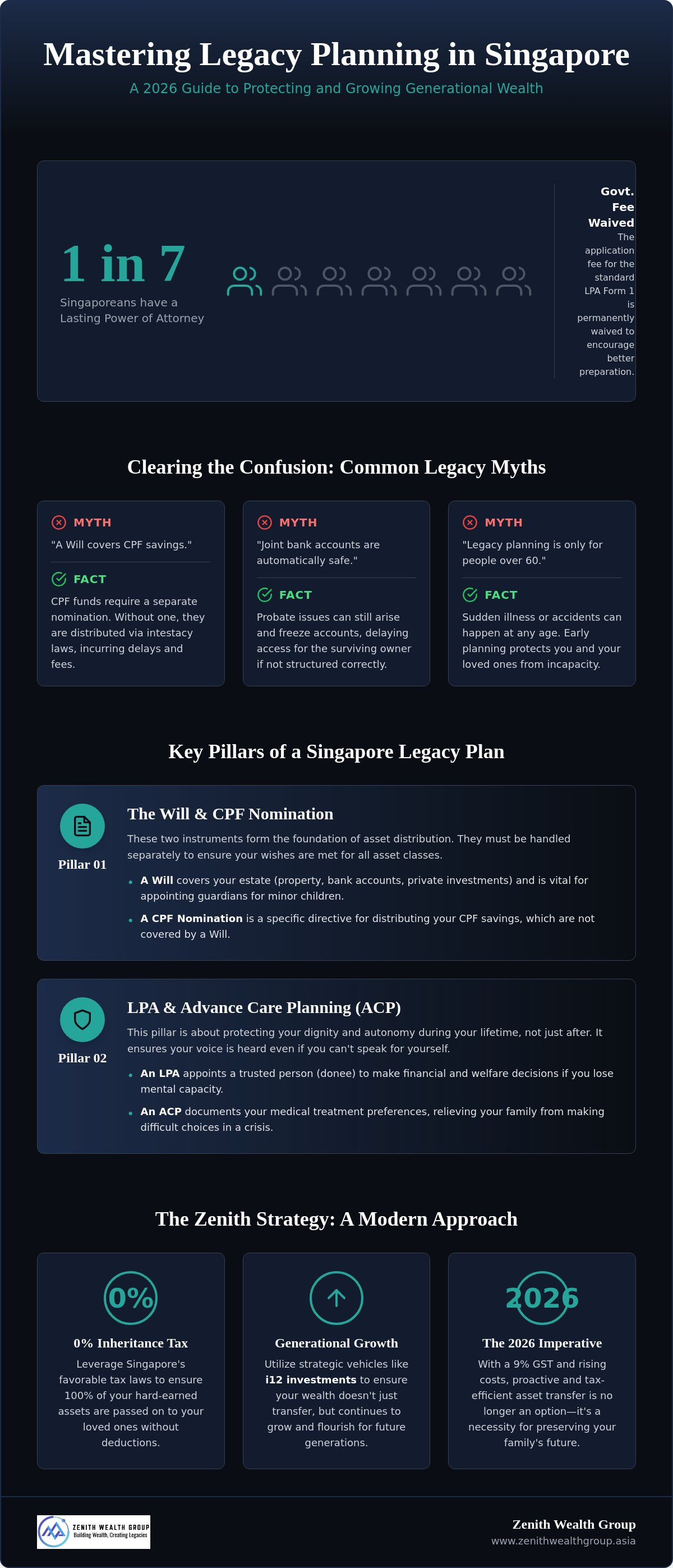

Did you know that as of early 2026, only about one in seven Singaporeans has registered a Lasting Power of Attorney? It's a startling gap, especially since the government permanently waived the application fee for the standard LPA Form 1 to encourage better preparation. We know that legacy planning Singapore often feels like a daunting task. You might worry about potential family disputes or feel stuck between the complexities of Wills and CPF nominations.

It's natural to want a clear path that protects your loved ones without the stress of legal jargon. This guide promises to help you master the essentials of estate distribution and wealth preservation. We'll show you how to leverage Singapore's 0% inheritance tax and use i12 investments to keep your family's wealth growing. Our financial consultants have broken down everything you need to know to move from anxiety to total confidence in your family's future. We will explore the latest CPF retirement sums for 2026 and the strategic steps required to ensure a seamless, tax-efficient transfer of assets.

Key Takeaways

- Learn how a dual-track strategy for legacy planning Singapore balances legal protection with proactive generational wealth growth.

- Identify the four essential legal and financial pillars that safeguard your assets during incapacity and ensure smooth distribution.

- Discover how i12 investments serve as a strategic vehicle to ensure your wealth continues to flourish for future generations.

- Use our 2026 step-by-step roadmap to navigate CPF nominations and Wills with the guidance of a professional financial consultant.

- Understand how to leverage current 0% inheritance tax laws and LPA fee waivers to create a modern, tax-efficient estate plan.

What is Legacy Planning in the Singapore Context?

Many people think Legacy Planning is just a fancy term for writing a Will. In reality, it's a proactive process that ensures your assets are managed for your benefit if you lose mental capacity and then distributed smoothly to your heirs after you pass. For families here, legacy planning Singapore style is a unique blend of legal instruments, strict CPF regulations, and strategic private investment vehicles. It's about taking control before life takes the choice away from you. Legacy planning in 2026 is a holistic strategy that combines legal protection with wealth growth to ensure Singaporean families thrive across multiple generations.

Don't let the term "generational wealth" intimidate you. This isn't just a service for the ultra-high-net-worth crowd. If you have a bank account, a CPF balance, or dependents who rely on your income, you have a legacy. It's about protecting what you've worked hard to build, regardless of the size of your portfolio. By working with a financial planner, you can ensure that your hard-earned assets don't get tied up in legal limbo.

Why 2026 is the Year to Start Your Plan

The landscape is changing fast. With the GST rate at 9% and rising costs of living, ensuring a tax-efficient transfer of assets is now a necessity. The government has made things easier with the MyLegacy portal, but digital tools can't replace a strategic conversation. We're also seeing a shift in how people view their money. It's no longer just about "emergency savings" for yourself; it's about building a foundation through i12 investments so your children start their journey on solid ground. Starting now gives your investments more time to compound and grow.

Common Misconceptions About Singapore Estate Law

Clearing up confusion is the first step toward peace of mind. Here are three myths we often hear:

- Myth: Your Will covers your CPF savings. It actually doesn't. Your CPF funds are distributed based on your CPF nomination. Without one, the Public Trustee distributes the funds according to intestacy laws, which takes longer and costs more.

- Myth: Joint bank accounts automatically transfer to the survivor. While often true, probate issues can still freeze accounts if the right clauses aren't in place.

- Myth: Legacy planning is only for those over 60. Life is unpredictable. Setting up your plan early ensures you are protected against sudden incapacity, such as a stroke or accident, at any age.

If you're feeling unsure about where your assets currently stand, it's a great time to start a conversation. You can reach out to a financial consultant to begin mapping out your family's future today.

The 4 Essential Pillars of a Singapore Legacy Plan

A truly effective strategy for legacy planning Singapore isn't built on a single document. It requires four distinct pillars working in perfect harmony to cover every stage of your journey. These pillars don't just dictate what happens after you're gone; they protect your dignity and your assets while you're still here. By structuring these elements correctly, you eliminate the ambiguity that often leads to painful family disputes. When everyone knows the plan, there's no room for conflict. It's about providing a clear roadmap that leaves nothing to chance.

A financial planner plays a vital role in this process. They ensure your legal documents align with your broader wealth strategy, including growth vehicles like i12 investments. Without this alignment, your legal wishes might not match your financial reality. It's one thing to have a Will; it's another to ensure the assets you're leaving behind have been managed to reach their full potential.

1. The Will and CPF Nomination

Many Singaporeans mistakenly believe a Will covers everything. It doesn't. Your CPF savings are not part of your estate and cannot be distributed via a Will. You must make a specific CPF nomination to specify who receives your balances. If you don't, the Public Trustee's Office distributes your funds according to intestacy laws, but they'll charge administration fees that eat into your family's inheritance.

A Will remains essential for your other assets, such as property, bank accounts, or private investments. It's also the primary tool for protecting minors. You can use a Will to appoint guardians and set up testamentary trusts, ensuring your children are cared for by people you trust. You can manage these records and view your status through the MyLegacy@LifeSG portal, which helps keep your legal life organized in one digital space.

2. Lasting Power of Attorney (LPA) and Advance Care Planning (ACP)

Legacy planning isn't only about death. It's about protecting yourself during your lifetime. The LPA allows you to appoint a "donee" to make decisions about your personal welfare and finances if you lose mental capacity. In 2026, this is a critical document for young parents and sandwich-generation professionals. It ensures that if an accident or illness occurs, a trusted person can access funds to pay for your family's needs without a costly and slow court order.

Advance Care Planning (ACP) complements the LPA by documenting your medical preferences. It's a gift to your family. It removes the heavy burden of making difficult medical choices during a crisis because your wishes are already known. These two pillars ensure your voice is heard even when you can't speak for yourself. Building these pillars is a collaborative, human process. If you're ready to start, a financial consultant can help you navigate the options and ensure your plan is airtight.

Beyond the Basics: Integrating i12 investments for Growth

Effective legacy planning Singapore style involves more than just signing legal papers. While Wills and LPAs provide the necessary legal structure, they don't address the most critical question: what exactly are you leaving behind? A robust plan must focus on wealth creation and preservation as much as distribution. Without a strategy for growth, inflation can quietly erode the value of your estate before it even reaches your heirs. This is where i12 investments become a vital part of your generational wealth strategy.

Your financial planner can help you move beyond simple savings toward a sophisticated investment mix. By integrating i12 investments, you ensure that your assets aren't just sitting idle. Instead, they're actively working to build a larger foundation for your children and grandchildren. We view this as the "fuel" for your legacy engine. It's about ensuring that the wealth you've built doesn't just last for your lifetime, but continues to flourish long after the transfer is complete.

Combating Inflation in Your Estate Plan

Leaving large sums of cash in a standard bank account is a risky legacy strategy in 2026. With the GST rate at 9% and persistent core inflation, the purchasing power of idle cash drops every year. To protect your family's future, your assets need to outpace these rising costs. Strategic use of i12 investments allows you to target returns that stay ahead of inflation while maintaining a risk profile that matches your family's long-term needs. A balanced approach ensures you aren't just saving money; you're growing a sustainable source of support for the next generation.

Bridging Government Tools with Private Wealth

Your private investment portfolio doesn't exist in a vacuum. It must interact seamlessly with your Will and other legal tools. One often overlooked factor is liquidity. When an individual passes away, bank accounts and properties can be frozen during the probate process, which can take several months. By structuring your i12 investments correctly, you can ensure your family has access to necessary cash flow during this transition period.

This coordination prevents your loved ones from facing financial strain while waiting for the legal system to process your estate. It's a human-centric approach to finance that prioritizes the immediate well-being of your heirs. If you want to dive deeper into how to shield your assets from external risks, Learn more about Wealth Protection in Singapore. Combining these growth strategies with legal safeguards creates a complete, airtight plan that stands the test of time.

Your 2026 Legacy Planning Checklist

Executing a strategy for legacy planning Singapore doesn't have to be an overwhelming ordeal. It's a journey that begins with a few decisive, manageable steps. Many families stall because the process feels too large, but breaking it down into specific phases makes it achievable. This checklist serves as your roadmap to move from uncertainty to full protection. It's about building a secure foundation that adapts as your life evolves. To keep your strategy effective, you must review your complete legacy plan every three to five years. This ensures your wishes stay aligned with new life milestones, such as marriage, the birth of a child, or significant shifts in your investment portfolio.

Working with a financial planner during this process provides the professional oversight needed to avoid common pitfalls. They help ensure your legal documents and financial assets work as a single, cohesive unit. This proactive approach prevents the administrative delays that often plague unplanned estates. Let's look at the specific actions you can take right now to secure your family's future.

Immediate Actions: The First 30 Days

The first month is all about clarity and baseline protection. You can't plan for the future if you don't have a clear picture of your current standing. Start by performing a comprehensive asset audit. This includes documenting your bank accounts, property holdings, and your current i12 investments. Having this data in one place is a gift to your future self and your heirs.

Next, use the Office of the Public Guardian (OPG) online portal to file your Lasting Power of Attorney. In 2026, the application fee for the standard LPA Form 1 remains permanently waived for Singapore citizens, making this an essential and cost-effective first step. Finally, log into your CPF account to verify your nomination status. Life changes often happen faster than our paperwork; ensure your beneficiaries reflect your current intentions so your funds don't end up with the Public Trustee.

Strategic Actions: The Next 90 Days

Once the basics are settled, focus on the long-term structure of your wealth. Schedule a session with a financial planner to draft or update your Will. They'll help you coordinate your Will with your CPF nomination and your private growth vehicles, ensuring nothing is left to chance. This is also the time to align your insurance policies with your legacy goals. The focus here is liquidity. You want to ensure your family has immediate access to cash for daily expenses while your estate moves through the probate process. For a deeper look at how your legacy fits into your broader life goals, Read our guide on Retirement Planning in Singapore.

Taking these steps transforms your plan from a "someday" task into a completed mission. If you're ready to cross these items off your list with professional support, reach out to a financial consultant at Zenith Wealth to start your personalized audit today.

Why Partner with a Zenith Wealth Financial Consultant?

Legacy planning Singapore is often treated like a series of cold, digital forms. While government portals provide the necessary infrastructure, they can't handle the nuances of your family's unique story. At Zenith Wealth, we believe this process is a human conversation first. Our financial consultants offer a welcoming, open-door approach to topics that others might find heavy or complex. We're here to listen. We want to understand your fears and your aspirations before we even look at the numbers. This personal touch ensures your plan reflects your heart, not just your assets.

As authorized representatives of finexis advisory, we provide holistic advice that bridges the gap between legal requirements and private wealth growth. We don't just look at where your money goes; we look at how it gets there and how it grows along the way. Effective legacy planning Singapore style requires leveraging strategic insights and vehicles like i12 investments to build a foundation that lasts. Our role is to act as your modern professional guide. We simplify the complex landscape of estate laws while keeping your long-term growth on track. We offer the reliability of a large institution with the attentive care of a boutique firm.

Tailored Solutions for Every Life Stage

Life doesn't stand still. Young parents might focus on securing their children's future through education funding and wealth protection. Pre-retirees often prioritize lifestyle preservation and tax-efficient asset transfer. Our boutique approach means we integrate your career growth and specific family goals into your legacy. Unlike cold, institutional corporate advisory firms, we value personal connection. We grow alongside you. We adjust your roadmap as your circumstances change. Whether you are managing a growing portfolio of i12 investments or just starting to look at your CPF nominations, we provide the specific expertise you need for your current life stage.

Start Your Conversation Today

Legacy planning is the ultimate gift to your loved ones. It's the difference between leaving a legacy of clarity or a legacy of confusion. Don't leave your family's future to chance or the default rules of intestacy. Our team is ready to help you create a personalized wealth roadmap that covers everything from your legal documents to your investment strategy. We believe in proactive engagement and straightforward communication. There's no jargon here. Just clear paths to a secure future.

We invite you to reach out and start this important dialogue in a comfortable, professional setting. It's time to move from "planning to plan" to having total peace of mind for your family. Contact Zenith Wealth to start your legacy plan and discover how we can help you protect and grow your generational wealth.

Build Your Generational Foundation Today

Effective legacy planning Singapore is more than a one-time legal chore; it's a living foundation for the people you love most. We've explored how the right legal pillars protect your dignity and ensure your wishes are respected during incapacity. By integrating strategic growth through i12 investments, you also ensure that your hard-earned wealth outpaces inflation to benefit future generations. This dual-track strategy transforms a static estate into a dynamic engine for generational growth, providing your family with lasting security.

At Zenith Wealth, we act as authorized representatives of finexis advisory to offer you professional, holistic guidance. We move past the institutional jargon to provide a welcoming, human-centered approach to your finances. Our team is ready to help you navigate these complex decisions with confidence and clarity. Secure your family’s future—connect with a Zenith financial consultant today. Let's start building a legacy that reflects your values and protects your loved ones for years to come.

Frequently Asked Questions

Do I really need a Will if I have a CPF nomination in Singapore?

Yes, because your CPF nomination only covers your CPF savings. Other assets like your family home, bank accounts, and private investment portfolios aren't included in that nomination. Without a Will, these remaining assets are distributed according to the Intestate Succession Act, which may not align with your personal wishes. It's a key part of legacy planning Singapore to have both in place to ensure all your properties transition smoothly.

What happens to my i12 investments if I lose mental capacity?

If you lose mental capacity, your i12 investments could be frozen unless you have a Lasting Power of Attorney (LPA) registered. Your appointed "donee" would then have the legal authority to manage these assets on your behalf. Without an LPA, your family might need to apply for a court order to access your portfolio. This is often a slow and expensive process that adds stress during a medical crisis.

How much does it cost to set up a Lasting Power of Attorney (LPA)?

For Singapore citizens, the application fee for the standard LPA Form 1 is permanently waived as of 2026. If you require the more complex LPA Form 2, the application fee was lowered to S$30 in May 2026. You'll still need to pay a fee to a certificate issuer, such as a doctor or lawyer, to witness and certify your application. This remains one of the most cost-effective ways to protect your future.

Can a financial consultant in Singapore help with my Will?

A financial consultant can't draft the legal document for you, but they play a critical role in the strategy behind it. They help you audit your assets, including your i12 investments, to ensure your Will aligns with your broader financial goals. Once the strategy is clear, they can refer you to a legal professional to formalize the document. This ensures your financial and legal plans work together perfectly.

What is the difference between legacy planning and estate planning?

Estate planning is primarily about the legal distribution of your assets after death. Legacy planning Singapore takes a broader approach by including your care during incapacity and the long-term growth of your wealth. It's a holistic strategy that ensures your values and wealth flourish across generations. We use tools like i12 investments to outpace inflation and provide a sustainable foundation for your heirs even after the assets are transferred.

Is legacy planning only for the elderly or high-net-worth individuals?

No, it's for anyone with a bank account, CPF savings, or loved ones who depend on them. Young parents especially need a plan to appoint guardians and manage assets if something happens early in life. Whether you're just starting your career or managing a significant portfolio, having a clear roadmap ensures your family is protected. You don't need a massive estate to start protecting what you have.

How often should I review my legacy plan in 2026?

You should review your plan every three to five years or whenever a major life event occurs. Marriage, the birth of a child, or a significant inheritance can all change your priorities. Regular check-ins with your financial planner ensure that your nominations and investment strategies remain relevant. We make sure your i12 investments and legal documents stay aligned with the 2026 economic landscape and your current family situation.