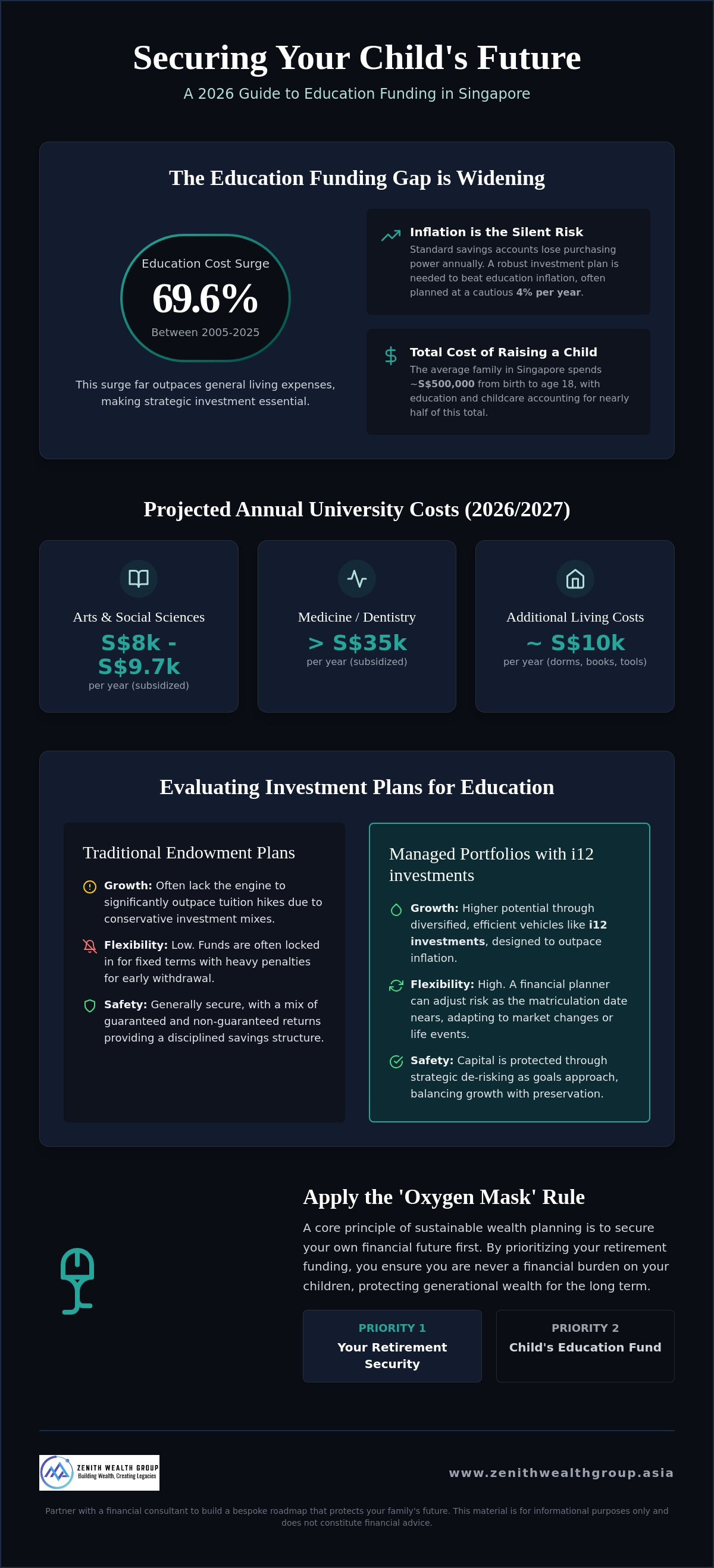

Between 2005 and 2025, the cost of education in Singapore surged by 69.6%, far outstripping the general rise in living expenses. This reality leaves many parents wondering if their current investment plans for child education Singapore are actually enough to keep pace. You want to provide every opportunity for your child, yet the fear of over-saving for tuition while neglecting your own retirement is a constant, quiet pressure.

It's a delicate balance to strike. You likely feel that a university degree is essential but increasingly expensive to fund. We're here to help you secure that future. This 2026 guide reveals how to build a robust fund that beats inflation while keeping your retirement goals on track. You'll discover clear dollar targets for local tuition, the strategic role of i12 investments in a diversified portfolio, and how a financial consultant can help protect your family's wealth against the unexpected. Let's start a conversation about securing your child's legacy today.

Key Takeaways

- Identify the latest tuition fee projections for NUS, NTU, and SMU to calculate your specific funding gap for 2026 and beyond.

- Compare the most effective investment plans for child education Singapore offers today to ensure your strategy stays ahead of rising inflation.

- Discover how i12 investments provide the global diversification necessary to build a resilient and growth-oriented portfolio.

- Learn to apply the 'Oxygen Mask' rule so you can fund your child's university years without compromising your own retirement security.

- Understand the value of partnering with a financial planner to create a bespoke roadmap that protects your family's generational wealth.

The Reality of Education Costs in Singapore: 2026 Update

The Education Gap isn't just a abstract concept. It's the very real difference between what's in your bank account today and what your child will need for university in 2026 and beyond. In Singapore, the average family spends about S$500,000 to raise a child from birth to 18. Education and childcare alone account for nearly half of that total. This gap widens every year that your funds remain stagnant.

For the 2026/2027 academic year, tuition fees at local autonomous universities reflect a steady climb. Arts and Social Sciences students can expect to pay between S$8,000 and S$9,700 annually. Those pursuing Medicine or Dentistry face much steeper costs, often exceeding S$35,000 per year. These figures represent the subsidized rates within Singapore's education system, yet they still present a significant hurdle for many families. You must also factor in the cost of living. On-campus dorms, specialized digital tools, and textbooks can easily add another S$10,000 to your annual budget.

Inflation is the silent killer of traditional savings. While the average education inflation rate has historically hovered around 2.68%, many parents now plan for a 4% surge to remain safe. Relying solely on a standard bank savings account often means losing purchasing power every single year. You need robust investment plans for child education Singapore to bridge this widening gap and ensure your child's future is secure.

Local vs. Overseas: The $200,000 Dilemma

Choosing between a local degree and an overseas education is a massive financial pivot. A local medical degree is already a six-figure commitment. If your child heads to the UK or US, that budget can easily double or triple. You must account for MAS exchange rate fluctuations, which can swing your total costs by 10% or more in a single year. Don't forget the "invisible" expenses. Student visas, international health insurance, and emergency travel funds often add S$15,000 to S$20,000 to the total bill. A financial consultant can help you model these scenarios accurately.

Why 'Savings' Aren't Enough in 2026

Fixed deposits and standard savings accounts can't keep up with 2026 costs. If you have a 15 or 20-year horizon, you're looking at an investment challenge, not a savings goal. An Education Fund is a purpose-driven investment portfolio designed to outpace inflation while protecting capital as the matriculation date nears. This is where i12 investments play a crucial role. They offer a strategic way to seek growth beyond local markets through a diversified approach. Moving from a "savings" to an "investment" mindset is the first step toward closing the Education Gap. We invite you to connect with us to begin building your bespoke roadmap.

Evaluating Investment Plans for Child Education: A 2026 Comparison

Selecting the right path requires more than just picking a product. Successful investment plans for child education Singapore are built on three non-negotiable pillars: safety, growth, and flexibility. Safety ensures the core capital is there when the first tuition bill arrives. Growth ensures that capital hasn't been eroded by the 4% inflation mentioned earlier. Flexibility allows you to pivot if your child secures a scholarship or decides on a different path. When planning for your child's future education, you'll likely encounter traditional endowment plans and Investment-Linked Policies (ILPs). Both have their place, but they serve different temperaments.

Endowment plans offer a disciplined savings structure with a mix of guaranteed and non-guaranteed returns. In the high-interest-rate environment of 2026, these can feel secure, yet they often lack the "engine" needed to significantly outpace tuition hikes. ILPs, on the other hand, offer more market upside by combining insurance coverage with investment sub-funds. While they provide growth potential, they require active monitoring to ensure the insurance costs don't eat into your returns as you age. For the highly disciplined parent, a DIY approach using Unit Trusts or ETFs is an option, though it lacks the automated safety nets found in structured plans.

Endowment Plans vs. Managed Portfolios

The "lock-in" is the biggest hurdle for traditional endowments. If your child wins a full scholarship, that money might still be tied up for years with heavy penalties for early withdrawal. Managed portfolios offer a more modern alternative. They allow a financial planner to adjust your risk profile as your child gets closer to university. This agility is vital in 2026's volatile markets. We believe in bespoke planning that prioritizes your family's specific timeline over "off-the-shelf" insurance products that may not fit your goals. If you're unsure which direction suits your family, you might find it helpful to speak with a financial consultant to clarify your options.

Direct Investing via i12 investments

Efficiency is the cornerstone of our approach. Our focus on i12 investments provides a structured framework for market growth without the unnecessary fluff. By utilizing low-cost, efficient investment vehicles, we aim to maximize the "net" return that actually goes into the education fund. You should always compare the Total Expense Ratio (TER) of any plan you consider. Even a 1% difference in annual fees can result in a five-figure gap in your final fund over a 15-year horizon. This focus on cost-efficiency ensures your hard-earned money works for your child, not the institution managing it.

Strategic Portfolio Construction with i12 investments

Building a fund isn't just about saving money. It's about where that money lives. At Zenith Wealth Group, i12 investments are the engine of our strategy. We don't believe in "set and forget" models. Your investment plans for child education Singapore need to be as dynamic as the 2026 global economy. Precision matters when you're targeting a specific date like a university enrollment year.

Singapore's market is stable, but your child's fund needs global growth. We look toward international markets to capture returns that local assets might miss. This isn't just about chasing high numbers. It's about spreading risk across different sectors and geographies. If one region slows down, another can pick up the slack. This global exposure is a core part of how we close the Education Gap we identified in previous sections. It ensures your portfolio isn't overly dependent on a single economy.

Time is your greatest ally. Over a 15 to 20 year horizon, compounding does the heavy lifting. Even modest, consistent contributions can snowball into a significant sum. Starting early isn't just a suggestion. It's a mathematical advantage. We help you map out this timeline with precision so you can see the long-term impact of your choices today.

The i12 investments Advantage for Parents

The core of our approach is alignment. We align your investment risk with your specific time-to-matriculation. If your child is five years old, we can afford to be more aggressive to capture higher growth. If they're fifteen, we prioritize stability. Our i12 investments framework adapts to 2026 market shifts in real-time. You won't be left wondering where your money is or how it's being used. We provide clear, transparent reporting so you can see exactly how your portfolio is performing. It's about quiet confidence and total clarity for your family's future.

Managing Volatility in the Final 5 Years

The "Glide Path" is essential as university approaches. You don't want a market crash to wipe out 20% of your fund just months before the first tuition bill. We gradually shift your portfolio from growth-oriented assets to capital preservation tools. This protects the gains you've made over the previous decade. By committing to regular, fixed contributions over time, dollar-cost averaging reduces the impact of short-term market volatility and lowers the average cost per unit of your investments. This disciplined approach removes the stress of trying to "time the market." If you want to see how a financial consultant can tailor this strategy for your family, let's start a conversation.

Balancing Education Funding with Retirement Planning

Many parents in Singapore find themselves caught in the 'Sandwich Generation' trap. You're balancing the needs of aging parents with the rising costs of your child's future. It's a heavy load to carry. At Zenith, we advocate for the 'Oxygen Mask' rule. You must secure your own retirement first. Your child can take a loan for university, but nobody will lend you money for your retirement. A financial consultant helps you navigate this tension without the guilt.

Using CPF can be a strategic move if managed correctly. You can use up to 40% of your accumulated Ordinary Account savings for tuition fees. This provides a helpful safety net, but remember it's a loan that carries a 2.5% interest rate. Repayment starts one year after graduation and can last up to 12 years. Your investment plans for child education Singapore should work alongside these government schemes to reduce the long-term debt burden on your child.

Is it Possible to Fund Both?

Integrated wealth modeling is the key to seeing how your goals interact. You'll often discover that retirement planning and education funding share the same growth engine. We utilize i12 investments to provide the necessary momentum for both. It's about making informed trade-offs. You might decide on a local university to ensure a robust retirement fund. Or, if the data aligns, you can confidently fund an overseas STEM degree. A financial planner provides the clarity needed to make these choices with confidence.

Wealth Protection for Young Parents

Your plan is only as strong as its protection. If the breadwinner can't work, the education fund must survive. Term Life and Critical Illness insurance are foundational, not optional. Payor waivers are especially valuable for parents. They ensure that your investment plans for child education Singapore continue even if you face a major health crisis. Our wealth protection guide goes deeper into these essential safeguards. Don't leave your child's future to chance. Connect with a financial planner today to build a plan that protects everyone you love.

Your Roadmap: Working with a Financial Planner

A financial planner provides more than just a product brochure. They offer a strategic partnership. Traditional services often focus on selling a specific insurance policy or endowment. We believe your family deserves better. We look at the entire landscape of investment plans for child education Singapore. This ensures your strategy is built on data, not just a sales pitch. It's about finding the most efficient way to reach your goals.

The Zenith 'Modern Professional' approach is different. We prioritize human interaction. We're a boutique firm that values personal connection over corporate coldness. During your first discovery session, we focus on your story. We'll help you define your targets and audit your current progress. You'll walk away with a clear understanding of your 'Education Gap' and a plan to close it. This is a conversation, not a lecture.

Your plan shouldn't be static. Markets shift. Life happens. A strategy designed today may need adjustments in five years. Regular reviews are essential to keep your fund on track. We'll help you monitor your progress and make proactive changes when needed. This ensures you're always moving toward your goal with confidence. We're ready to engage and grow alongside your family.

The 5-Step Education Planning Checklist

- Step 1: Define the target. Decide on the likely degree and location. This sets your dollar-target for 2026 and beyond.

- Step 2: Audit your current path. Look at your bank balances, existing insurance policies, and CPF accounts. Know where you stand today.

- Step 3: Select the right engine. Choose between traditional endowments, ILPs, or the growth potential of i12 investments. We help you find the right balance of safety and upside.

- Step 4: Automate the process. Set up regular contributions. This removes the temptation to spend and uses dollar-cost averaging to your advantage.

- Step 5: Secure the future. Add wealth protection layers. Ensure the fund continues even if you face an unforeseen health event.

Start Your Journey with Zenith Wealth Group

We invite you to connect with us. Preparing for your first meeting is simple. Bring your current financial statements and a clear idea of your child's potential path. Don't worry if you don't have all the answers yet. That's what we're here for. Our financial consultants are ready to listen and help you build a bespoke roadmap. Let's secure your child's legacy together. We're excited to start this conversation with you. Schedule a consultation with a Zenith financial planner today.

Secure Your Child's Generational Wealth

Closing the Education Gap requires a blend of foresight and action. You now understand the 2026 tuition landscape and the importance of selecting investment plans for child education Singapore that outpace inflation. By integrating tailored i12 investments and prioritizing wealth protection, you can fund your child's dreams while keeping your own retirement on track. It's about building a legacy that lasts for generations.

As authorized representatives of finexis advisory, we take a holistic approach to your family's future. We don't just look at numbers; we look at the people behind them. You deserve a partner who values personal connection as much as professional integrity. Let's turn these insights into a concrete roadmap for your family. Our team is ready to help you navigate the complexities of 2026 with quiet confidence and clarity.

Secure your child's future today. Connect with a Zenith financial planner. We're ready to start the conversation whenever you are. Your child's future is bright, and we're here to help you keep it that way.

Frequently Asked Questions

Can I use my CPF to pay for my child's university education in Singapore?

Yes, you can use the CPF Education Loan Scheme to pay for tuition at approved local institutions. You're allowed to withdraw up to 40% of your Ordinary Account savings for this purpose. Keep in mind that your child must repay the principal plus the 2.5% accrued interest starting one year after graduation. A financial consultant can help you determine if this is the most cost-effective path for your family.

How much should I be saving monthly for a child's education in 2026?

The amount depends on whether you target a local degree or overseas studies. With 2026 NUS tuition fees starting around S$8,000 annually for general degrees, many parents aim for a total fund of at least S$150,000 per child to cover tuition and living costs. We recommend reverse-engineering this goal based on your child's current age. This ensures your monthly contributions are realistic and sustainable over the long term.

What is the difference between an education endowment and an ILP?

An education endowment focuses on capital preservation with a mix of guaranteed and non-guaranteed returns. In contrast, an Investment-Linked Policy (ILP) offers higher growth potential by investing in sub-funds but includes insurance costs that may increase over time. Choosing the right one depends on your risk appetite for investment plans for child education Singapore. Both options require a disciplined approach to see the best results.

Is it better to invest in a 529 plan or a Singapore-based education fund?

Singapore-based families should prioritize local instruments like the Child Development Account (CDA) and the Post-Secondary Education Account (PSEA). 529 plans are specific to the US tax system and offer little benefit to those living in Singapore. Instead, consider i12 investments to gain global market exposure while remaining within the local regulatory framework. This approach maximizes your tax efficiency and government matching grants.

What happens to my education investment if my child gets a full scholarship?

If your child secures a scholarship, the outcome depends on your chosen vehicle. Traditional endowments often have rigid lock-in periods and surrender penalties. However, a diversified portfolio focused on i12 investments provides the flexibility to repurpose those funds for your child's first home or your own retirement without heavy fees. It's a great "problem" to have, provided your plan allows for such a pivot.

Should I prioritize my retirement or my child's education fund?

You should prioritize your retirement first to avoid becoming a financial burden on your children later. This is the "Oxygen Mask" rule of financial planning. Your child can access the CPF Education Scheme or study loans to fund their degree, but no bank will lend you money for your retirement lifestyle. A financial planner can help you model a plan that supports both goals without compromising your future security.

How do i12 investments fit into a child's education plan?

They serve as the primary growth engine for your portfolio. We use i12 investments to access global markets and keep management costs low. This ensures your capital works harder to beat the 4% education inflation rate we're seeing in 2026. By focusing on efficiency and transparency, you can build a more robust fund with the same monthly contribution. It's a modern approach to a traditional goal.

Is it safe to invest in equities for an education fund with only a 10-year horizon?

A 10-year horizon is generally sufficient for equity exposure, provided you have a clear "glide path" strategy. You should maintain a higher equity weight in the early years and gradually shift to safer assets as your child approaches age 18. This protects your gains from a sudden market downturn just before the first tuition bill arrives. Disciplined rebalancing is the key to managing this risk effectively.