funds aren't sitting in a government-managed account; they are in an account you oversee. This flexibility allows for a more personalized approach to retirement planning and investment management. You aren't tied to a specific government interest rate; you're in the driver's seat.

Eligibility Criteria for Non-Singaporeans

Opening an srs account for foreigners is straightforward. You must be at least 18 years old and not an undischarged bankrupt. You need to be earning income in Singapore to benefit from the tax relief. Without "earned income," there is no tax to offset, which defeats the primary purpose of the scheme. You can only hold one SRS account at any time. If you try to open a second one, you may face penalties. It's a simple, one-account-per-person rule that keeps the system transparent. If you're ready to optimize your tax strategy and build a more secure future, drop us a line!

2026 SRS Contribution Limits and Tax Relief for Foreigners

For 2026, the annual contribution cap for an srs account for foreigners remains at S$35,700. This is significantly higher than the S$15,300 limit set for Singapore Citizens and Permanent Residents. The reason is simple. Expats don't benefit from CPF tax reliefs, so the government provides a larger SRS window to level the playing field. Every dollar you put in reduces your taxable income by that same dollar. However, you must keep the S$80,000 total personal income tax relief cap in mind. If your other reliefs already hit this ceiling, additional SRS contributions won't lower your tax bill further.

The "tax sweet spot" for high earners occurs when your contribution pulls your remaining income into a lower tax bracket, effectively generating an immediate return through tax savings. To secure these benefits, you must complete your transfer by December 31st. We recommend acting by mid-December. Bank processing times can vary, and a late transfer means losing a full year of tax relief. It's a simple deadline, but missing it is a costly mistake.

Calculating Your Tax Savings

Let's look at the math. If you are in the 15% tax bracket, contributing the full S$35,700 to your srs account for foreigners saves you approximately S$5,355 in taxes. For those in the 22% bracket, that same contribution saves nearly S$7,854. This is an immediate, risk-free gain that boosts your net worth before you even invest the funds. You can find more detailed breakdowns in our SRS Tax Relief guide. Understanding how SRS Tax Relief for Foreigners applies to your specific income level is the first step toward efficient wealth management.

Contribution Deadlines and Mechanics

Tax relief is claimed in the Year of Assessment (YA) following your contribution. For example, any funds you deposit in 2025 are claimed in YA 2026. Be careful about the "one account" rule. Opening multiple accounts across different banks is prohibited and leads to financial penalties. To avoid the year-end rush, consider setting up a monthly standing instruction. This ensures you consistently hit your target without a large lump-sum hit in December. It's a proactive way to manage your cash flow while staying on track for retirement. If you need help structuring these contributions alongside your other financial goals, reach out to our team for a quick chat.

Navigating SRS Withdrawals: The 10-Year Rule for Foreigners

Most people assume they must wait until the statutory retirement age to touch their savings. In 2026, that age is 63. While this applies to locals, an srs account for foreigners offers a unique and powerful exit strategy. If you've maintained your account for at least 10 years from the date of your first contribution, you can withdraw your funds in a one-time lump sum. This exception is exclusive to non-Singaporeans. You don't have to stay in Singapore until you're 63 to access your money. You just need to meet the 10-year holding requirement and be a non-resident at the time of withdrawal.

The financial incentive for waiting a decade is massive. Only 50% of your withdrawal is subject to tax. This creates a significant tax arbitrage opportunity. You get a 100% tax deduction on your contributions today while you're in a high tax bracket. Ten years later, you withdraw the funds and only pay tax on half the amount. If you time your withdrawal during a year when you have no other Singapore income, your effective tax rate could drop to nearly zero. This is why the timing of Opening an SRS Account is so critical. The 10-year clock starts the moment you make your first dollar of contribution.

The 5% Early Withdrawal Penalty

Plans change, but withdrawing early from your srs account for foreigners is costly. If you pull funds before the 10-year mark or before reaching the statutory retirement age, you lose the tax benefits. The government will tax 100% of the withdrawn amount as income. To make matters worse, they apply a 5% penalty on top of that. This penalty exists to discourage using the SRS as a short-term savings account. Unless you face a true financial emergency, avoid early withdrawals. They often wipe out all the tax savings you worked hard to accumulate.

Withholding Tax for Non-Resident Withdrawals

When you eventually withdraw your funds as a non-resident, your bank is legally required to withhold tax. This isn't a hidden fee; it's a compliance measure. The bank (DBS, OCBC, or UOB) will typically withhold 15% of the gross withdrawal amount. If your withdrawal is exceptionally large, they may withhold at the top marginal rate. Don't worry. This isn't your final tax liability. You can file a tax return with IRAS to claim the 50% concession and receive a refund for any excess tax withheld. For help navigating the paperwork of a cross-border exit, reach out for personalized exit planning. We'll help you ensure your exit is as tax-efficient as possible.

Strategic Investment Options for Your SRS Funds

Don't let your tax savings evaporate through inflation. Leaving your funds idle in an srs account for foreigners earns a negligible 0.05% interest rate. While the initial tax break is a win, the real wealth-building power lies in how you deploy that capital. Within the SRS wrapper, all your investment gains, including dividends and capital growth, accumulate tax-free. This allows for much faster compounding than a standard taxable brokerage account. You're essentially creating a tax-sheltered environment for your long-term growth.

Approved investment classes for these funds are diverse. You can choose from unit trusts, Singapore-listed REITs, and specific insurance-linked products. Because your goal is long-term retirement funding, risk management is paramount. You aren't just looking for high-octane growth; you're looking for sustainable, protected wealth that survives market cycles. The key is to match your investment choices with your expected residency timeline in Singapore.

Balancing Growth and Wealth Protection

Many expats opt for endowment plans within their SRS portfolio. These products often provide capital guarantees, ensuring your principal remains safe while offering significantly better returns than a bank account. Dividends from REITs also play a vital role. By reinvesting these payouts tax-free, you accelerate the growth of your nest egg. For a deeper look at how to balance these assets, see our Wealth Protection guide. This approach ensures your retirement plan is resilient against both market volatility and inflation.

Portfolio Rebalancing for Expats

Your strategy should change as you approach the 10-year withdrawal mark we discussed earlier. Shifting from aggressive equity funds to lower-risk fixed income assets helps lock in your gains. You must also consider currency fluctuations. Since your SRS assets are denominated in SGD, their value relative to your home currency will shift over time. Professional oversight ensures your portfolio remains aligned with your global retirement goals, not just your Singaporean tax needs. If you want to build a resilient, tax-efficient portfolio, book an investment management consultation today. We'll help you align your SRS strategy with your broader financial roadmap.

Optimizing Your SRS Strategy with Zenith Wealth

Building wealth in a foreign country requires more than just a high salary. It requires a partner who understands the nuances of the Singaporean system. At Zenith Wealth, we act as your modern professional guide. We bridge the gap between tax regulations and your personal aspirations. Our team moves away from the cold, institutional feel of traditional firms. We offer a friendly, open-door policy that prioritizes human connection. Managing an srs account for foreigners is a great start, but we help you look at the bigger picture.

Our business model is designed for the modern global citizen. We offer both fee-based and commission-based structures, providing the transparency you need. We take a holistic view of your financial health. This includes legacy planning, education funding, and long-term wealth protection. Your Singaporean assets should be a cornerstone of your global portfolio. Drop us a line! for a complimentary tax optimization review to see where you stand.

Tailored Solutions for Career-Driven Expats

Starting early is the best way to maximize your returns. We help young professionals navigate the setup process and select growth-oriented investments. By integrating your srs account for foreigners into the Complete Guide to Retirement Planning, we ensure your strategy is cohesive. We focus heavily on portability. Whether your career keeps you here for three years or thirty, your wealth must remain tax-efficient. We help you build a nest egg that works anywhere.

Start Your 2026 Planning Today

The tax benefits of the SRS are too significant to ignore. Opening an account today secures your relief for the current year and starts the 10-year clock for non-resident withdrawals. It's a simple move that yields massive long-term results. Don't wait for the year-end rush to scramble for tax savings. Take control of your financial future now with a professional roadmap. Book a consultation with our experts today. We are ready to engage and help you reach your financial zenith.

Secure Your Financial Future in Singapore

You now have the blueprint to transform a high tax burden into a strategic retirement advantage. By utilizing an srs account for foreigners, you aren't just capturing immediate relief; you're building a tax-sheltered engine for long-term growth. The unique 10-year withdrawal rule and the 50% tax concession provide the flexibility every global professional needs. Don't let your savings sit idle when they could be compounding toward your ultimate financial goals.

Zenith Wealth is here to ensure your strategy is seamless and effective. As an authorized representative of finexis advisory, we specialize in crafting financial roadmaps specifically for the expat community. Our holistic 2026 tax-efficiency analysis looks beyond the basics to align your SRS contributions with your broader legacy and investment goals. We pride ourselves on being an approachable partner that values your time and your vision for the future.

Ready to lower your 2026 tax bill? Drop us a line for a customized SRS strategy!

A more secure future is just one conversation away. We look forward to helping you reach your financial zenith. Let's get started today!

Frequently Asked Questions

Can I open an SRS account if I am on an Employment Pass (EP)?

Yes, you can open an account while on an Employment Pass. Since you're earning income in Singapore, you qualify for the dollar-for-dollar tax relief benefits. It's the most effective way for EP holders to lower their taxable income while building a long-term nest egg.

What is the maximum I can contribute to SRS as a foreigner in 2026?

The 2026 contribution cap for an srs account for foreigners is S$35,700. This is significantly higher than the S$15,300 limit for Singapore Citizens and PRs. This higher cap helps you offset the fact that you don't receive CPF tax reliefs on your employment income.

Is there a penalty if I close my SRS account and leave Singapore?

Yes, if you close the account before meeting the 10-year holding rule or reaching the statutory retirement age. You'll face a 5% penalty on the total amount. Additionally, 100% of the withdrawn funds will be taxed as income in the year you close the account.

How long must a foreigner hold an SRS account to avoid the 5% penalty?

You must hold the account for at least 10 years from the date of your first contribution. This specific rule allows foreigners to make a one-time lump sum withdrawal without the 5% penalty. It also unlocks the 50% tax concession, making your exit much more cost-effective.

What happens to my SRS funds if I become a Permanent Resident (PR)?

Your annual contribution limit will drop immediately to S$15,300. You also lose the "10-year rule" exception available to foreigners. Once you're a PR, you must wait until the statutory retirement age (63 in 2026) to make penalty-free withdrawals, just like a Singapore Citizen.

Can I use SRS funds to buy property in Singapore?

No, you cannot use these funds for real estate. The SRS is designed for financial investments like unit trusts, REITS, and endowment plans. While you can't buy a home with it, you can use the tax savings to bolster your overall wealth and property-buying power elsewhere.

How is the withholding tax calculated for foreigners withdrawing from SRS?

Banks are required to withhold 15% of the gross withdrawal amount for non-residents. If your withdrawal is very large, the bank may withhold tax at the top marginal rate instead. You can later file a tax return to claim the 50% concession and receive a refund of any excess tax.

What are the best low-risk investment options for SRS funds?

Singapore Savings Bonds (SSB) and T-bills are excellent low-risk choices that offer better returns than the 0.05% idle rate. You might also consider capital-guaranteed endowment plans. These products protect your principal while providing a steady path toward your retirement goals.