Could a strengthening Singapore dollar actually be the silent thief of your global investment gains? Many local investors watch their international assets climb, only to see those profits shrink when converted back to a rising SGD. It's a common frustration. With the MAS recently announcing a slight increase in the rate of S$NEER appreciation in April 2026, the challenge of managing currency risk in investment portfolio Singapore has never been more relevant.

We understand that unpredictable exchange rate swings can make your financial future feel uncertain. You've worked hard for your wealth, and you deserve a portfolio that stays stable in SGD terms. This guide provides the clarity you need. You'll learn how to protect your global wealth using strategic frameworks that align with the latest MAS policy shifts. We'll also explain how i12 investments helps you navigate these complexities with quiet confidence.

We'll preview the 2026 currency trends and show you exactly how to decide when to hedge your assets. Whether you're collaborating with a financial planner on retirement planning or wealth protection, these insights will help you turn volatility into a diversification advantage. Let's start a conversation about securing your global gains today.

Key Takeaways

- Decode the MAS exchange rate mechanism to see how the S$NEER basket directly influences your portfolio stability.

- Learn the essential frameworks for managing currency risk in investment portfolio Singapore to protect your global wealth from SGD volatility.

- Compare the real-world performance of hedged versus unhedged funds to identify the most cost-effective path for your wealth protection goals.

- Discover how the i12 investments approach to asset allocation helps you reduce USD-dependency through strategic G10 currency diversification.

- Understand the value of working with a financial consultant to gain institutional-grade insights and avoid the high transaction costs of DIY management.

What is Currency Risk and Why Does it Matter in Singapore?

If you've ever held US stocks while the Singapore dollar strengthened, you've felt the sting of currency risk. Put simply, What is Currency Risk involves the potential for financial loss because of shifts in exchange rates. It's the difference between what your investment earns in its home market and what actually lands in your bank account here in Singapore. For many local investors, managing currency risk in investment portfolio Singapore is the missing piece of their long term financial strategy.

This isn't about active currency speculation. We aren't looking to "beat the market" by guessing which way the yen will move tomorrow. Instead, we're looking at the incidental risk that comes with owning global assets. When the SGD is strong, it creates a dual impact. Your foreign dividends buy fewer groceries at the local supermarket, and your capital gains can vanish when converted back to SGD. In 2026, with the MAS continuing to favor a stronger local dollar to fight imported inflation, this risk is front and center for every local investor.

The Hidden Cost of Global Diversification

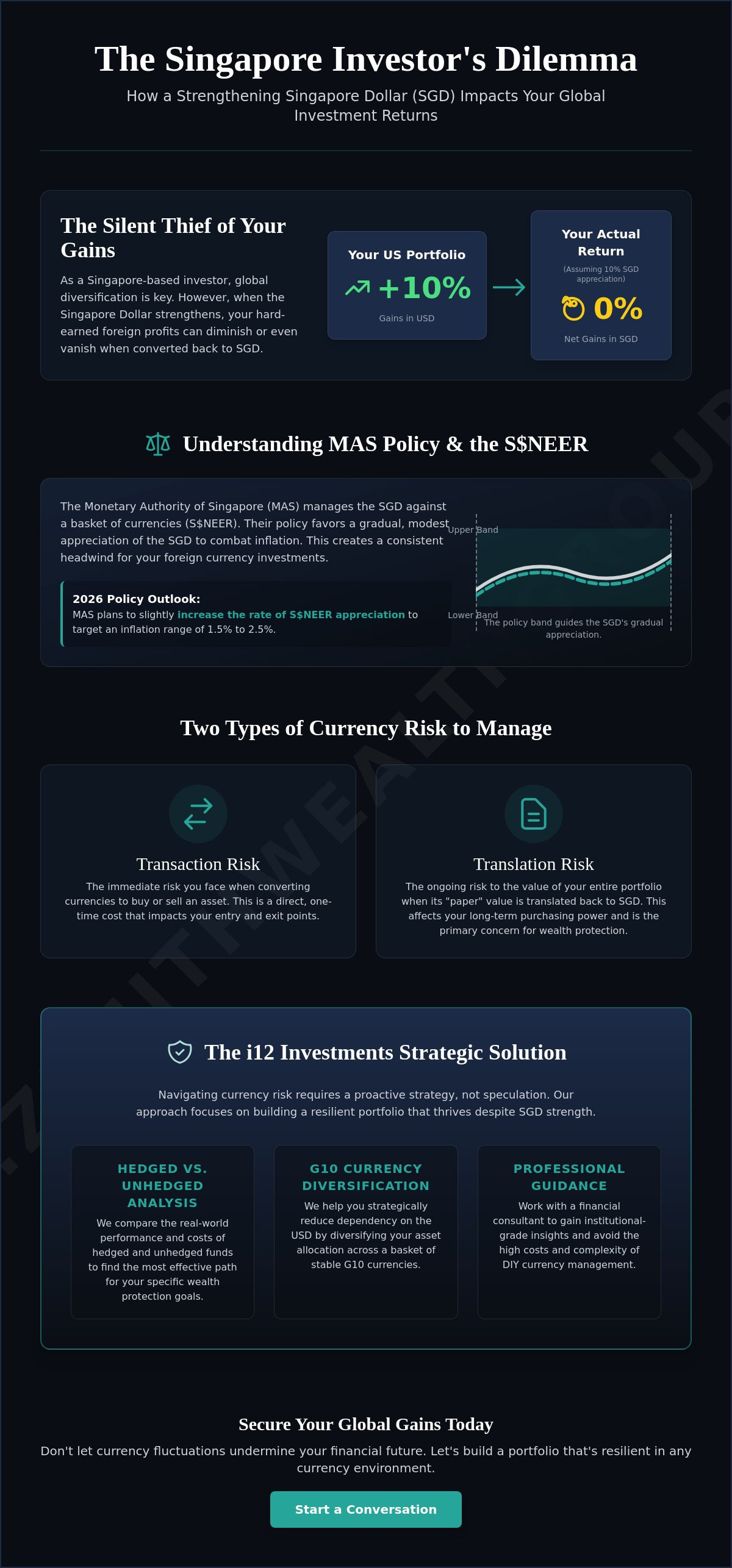

We often tell clients that staying purely in Singapore assets is a mistake. It creates a dangerous concentration in a single, small market. However, going global has a price. Imagine your US tech portfolio grows by 10% over a year. If the SGD also appreciates by 10% against the USD in that same period, your actual return in local terms is zero. This is especially true for sectors like global tech or international bonds, which are highly sensitive to these swings. At i12 investments, we help you see these hidden costs before they impact your wealth protection goals.

Transaction Risk vs. Translation Risk

It's helpful to distinguish between two types of exposure. Transaction risk is the immediate cost you pay when you physically swap SGD for USD to buy a stock. It's a one-time hurdle. Translation risk, however, is more subtle. This is the "paper" value of your entire portfolio when measured in SGD. Even if you don't sell your assets, a rising Singapore dollar makes your global wealth look smaller on your monthly statement. For successful investment management, translation risk is the primary concern. It affects your future purchasing power and your ability to fund a stable retirement. A financial consultant can help you determine which risks are worth hedging and which are simply part of a healthy, diversified plan.

Understanding the MAS Exchange Rate Policy and Portfolio Stability

Most central banks use interest rates to steer their economies. The Monetary Authority of Singapore (MAS) takes a different path. It manages the Singapore dollar against a secret basket of currencies from our major trading partners. This unique approach is the single most important factor when managing currency risk in investment portfolio Singapore. By focusing on the exchange rate, MAS provides a stability corridor that helps dampen global price shocks and keep our economy steady.

In April 2026, the MAS announced it would increase slightly the rate of appreciation for the S$NEER. This move targets the projected 2026 inflation range of 1.5% to 2.5%. When managing currency risk in investment portfolio Singapore, you must account for this intentional strengthening of the local dollar. While a stronger SGD helps keep your cost of living down, it also means your foreign assets face a steady currency headwind that can erode your returns.

The S$NEER Mechanism Explained

The S$NEER (Singapore Dollar Nominal Effective Exchange Rate) operates within a policy band. Think of the slope as the speed of appreciation, the mid-point as the target value, and the width as the room for movement. This mechanism is designed to protect the purchasing power of your savings over the long term. Understanding the mas exchange rate policy is vital for anyone planning for retirement or wealth protection. It also helps you understand the impact of US economy on Singapore investments. When the US economy fluctuates, the MAS adjusts the band to ensure our local economy remains resilient. How currency fluctuations impact investments often depends on how far the SGD deviates from this policy mid-point.

Why the SGD is a 'Safe Haven' Currency in 2026

Singapore maintains a rare AAA credit rating and massive foreign reserves. This makes the SGD a global safe haven. During times of market stress, investors often flock to the SGD. This causes the currency to strengthen exactly when your global stocks might be falling. If you hold USD-denominated assets, this flight to safety can amplify your losses in SGD terms. At i12 investments, we analyze these correlations to help you decide when to stay unhedged versus when to protect your gains. If you're feeling unsure about your current exposure, a quick chat with a financial planner can offer the clarity you need to move forward with confidence.

Hedged vs. Unhedged Portfolios: A 2026 Comparison

Choosing between a hedged and unhedged share class is a pivotal decision when managing currency risk in investment portfolio Singapore. Many investors assume that hedging is always the "safer" choice. This is a common misconception. While hedging protects you from a strengthening Singapore dollar, it also cuts you off from potential gains if the SGD weakens. More importantly, hedging is never free. You pay for this protection through forward contract fees and the interest rate differential between the SGD and the foreign currency. If the cost to hedge is 1.5% and the currency only moves by 1%, you've effectively paid for protection you didn't need.

A currency neutral approach works well for conservative investors who want their returns to reflect purely the performance of the underlying assets. It removes the "noise" of the FX market. However, for those with a longer horizon, staying unhedged can actually serve as a diversification tool. It allows your portfolio to breathe with global market cycles and can provide a cushion when the local economy faces headwinds.

When to Choose Hedged Share Classes

Hedged share classes are often the right fit for fixed income and bond portfolios. Because bond yields are typically lower than equity returns, a sudden 4% swing in the exchange rate could easily swallow your entire annual coupon. Hedging is also vital for short term goals. If you need your funds within the next three to five years, you can't afford a sudden SGD spike to erode your capital. At i12 investments, we frequently employ hedged structures for clients focused on wealth protection. This ensures that your capital remains stable in local terms, regardless of the volatility in global currency markets.

The Case for Staying Unhedged

Long term equity investors often have the luxury of time. Historical data suggests that over 20 year periods, currency fluctuations tend to mean-revert, meaning they often balance out. Staying unhedged is also a strategic move if you have future liabilities in foreign currencies. If you are planning for education funding for a child headed to London or New York, holding unhedged GBP or USD assets is a natural way to match your future costs without incurring hedging fees.

Academic insights into Singapore's Exchange Rate Policy highlight how the MAS manages the SGD for long term stability. This managed float gives long term investors the confidence to hold global assets without excessive fear of total currency collapse. A financial consultant can help you weigh these hedging costs against your specific timeline. They'll ensure your strategy aligns with your overall goals for retirement planning or legacy planning without letting unnecessary costs eat into your potential gains.

5 Practical Strategies for Managing FX Volatility in 2026

Protecting your global wealth requires more than just watching the news. It takes a disciplined approach to maintain your purchasing power. Here are five practical strategies for managing currency risk in investment portfolio Singapore as we move through 2026.

- Strategy 1: Strategic Asset Allocation. We use the i12 investments framework to balance regional exposure. This ensures you aren't over-concentrated in a single currency zone.

- Strategy 2: Currency Diversification. Don't rely solely on the USD. Holding a basket of G10 currencies can reduce your dependency on any single economy's performance.

- Strategy 3: Dollar-Cost Averaging (DCA). Investing fixed amounts at regular intervals helps smooth out your entry prices. This naturally averages your exchange rate costs over time.

- Strategy 4: Utilizing SRS for Global Assets. Your Supplementary Retirement Scheme (SRS) offers tax advantages, but investing it in foreign-denominated ETFs requires careful FX planning.

- Strategy 5: Regular Portfolio Rebalancing. Discipline is key. Trim your winners in strong currency zones and reinvest in undervalued areas to maintain your target risk profile.

Implementing the i12 Investments Framework

i12 investments is a structured approach to multi-asset wealth management. This framework prioritizes risk-adjusted returns by looking beyond simple stock picking. Our team provides professional oversight to monitor how a potential fed rate cut might impact the USD/SGD exchange rate. By staying proactive, we help you adjust your hedges before volatility strikes. This level of coordination is essential for successful investment management and long term wealth protection.

Managing FX Risk in Your SRS and CPF Portfolios

Investing your SRS funds into US-denominated ETFs presents unique challenges. While the growth potential is high, the conversion costs and translation risk can eat into your retirement nest egg. It's helpful to use a cpf retirement payout calculator to determine your guaranteed SGD-income floor first. Once you know your basic needs are met in local currency, you can take more calculated currency risks with your SRS or cash investments. A practical tip is to match your passive income currency to your expected retirement spending currency. If you plan to retire in Singapore, ensure a significant portion of your cash flow remains SGD-neutral. If you're ready to optimize your retirement strategy, speak with a financial planner to build a custom multi-currency plan.

Partnering with a Financial Consultant for Multi-Currency Wealth

Managing currency risk on your own often leads to emotional fatigue. It's easy to get distracted by daily headlines or sudden market shifts. This often results in costly errors, such as panic selling during a temporary USD dip or over-hedging when transaction costs are at their peak. For most retail investors, the spreads and fees associated with DIY currency management can quietly erode your returns. Partnering with a professional gives you access to institutional-grade insights that aren't always available to the public. This collaborative approach is essential for successfully managing currency risk in investment portfolio Singapore.

At Zenith Wealth, we don't view currency in isolation. We integrate FX strategy into your holistic retirement planning singapore. This ensures your global assets support your local lifestyle goals without unnecessary exposure. Your next step should be a "Currency Audit." We'll review your current holdings and identify where you might be over-exposed to exchange rate volatility.

The Value of Professional Advice in 2026

Monitoring MAS policy shifts requires constant vigilance. A financial consultant singapore tracks the S$NEER slope and its implications for your specific portfolio. Beyond the technical data, we provide a steady hand. We help you stay disciplined during periods of market stress, preventing the knee-jerk reactions that often derail long term wealth protection. Our team is ready to help you optimize your global exposure. Book a consultation with Zenith Wealth to start your portfolio review today.

Customising Your Risk Management Roadmap

Every investor's "Currency Comfort Zone" is different. Your strategy should reflect your unique timeline and future needs. We tailor our approach by linking your currency exposure to specific goals like education funding or legacy planning. If you're building a legacy for family members living abroad, your needs will differ significantly from someone focused purely on local spending. The i12 investments framework provides the structure needed to balance these competing priorities. Remember, currency is a tool for growth, not just a risk to be feared. Let's work together to ensure your multi-currency wealth is a source of strength for your future.

Secure Your Global Gains for the Years Ahead

Global markets offer immense opportunity, but they shouldn't come at the cost of your peace of mind. By aligning your strategy with the MAS managed float and choosing the right hedging frameworks, you can turn exchange rate shifts into a calculated advantage. We've explored how understanding the S$NEER and using tools like i12 investments can provide the stability your wealth deserves. Successfully managing currency risk in investment portfolio Singapore is no longer a guessing game when you have a structured roadmap in place.

Zenith Wealth is here to help you navigate these complexities with quiet confidence. Our financial consultants are authorised representatives of finexis advisory and bring specialised expertise in MAS regulatory environments. We focus on the i12 investments framework to ensure your retirement and legacy plans remain resilient against volatility. It's time to move from uncertainty to clear, actionable strategy. We're ready to start the conversation whenever you are.

Secure your global portfolio today; speak with a Zenith Wealth financial consultant. We look forward to helping you protect your wealth and grow with confidence.

Frequently Asked Questions

How does a strong Singapore Dollar affect my US stock investments?

A strong SGD reduces the value of your US holdings when they are converted back to your home currency. Even if your US stocks rise in price, a simultaneous appreciation of the Singapore dollar can eat into those gains. This is the core challenge of managing currency risk in investment portfolio Singapore. It effectively creates a headwind for your total returns in local terms.

Is it better to buy the SGD-hedged or USD version of a fund?

There is no single right answer, as it depends on your specific time horizon and goals. SGD-hedged funds remove exchange rate volatility but involve additional hedging costs. USD versions allow you to benefit if the US dollar strengthens but expose you to losses if it weakens. A financial planner can help you evaluate these trade-offs based on your retirement planning needs.

Does the MAS exchange rate policy predict future interest rate movements?

The MAS manages the exchange rate rather than interest rates, so there is no direct prediction. However, Singapore's interest rates, like the Singapore Overnight Rate Average (SORA), are heavily influenced by global trends and the MAS stance. As of May 28, 2026, the 3-month compounded SORA is 1.06450%. This reflects the broader liquidity environment shaped by our unique monetary policy.

Can I use my SRS account to invest in foreign currency assets?

Yes, you can use your Supplementary Retirement Scheme (SRS) funds to access global markets through approved investment platforms. While this provides great diversification, you must account for the conversion fees and translation risk. Since your SRS withdrawals will eventually be in SGD, managing currency risk in investment portfolio Singapore is vital to ensure your future purchasing power remains intact.

How often should I rebalance my portfolio to manage currency risk?

Most investors find that a semi-annual or annual review is sufficient to maintain their target risk levels. Rebalancing more frequently can lead to high transaction costs and emotional decision making. A regular schedule allows you to trim assets in overperforming currency zones and reinvest in undervalued areas. This disciplined approach is a cornerstone of effective investment management and wealth protection.

What happens to my global portfolio if the US Fed cuts interest rates in 2026?

A US Fed rate cut generally puts downward pressure on the US dollar. If this happens, your US-denominated assets may lose value when measured in SGD. This is particularly relevant as the MAS continues its policy of gradual SGD appreciation to combat the 1.5% to 2.5% inflation forecast for 2026. We monitor these global shifts to help you adjust your hedges proactively.

What are i12 investments and how do they help with risk management?

i12 investments is a structured framework designed for multi-asset wealth management and stability. It focuses on achieving risk-adjusted returns by diversifying across different geographic regions and currency zones. By using this framework, a financial consultant can help you build a portfolio that is less dependent on any single currency. This provides a more reliable path for legacy planning and long term growth.

Should I worry about the MAS exchange rate if I only invest in the STI?

Yes, because many companies in the Straits Times Index (STI) are global players with significant overseas operations. Even if you buy shares in SGD, the underlying profits of these companies are often earned in foreign currencies. A strong SGD can make their overseas earnings look smaller when reported in their financial statements. Currency volatility impacts almost every asset class, even those listed locally.