Did you know that the Straits Times Index surpassed the 5,000 mark for the first time in February 2026? While this milestone highlights the strength of the local economy, many new PRs find themselves overwhelmed by the unique financial landscape. Understanding the best investment options for permanent residents in Singapore requires more than just picking stocks; it's about navigating a system designed with specific incentives and hurdles. From the 5% ABSD on your first home to the $15,300 annual SRS cap, the rules have changed since your days on an employment pass.

It's natural to feel a bit lost when trying to balance global market exposure with local requirements. You want to make your status work for you. We'll show you how to build wealth through a strategic triple-pillar integration of CPF, SRS, and private managed portfolios. This guide offers a clear roadmap for tax-efficient growth, leveraging private frameworks like i12 investments to bridge the gap. By the end, you'll know how to work with a dedicated financial planner to turn these complex regulations into a seamless, high-performing strategy that respects your new residency status.

Key Takeaways

- Understand how your new status transforms you from a temporary resident into a long-term stakeholder with exclusive access to tax-advantaged schemes.

- Master the "Triple-Pillar" strategy to optimize investment options for permanent residents in Singapore by integrating CPF, SRS, and private managed portfolios.

- Evaluate the real cost of property ownership against diversified financial assets, considering the 5% ABSD and potential opportunity costs.

- Explore how the i12 investments framework provides sophisticated PR investors with global exposure and professional management to counter inflation.

- Learn why partnering with a professional financial planner ensures your portfolio remains tax-efficient and balanced through every market shift.

Why PR Status Changes Your Investment Landscape in 2026

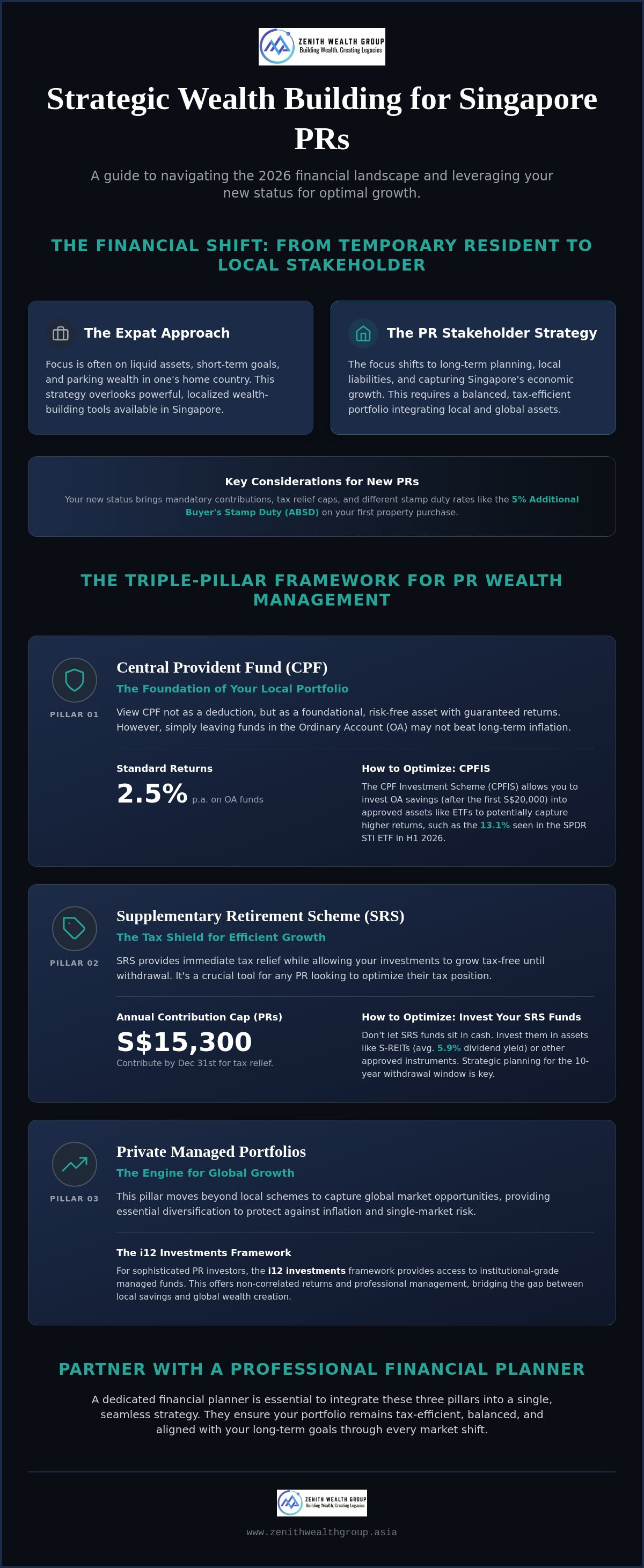

Securing your Permanent Residency is more than a legal milestone. It's a total shift in your financial identity. You've moved from being a temporary resident to a long-term stakeholder in one of the world's most stable economies. While some enter through the Global Investor Programme (GIP) by committing S$10 million or more, most residents gain status through professional and technical schemes. Regardless of how you arrived, your strategy must now pivot. You have gained access to exclusive investment options for permanent residents in Singapore that can significantly accelerate your wealth building.

Singapore offers a unique tax environment with no capital gains tax. This makes it an ideal base for compounding wealth over decades. However, the rules of engagement have changed. You now face mandatory contributions, specific tax relief caps, and different stamp duty rates. Managing these variables requires a proactive approach. It's about moving away from "expat" thinking and embracing a localized, yet globally diversified, strategy.

The Shift from Expat to Stakeholder

Your risk appetite often changes once you commit to staying. Expats typically keep their wealth liquid or parked in their home countries. As a PR, you start looking at local liabilities. You might be planning for a child's education at a local university or envisioning a long-term future here. In 2026, market conditions favour a more balanced approach. With the Straits Times Index reaching record highs, localising a portion of your wealth is no longer just about convenience. It's about capturing local growth. Relying solely on property isn't as efficient as it once was. The 5% Additional Buyer's Stamp Duty (ABSD) for your first purchase is a factor, but the opportunity cost of illiquid assets is the real concern. A financial planner can help you determine the right ratio of local to global assets.

Understanding the New Regulatory Benefits

The most significant change is your inclusion in the Central Provident Fund (CPF). Don't view this as a mere deduction. It is a foundational, risk-free asset with guaranteed returns that forms the bedrock of your local portfolio. You also gain full access to the Supplementary Retirement Scheme (SRS). For PRs, the annual contribution cap is S$15,300. This provides immediate tax relief while allowing your investments to grow tax-free until withdrawal. Within the i12 investments framework, we analyze how these local benefits integrate with your broader goals. You aren't just saving for retirement. You're optimizing every dollar. If you're ready to refine your strategy, connecting with a financial consultant is the first step toward maximizing your new status.

The Three Pillars of PR Wealth Management

Building wealth as a PR isn't about chasing a single "hot" asset. It's about constructing a robust structure that balances mandatory obligations with voluntary tax benefits. We call this the Triple-Pillar framework. It creates a powerful synergy between your local savings and global growth. While the Global Investor Programme (GIP) serves those entering with S$10 million or more, the majority of professionals rely on these three pillars to secure their future. Together, they act as both a safety net and a high-performance growth engine for your capital.

By mastering these investment options for permanent residents in Singapore, you ensure that every dollar is working toward a specific purpose. Your CPF provides the floor, your SRS provides the tax shield, and your private portfolios provide the ceiling for your wealth. Let's look at how to optimize each one for the 2026 market climate.

Optimising Your CPF for Investment

Your CPF is the bedrock of your local portfolio. However, leaving all your funds in the Ordinary Account (OA) at a 2.5% interest rate might not be enough to beat long-term inflation. The CPF Investment Scheme (CPFIS) allows you to deploy these funds into approved ETFs or unit trusts. While the 6-month T-bill yield sat at 1.50% in July 2026, many PRs use CPFIS to capture the 13.1% returns seen in the SPDR STI ETF during the first half of the year. In 2026, permanent residents can invest their Ordinary Account savings after setting aside S$20,000, or their Special Account savings after setting aside S$40,000.

Maximising SRS Tax Relief

The Supplementary Retirement Scheme (SRS) is a PR’s best friend for tax efficiency. You must contribute by the December 31st deadline to claim relief for that year. For PRs, the annual cap is S$15,300. Once the funds are in your SRS account, don't let them sit in cash earning nominal interest. You can invest in S-REITs, which offered average dividend yields of 5.9% in late 2025, or low-volatility funds. Planning for the 10-year withdrawal window is essential to ensure you minimize the tax impact when you eventually access your gains.

Cash Investments and Private Wealth

The third pillar involves moving beyond "safe" local assets to capture global market growth. This is where the i12 investments framework excels. It provides access to institutional-grade managed funds that offer non-correlated returns. This diversification is vital for protecting your wealth against US inflation or regional trade shifts. A qualified financial planner can help you select assets that complement your CPF and SRS holdings. If you're looking to elevate your strategy, a conversation with a financial consultant can help you integrate these private options into your broader roadmap.

Property vs. Financial Portfolios: A 2026 Comparison

For many, the Singapore dream is synonymous with owning private property. However, as a PR in 2026, the math has changed. You now face a 5% Additional Buyer's Stamp Duty (ABSD) on your first residential purchase. This is a significant upfront cost that doesn't exist for citizens. When evaluating investment options for permanent residents in Singapore, it's vital to look past the physical asset. Tying up millions in a single, illiquid condo can create a massive opportunity cost. While residential rental yields often hover around 2% to 3%, a diversified dividend-paying portfolio can offer much higher cash flow with far less hassle.

We are seeing a growing trend among savvy PRs: the "Rent where you live, invest where it grows" strategy. By renting your primary residence, you maintain the flexibility to move for career opportunities. Meanwhile, your capital is deployed into high-growth sectors. This approach allows you to bypass the heavy taxes and maintenance fees associated with local real estate ownership. It also ensures your wealth isn't overly concentrated in a single geographical market.

The Real Cost of Singapore Real Estate

Owning property isn't just about the mortgage. You must factor in property taxes, conservancy charges, and the impact of the MAS exchange rate on your global wealth. In the 2026 environment, interest rates remain a key variable for leveraged buyers. Property still makes sense if it's your primary home and provides emotional stability. However, for pure wealth accumulation, voluntary schemes like the Supplementary Retirement Scheme (SRS) often provide better tax-adjusted returns. A financial planner can help you model these costs to see if a mortgage truly fits your long-term roadmap.

The Liquidity Advantage of Financial Assets

Financial portfolios offer a level of agility that physical buildings cannot match. You can rebalance your holdings in minutes during market shifts. Through the i12 investments framework, you gain exposure to global tech, healthcare, and emerging markets. These are sectors that a local condo simply cannot reach. Legacy planning is also much simpler. It's easier to divide a managed fund among heirs than it is to split a physical apartment. If you want to explore more liquid alternatives, it's time to speak with an experienced financial consultant about your next steps.

Strategic Growth with i12 Investments and Managed Portfolios

While CPF and SRS provide a solid foundation, achieving true financial independence requires a sophisticated growth engine. Many professionals find that standard retail products don't offer the precision needed to navigate the 2026 market. This is where the i12 investments framework changes the conversation. It's a structured approach designed specifically for those who need more than just "average" returns. By moving beyond basic investment options for permanent residents in Singapore, you can access global trade shifts and hedge against US inflation with professional oversight. It's about being proactive rather than reactive.

The 2026 landscape demands an "active-passive" hybrid strategy. You've likely seen the Straits Times Index hit record highs, but relying solely on local indices can be risky. We combine the cost-efficiency of passive ETFs with the tactical agility of active management. This allows you to capture the 13.1% growth seen in local benchmarks while pivoting quickly when global volatility strikes. Your portfolio should be a reflection of your ambition, not just a collection of accounts.

Advanced Asset Allocation

Modern wealth management isn't just about diversification; it's about intelligent allocation. The i12 investments framework provides a clear structure for risk management by integrating ESG factors and thematic trends like green energy and AI infrastructure. This ensures your capital isn't just growing, but growing in the right directions. The i12 investments framework utilizes a proprietary layering technique to capture upside in burgeoning sectors while maintaining rigorous downside buffers for your capital. It's a balance of growth and protection that most DIY portfolios lack. A financial planner can help you identify which themes align with your personal values and risk tolerance.

Education and Legacy: Investing for the Next Generation

As a PR, you're likely thinking about more than just your own retirement. You're building a foundation for your family. This requires dedicated investment silos for future liabilities, such as university fees for children. Your status makes it easier to utilize Singaporean structures for Legacy Planning in Singapore, ensuring your wealth transitions smoothly to the next generation. By setting up these silos early, you protect your core retirement funds from being drained by education costs. Ready to see how i12 investments fits your 2026 goals? Connect with a financial consultant to start your transition today.

How a Financial Planner Elevates Your PR Investment Strategy

Managing your wealth solo often feels like a full-time job. While you now have access to diverse investment options for permanent residents in Singapore, the technical execution is where many stumble. DIY investing frequently leads to tax inefficiencies, especially when balancing SRS withdrawals or CPF allocations. A dedicated financial planner doesn't just pick products. They ensure your entire strategy remains cohesive as market conditions shift. In a 2026 environment defined by MAS exchange rate fluctuations and unpredictable Fed rate impacts, having a professional eye on your portfolio is no longer a luxury. It's a necessity for wealth protection.

At Zenith Wealth, we provide a "Modern Professional Guide" experience. We believe in human interaction over institutional coldness. Our approach focuses on your specific life stages, from education funding to legacy planning. We use the i12 investments framework to build portfolios that are resilient and growth-oriented. This isn't about following the herd. It's about a customized roadmap that respects your new status as a long-term stakeholder in Singapore. We stay ahead of the curve so you can focus on your career and family.

The Value of Independent-Minded Advice

Your journey is unique. You need advice that prioritizes your personal roadmap rather than just hitting sales targets. Your financial consultant acts as a proactive partner, helping you navigate the complexities of the local market. This partnership is built on transparency and professional integrity. As authorized representatives under finexis advisory, we combine boutique personal service with the strength of a leading financial institution. This ensures your wealth protection and retirement planning strategies meet the highest regulatory standards while remaining deeply personal.

Taking the Next Step

Getting started is straightforward. During your first discovery session, we'll focus on understanding your current position and future aspirations. It's an open-door conversation where your questions take center stage. To make the most of this time, prepare your financial documents, including your latest CPF statements and existing insurance policies. We'll conduct a comprehensive review to identify gaps in your current strategy and highlight new opportunities for growth. Ready to optimise your PR status? Contact a Zenith Wealth financial planner today to begin your transition toward a more secure and efficient financial future.

Secure Your Future in Singapore Today

Your status as a Singapore PR is a powerful tool for wealth creation. By integrating your mandatory savings with voluntary tax-efficient contributions and the i12 investments framework, you move from simply saving to strategically growing. You've seen how modern market conditions shift the math toward liquid, global portfolios. Now is the time to act on these insights. Navigating the diverse investment options for permanent residents in Singapore requires a partner who understands the local nuances. It's about more than just numbers; it's about your long-term security in your new home.

As authorized representatives of finexis advisory, we specialize in Singapore-specific retirement and legacy planning. Our team uses the i12 investments framework to ensure your portfolio remains resilient against global shifts. We're ready to help you build a legacy that lasts for generations. Your roadmap to financial independence is just one conversation away. We look forward to growing alongside you.

Start your PR wealth strategy session with Zenith Wealth. Let's start a conversation about your roadmap today.

Frequently Asked Questions

What are the best investment options for new PRs in Singapore?

The most effective strategy involves a coordinated approach across CPF, SRS, and private portfolios. This "Triple-Pillar" framework ensures you aren't just saving but actively compounding wealth through different tax-advantaged vehicles. By aligning these investment options for permanent residents in Singapore, you can capture local growth while maintaining a global hedge against regional volatility. It's about moving away from a fragmented "expat" mindset and building a cohesive local foundation.

Can a PR invest their CPF Ordinary Account (OA) in the stock market?

You can invest your CPF Ordinary Account savings through the CPF Investment Scheme (CPFIS) once you've set aside S$20,000 in your account. This scheme allows you to deploy funds into approved unit trusts and ETFs, such as the SPDR STI ETF, which saw strong performance in early 2026. For those looking to optimize their Special Account, a S$40,000 set-aside is required before investing. It's a proactive way to potentially exceed the guaranteed 2.5% base interest rate.

How does the SRS account help PRs save on income tax?

The Supplementary Retirement Scheme (SRS) offers a dollar-for-dollar tax deduction on all contributions, effectively lowering your taxable income for the year. For PRs, who can contribute up to S$15,300 annually, this provides an immediate and substantial tax shield. Once the funds are in the account, any investment gains grow tax-free until withdrawal. It's one of the most efficient ways to build a retirement nest egg while managing your current tax liabilities.

Is it better for a PR to buy a condo or invest in a diversified portfolio in 2026?

In the 2026 market, the 5% ABSD on a PR's first property purchase can make diversified portfolios more capital-efficient than physical real estate. While a condo ties up significant capital in a single illiquid asset, a portfolio of S-REITs can offer dividend yields in the 5% to 7% range without the maintenance costs. Many PRs now choose to rent their primary residence and invest their capital where it has higher growth potential. This approach offers far greater liquidity and geographical diversification.

What is i12 investments and how does it fit into my portfolio?

i12 investments is a sophisticated managed framework that uses an "active-passive" hybrid strategy to capture market upside while minimizing downside risk. It fits into your portfolio as the primary growth engine, providing institutional-grade access to sectors like global technology and healthcare. By integrating i12 investments, you move beyond basic retail products to a more tactical allocation. This ensures your wealth isn't just sitting in "safe" assets but is actively working to beat inflation.

How much should a PR contribute to their SRS account annually?

Permanent residents should aim to contribute the maximum of S$15,300 each year to fully leverage the available tax benefits. However, you must also be mindful of the S$80,000 overall personal income tax relief cap, which includes SRS, CPF, and other reliefs. Contributions must be completed by December 31st to qualify for that assessment year. A financial planner can help you calculate the exact amount needed to bring your taxable income down to the next lower bracket.

Do PRs have to pay tax on investment gains made outside of Singapore?

Singapore operates on a territorial tax system, meaning capital gains and most foreign-sourced income are generally not taxable for individuals. This makes it an ideal environment for PRs to manage global portfolios without worrying about local tax erosion on their gains. Whether you're investing in US tech stocks or European bonds, your profits typically remain yours to keep. This tax-neutral status is a major advantage for those looking to build generational wealth in the region.

How do I find a reliable financial planner for PR-specific advice?

Verify that your financial planner is an authorized representative of a licensed firm such as finexis advisory. You should look for a partner who prioritizes your personal roadmap over generic product sales. At Zenith Wealth, we focus on the i12 investments framework to help PRs navigate the transition from expat to long-term stakeholder. Seek a financial consultant who understands the nuances of CPF and SRS integration to ensure your strategy is both compliant and high-performing.