Imagine opening a tuition invoice for a primary school in Jakarta and seeing a figure like USD 28,000 for the year. As the sole provider, that number isn't just a bill; it's a heavy reminder that every financial choice rests entirely on your shoulders. Managing finances as a single parent in Jakarta requires more than just a tight budget in 2026. With local inflation reaching 3.08% in May, the "Jakarta Premium" is real. You're likely feeling the strain of rising costs while trying to build a safety net without a second income to lean on.

We understand that your goal isn't just to get by. You want to ensure your children have every opportunity possible. This guide shows you how to secure your family's future and build lasting wealth through strategic engineering. You'll learn how a financial planner can help you structure education funding and robust wealth protection. At i12 investments, we believe in proactive planning over reactive spending. We'll explore a clear roadmap for your child's schooling, disability protection, and a retirement strategy that lets you look forward to the future with confidence.

Key Takeaways

- Understand the "Sole Pillar" reality and how to navigate specific inflation risks unique to single providers in the Indonesian economy.

- Learn the essential steps for managing finances as a single parent in Jakarta by building a defensive moat through wealth protection and the i12 investments framework.

- Discover how to outpace the "Education Inflation" trap when planning for top-tier international schooling costs in Jakarta.

- Break the "Retirement Paradox" to ensure your long-term security while simultaneously establishing a clear legacy through Indonesian estate planning.

- See how a dedicated financial planner transforms basic budgeting into a professional roadmap tailored for your family's specific needs.

Navigating Jakarta’s Financial Landscape as a Sole Provider

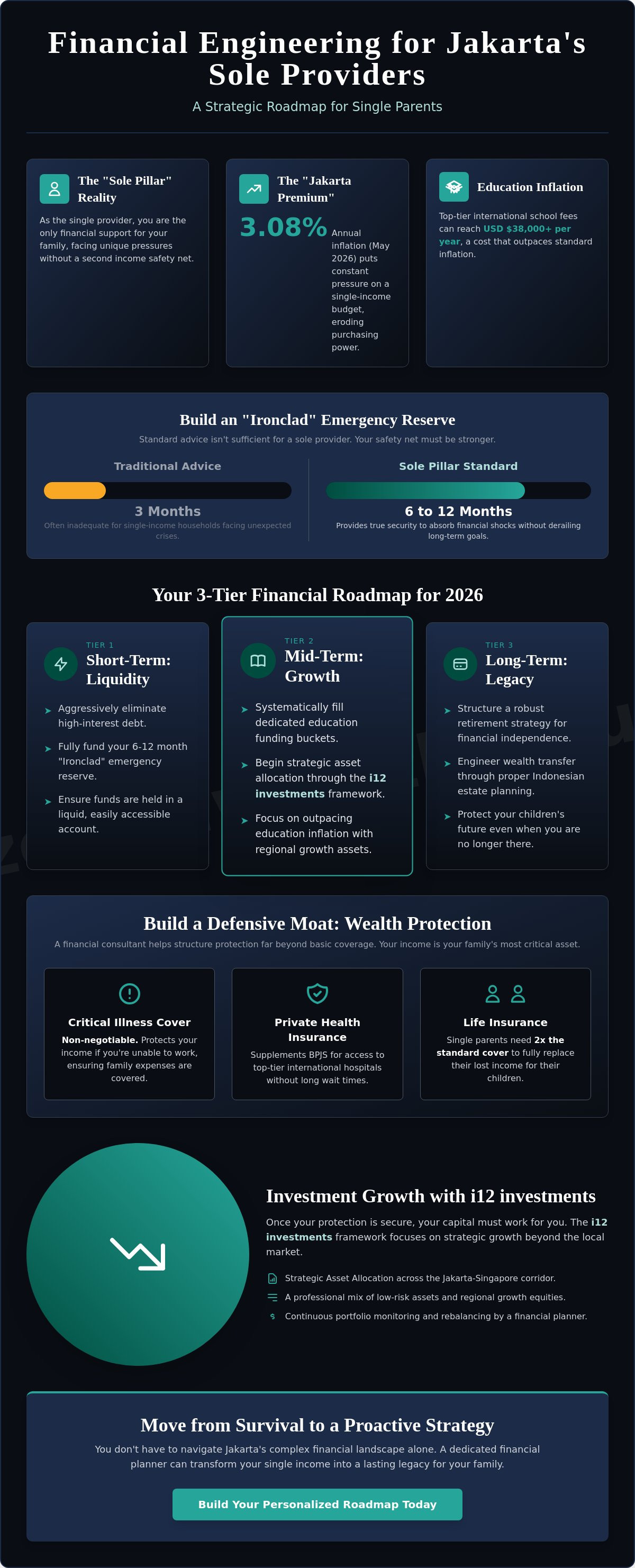

Being the "Sole Pillar" of a household in Jakarta means you're the only person standing between your family and financial instability. When you're managing finances as a single parent in Jakarta, you don't have a second income to absorb shocks like the 3.08% annual inflation rate recorded in May 2026. This reality changes how you should view risk. Traditional personal finance principles often suggest a three month emergency fund, but for a single parent in this city, that isn't enough. You need an "Ironclad" reserve of 6 to 12 months of expenses to feel truly secure.

Financial security in the Indonesian context isn't just about having money in the bank. It's about ensuring your lifestyle doesn't erode your future. Jakarta is famous for "lifestyle creep." It starts with frequent Gojek orders and ends with high overheads that leave nothing for growth. At i12 investments, we focus on helping you distinguish between financial security, which protects your current state, and financial independence, which funds your future freedom. You need a strategy that accounts for the fact that you're the primary engine for every financial goal your family has.

Understanding Jakarta’s Specific Economic Pressures

Living in Jakarta comes with a hidden "convenience tax." While domestic help and ride-hailing services are accessible, they can silently consume a single-income budget. Local inflation often hits food and fuel hardest, but as a single parent, you're also dealing with the rising cost of imported goods and international services. It's vital to use OJK-regulated financial products for your core savings. These provide a layer of legal protection and professional oversight that's non-negotiable for sole providers. Protecting your downside is just as important as chasing growth.

Setting 2026 Financial Milestones

Your roadmap needs clear markers to stay on track. A professional financial planner can help you categorize these goals to ensure no part of your life is left vulnerable. Consider these three tiers for your 2026 strategy:

- Short-term: Focus on debt elimination and immediate liquidity. You want your emergency fund fully funded and accessible in a liquid account.

- Mid-term: Start filling your education buckets. With international school fees reaching up to USD 38,000 for high school, early and consistent allocation is essential.

- Long-term: This is where we look at retirement and legacy planning. You aren't just saving; you're engineering a wealth transfer that protects your children even when you're no longer there to provide.

If you're ready to move from survival to a proactive strategy, reach out to us to start building your personalized roadmap. We're here to help you turn your single income into a lasting legacy.

Engineering Your Cash Flow and Wealth Protection Strategy

Basic budgeting tools like digital "pockets" are excellent for managing daily spending. However, managing finances as a single parent in Jakarta requires a more sophisticated engine to drive long-term wealth. You aren't just looking to survive the month; you're building a defensive moat around your family's future. This process starts with a professional audit of your current cash flow. A financial consultant can help you move from reactive saving to proactive wealth engineering by identifying where your capital is most effective.

Wealth Protection Beyond BPJS

While BPJS provides a vital safety net, it often falls short of the comprehensive coverage a sole provider needs in a high-cost city. Private health insurance ensures access to top-tier international hospitals without the long wait times that could keep you away from your career. Critical illness insurance is non-negotiable for solo providers. If you're unable to work, your income stops, but your family's expenses do not. Resources like the Single Moms Indonesia Community often highlight how unexpected health shocks are the primary hurdle for solo parents. Single parents need twice the standard life cover because there is no second income to mitigate the loss of the primary breadwinner.

Investment Growth with i12 investments

Once your protection is set, your money needs to work as hard as you do. Using the i12 investments framework, we focus on strategic asset allocation that looks beyond the local Jakarta market. This approach provides essential exposure to regional growth while actively balancing volatility. It's about finding the right mix of low-risk assets and growth-oriented regional equities to ensure your wealth outpaces inflation. A financial planner plays a crucial role in this journey. They monitor market shifts across the Jakarta-Singapore corridor and rebalance your portfolio to stay aligned with your long-term goals. This professional oversight prevents emotional decision-making during market dips.

Engineering a robust strategy means looking at the big picture rather than just the next bill. You don't have to navigate these complex regional markets alone. You can speak with a financial planner today to audit your existing Indonesian policies and ensure your protection is truly ironclad for the years ahead.

Education Funding: Securing Your Child's Future in Jakarta

Education inflation in Jakarta often moves at double the rate of the Consumer Price Index. For the sole provider, this creates a unique pressure. Managing finances as a single parent in Jakarta means you aren't just saving for today's costs; you're chasing a moving target. Top-tier institutions like Jakarta Intercultural School (JIS) and British School Jakarta (BSJ) represent the gold standard for many families, but their fee structures require precise engineering. In 2026, tuition for high school years can reach up to USD 38,000 annually. When you factor in capital levies ranging from USD 2,000 to USD 10,000, the first-year bill often carries a 40% premium over the base tuition.

Relying on a simple savings account isn't enough to bridge this gap. You need a strategy that outpaces the rising cost of local private national schools, which now range from IDR 50 million to over IDR 200 million per year. Our Guide to Education Funding offers a deeper look at how to structure these multi-year commitments effectively. By using the i12 investments framework, you can align your portfolio with these specific milestones, ensuring your capital grows in tandem with your child’s academic journey.

The International School Roadmap

Success in managing finances as a single parent in Jakarta involves distinguishing between sinking funds for immediate fees and long-term investment-linked plans. Sinking funds handle the predictable annual development fees and extracurricular costs. Meanwhile, investment-linked plans target the heavy lifting of secondary school and university. The 'Education Gap' for single-income families is the widening chasm between a parent's current savings rate and the hyper-inflated future cost of elite schooling. A financial planner can help you calculate this gap with precision, ensuring your monthly contributions are realistic and effective.

University Planning for Global Citizens

If your goal is a university in Singapore, Australia, or the UK, currency volatility is your biggest risk. Saving in Indonesian Rupiah for a future USD or SGD expense can lead to significant shortfalls if the exchange rate shifts. We focus on building global education funds that are tax-efficient and currency-hedged. Starting this process at birth versus age ten drastically changes your required monthly contribution; the power of compounding is a single parent's most loyal ally. By leveraging i12 investments for regional market exposure, you can build a diversified pool of wealth that remains resilient regardless of local market fluctuations.

Retirement and Legacy Planning: Beyond the Single-Income Trap

Many solo providers fall into the 'Retirement Paradox.' They prioritize every cent for their children's international school fees while leaving their own future unfunded. This is a high-stakes gamble. Managing finances as a single parent in Jakarta means you must be your own safety net. You don't have a partner's pension or savings to fall back on. Relying on your children for support in 2026 is increasingly risky as the cost of living in Southeast Asia continues to climb. Your goal is to be a financial resource for your children, not a future liability.

Designing Your Retirement Exit Strategy

A comfortable retirement in Jakarta requires a clear understanding of your future overheads. You need to account for healthcare, housing maintenance, and the "Jakarta lifestyle" you've worked hard to build. Investment management is the key to turning your current surplus into a passive income stream. By utilizing the i12 investments framework, we help you build a portfolio that generates consistent returns. This ensures that when you stop working, your capital starts working for you. A financial planner can calculate exactly how much you need to save today to maintain your independence tomorrow.

Guardianship and Asset Protection

Legacy planning is about more than just money. It's about control. Without a formal Will and estate plan, the Indonesian state could determine how your assets are distributed. This is especially critical for single parents with minor children. You must choose a guardian who aligns with your values and has the capacity to care for your family. We recommend drafting a 'Letter of Wishes' alongside your formal legal documents. This informal guide provides your chosen guardian with specific instructions on your child's upbringing and financial management. Your comprehensive legacy strategy should include:

- A Formal Will: To designate beneficiaries and clarify asset distribution according to Indonesian law.

- Legal Guardianship: Explicitly naming who will care for your children to avoid state intervention.

- Cross-border Coordination: Understanding Legacy Planning in Singapore if you hold regional investments or accounts.

- Trust Structures: Ensuring assets are managed professionally for minor children until they reach a specific age.

Estate clarity is a collaborative effort. A financial consultant works alongside legal experts to ensure your Will, trusts, and insurance beneficiaries are all perfectly aligned. This proactive approach ensures your assets stay with your children, providing them with the security you've worked so hard to build. Don't leave your family's future to chance. You can schedule a legacy planning session with our team to start securing your children's inheritance today.

How a Financial Consultant Transforms Your Financial Roadmap

Managing finances as a single parent in Jakarta shouldn't feel like a solo trek through a storm. While many people start with "DIY budgeting" using simple apps or spreadsheets, these tools often fall short of the strategic foresight needed for complex wealth engineering. A digital pocket can track your groceries, but it won't help you navigate cross-border tax implications or the specific risks of the Jakarta-Singapore corridor. A financial planner bridges this gap. They turn a static list of expenses into a dynamic strategy that grows with you. This transition from self-service to professional advisory is where true security begins.

The shift from anxiety to action happens when you have a partner to share the burden of decision-making. As the sole provider, the pressure of "getting it right" can be paralyzing. Professional guidance replaces that guesswork with data-driven confidence. We focus on building a roadmap that doesn't just look at next month's bills, but at the next decade of your family's life. By shifting your focus from survival to strategic growth, you can finally move toward long-term peace of mind.

The Zenith Wealth Group Advantage

We provide tailored solutions for young parents and pre-retirees throughout Southeast Asia who need more than just generic advice. Our partnership with finexis allows us to offer specialized advice on investments and insurance that remains objective and focused entirely on your family's goals. We don't just look at your bank account; we look at your life. If you're ready to stop guessing and start growing, it's time to Contact a Financial Consultant. We're here to help you navigate the complexities of regional wealth management with clarity and care.

Your 90-Day Action Plan

Moving from financial uncertainty to an actionable roadmap happens in stages. We recommend a structured 90-day approach to stabilize and then scale your wealth. This plan ensures that every rupiah is working toward your family's future. Here is how we start:

- Step 1: Audit all current Indonesian and offshore assets. We look at everything from your local BPJS coverage to your regional property holdings and bank accounts.

- Step 2: Define 'Must-Have' vs 'Nice-to-Have' goals. Your financial planner helps you prioritize international school fees and wealth protection without sacrificing your own retirement security.

- Step 3: Implement the i12 investments strategy. We set your diversified portfolio in motion and schedule quarterly reviews to ensure your plan remains resilient against Jakarta market shifts.

Taking this first step changes the narrative of your family's story. You aren't just a single parent managing a budget; you're a wealth engineer building a legacy. With the right support and the i12 investments framework, you can secure your child's future while ensuring your own financial independence remains ironclad. Let's start that conversation today.

Take Control of Your Family's Financial Legacy

Building a secure future as a solo provider requires shifting from reactive saving to proactive wealth engineering. We've explored the necessity of an "Ironclad" emergency fund and the power of the i12 investments framework to outpace Jakarta's unique inflation risks. By addressing the education gap early and establishing a clear estate plan, you're doing more than just surviving; you're building a lasting legacy for your children.

Managing finances as a single parent in Jakarta is a significant responsibility, but you don't have to carry it alone. Our team at Zenith Wealth Group consists of authorized representatives of finexis advisory. We specialize in education and retirement planning with deep regional expertise across Singapore and Indonesia. We're ready to help you transform your current anxiety into a robust, actionable roadmap.

Secure your family's future; speak with a Zenith Wealth Group financial consultant today. Your journey toward lasting financial confidence starts with a single conversation. We look forward to growing alongside you and your family.

Frequently Asked Questions

Is it better to save for my child's education or my retirement first?

You should prioritize your retirement because there are no loans for retirement, whereas children have access to scholarships and financing for school. Managing finances as a single parent in Jakarta requires this difficult trade off. A financial planner can help you build a strategy that funds both goals simultaneously by using the i12 investments framework to maximize your surplus cash flow.

How much should a single parent in Jakarta have in an emergency fund?

You should aim for 6 to 12 months of total household expenses. As a sole provider, you don't have a second income to absorb shocks like sudden job loss or medical emergencies. Since Jakarta's cost of living is rising, your fund must cover rent, international school fees, and domestic help to ensure your family's lifestyle remains stable during a transition.

What are the best investment options for single parents using i12 investments?

The most effective options focus on regional market exposure to hedge against local currency volatility. Through i12 investments, we prioritize a diversified mix of low volatility assets and growth oriented regional equities. This approach helps your capital outpace the 3.08% inflation rate while providing the liquidity you might need for mid term goals like school development fees.

Can a financial consultant help me manage assets across both Indonesia and Singapore?

Yes, a financial consultant provides essential coordination for assets held across the Jakarta-Singapore corridor. We help you navigate different regulatory environments and manage the currency risks between IDR, SGD, and USD. This regional expertise is vital for single parents who want to maintain a global investment footprint while living in Indonesia.

What happens to my children's finances if I am no longer able to work?

Your wealth protection strategy, specifically critical illness and disability insurance, acts as your income replacement. These policies provide a lump sum or regular payments to cover your family's living costs and school fees. It's the only way to ensure your children's financial future stays on track if your ability to earn is compromised.

How do I protect my assets from being mismanaged by a future guardian?

Setting up a formal trust structure is the most effective way to protect your legacy. A trust ensures that your assets are managed by professionals according to your specific instructions. This prevents a guardian from accessing funds for anything other than your children's welfare, providing a legal layer of safety for their inheritance.

Are international schools in Jakarta worth the investment for a single-income family?

International schools are a significant investment, with high school tuition reaching up to USD 38,000 annually. They are worth it if you intend for your child to attend university abroad and pursue a global career. However, this commitment requires a professional financial plan to ensure the fees don't jeopardize your long term retirement security.

How often should I review my financial plan with a financial planner?

You should review your roadmap at least once a year or whenever you experience a major life change. Jakarta's economic environment and tax regulations can shift quickly. Regular reviews with your financial planner ensure your i12 investments portfolio and insurance coverage remain perfectly aligned with your family's needs and current market conditions.