Did you know that even with Malaysia's core inflation averaging 2.1% in the first quarter of 2026, the specific cost of tertiary education continues to climb at a much faster rate? Most young parents feel the constant tension between funding their children's future and maintaining a comfortable lifestyle today. It's a difficult balance to strike when you're trying to figure out if your EPF contributions are enough or if you need to look toward private alternatives. If you've felt confused by the gap between your current savings and your future goals, you aren't alone.

This guide offers a clear, strategic roadmap for financial planning for young families Malaysia. You'll discover how to set precise education fund targets, maximize the latest 2026 tax reliefs, and build a retirement plan that doesn't sacrifice your current happiness. We'll show you how a professional financial planner uses frameworks like i12 investments to secure your wealth. From understanding the 4.10% SSPN dividend rates to implementing a "Barbell Strategy" for growth, we're here to help you move forward with quiet confidence and a solid plan for your family's legacy.

Key Takeaways

- Learn to build a dynamic financial roadmap that stays resilient against 2026 currency volatility and inflation trends.

- Discover why wealth protection is your non-negotiable foundation and how to mitigate the impact of rising private healthcare costs.

- Tackle the "Education Inflation Gap" with specific funding strategies designed for the current private and international school landscape.

- Calculate the true cost of a middle-class retirement and learn why financial planning for young families Malaysia must extend beyond basic EPF contributions.

- Explore how a professional financial planner integrates i12 investments to transform your family’s financial health through strategic management.

The 2026 Landscape: Why Financial Planning for Young Families in Malaysia has Changed

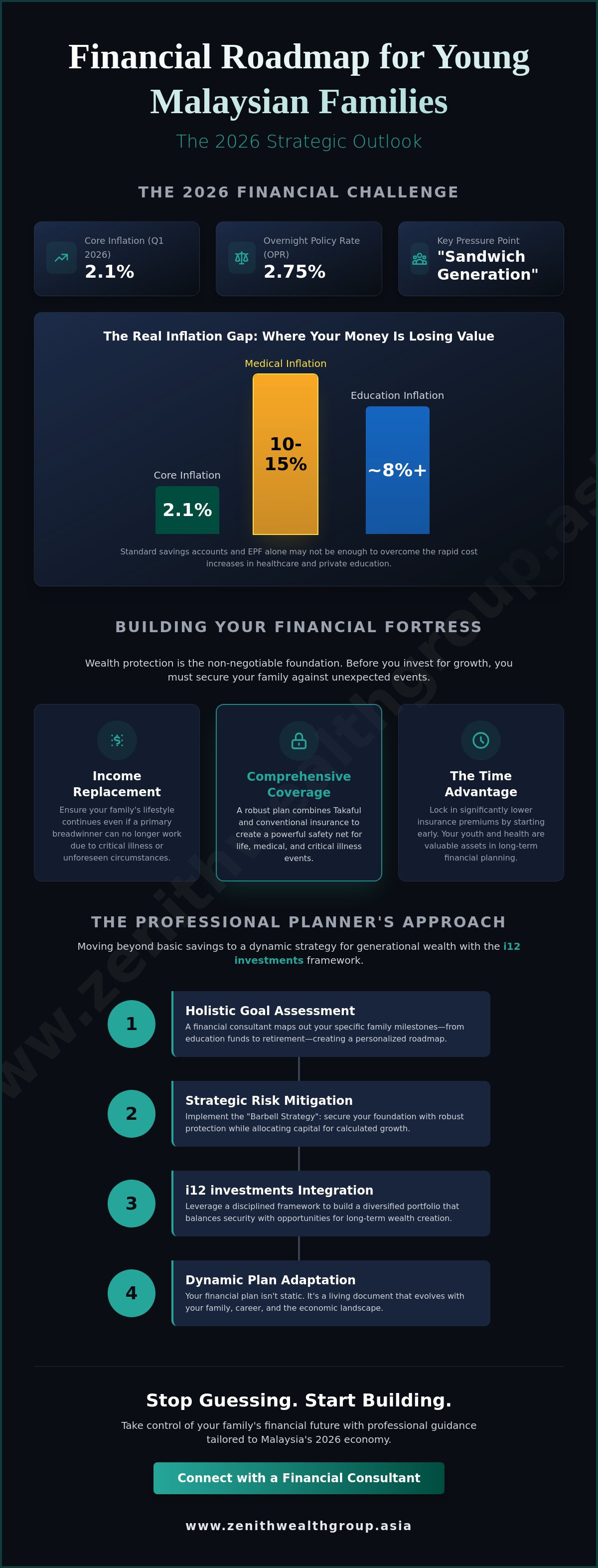

The 2026 economic environment in Malaysia is a complex puzzle for new parents. Core inflation averaged 2.1% in the first quarter of the year, but these numbers don't tell the whole story for a growing household. You're likely feeling the squeeze of the "Sandwich Generation" reality. You're trying to secure your child's future while ensuring your parents are well cared for in their later years. This dual pressure means your old approach to money needs an upgrade. You can't rely on a static savings account anymore. Instead, you need a deep understanding of what is a financial plan in a modern, volatile economy. It's not just a folder in a drawer; it's a living roadmap. Effective financial planning for young families Malaysia requires a shift from simply "saving for a rainy day" to strategically investing for generational wealth. Using frameworks like i12 investments allows you to build a legacy that lasts beyond the current market cycles.

Navigating the 2026 Cost of Living

Subsidy rationalisation has significantly changed the math for middle-class Malaysian families. With the Overnight Policy Rate (OPR) holding steady at 2.75%, the interest you earn in a standard bank account is barely keeping your head above water. Real inflation, especially in healthcare and education, often runs much higher than the headline figures. You need a proactive approach to cash flow management. It's about finding the "leaks" in your budget and redirecting those funds into assets that grow. High-interest environments demand discipline, but they also offer opportunities for those who know how to navigate them. This pressure is unique to our generation. We are the first to manage globalized investment opportunities while navigating local subsidy changes and currency volatility.

The Shift Toward Holistic Advisory

Many young couples turn to DIY financial apps to manage their wealth. While these are helpful for tracking daily spending, they rarely account for complex family milestones. They don't understand the nuance of your specific goals or the emotional weight of protecting your loved ones. A professional financial planner provides the strategic objectivity that an algorithm lacks. Zenith Wealth bridges the gap between high-level Singaporean expertise and the localized needs of the Malaysian market. We focus on human connection first. If you want to stop guessing and start building a secure future, you're invited to connect with a financial consultant today. We're ready to help you grow and adapt to whatever the 2026 economy brings next.

Building the Safety Net: Wealth Protection and Risk Mitigation

Building a family is an act of hope. Protecting it is an act of strategy. Wealth protection is the non-negotiable floor of your financial house. Without it, your investment strategy is just a house of cards. For those pursuing financial planning for young families Malaysia, the primary goal is ensuring that a single medical crisis or loss of income doesn't derail years of progress. Malaysian private healthcare is excellent, but it comes with a price tag. Medical inflation currently hovers between 10% and 15% annually. This means a hospital bill that costs RM20,000 today could easily double in a few short years. You need a plan that accounts for this trajectory, not just today's costs.

Income replacement is the next layer of your shield. If a breadwinner faces a critical illness, the family's lifestyle shouldn't have to change. We often see families integrate both Takaful and conventional insurance to create a comprehensive safety net. This hybrid approach respects cultural values while maximizing coverage efficiency. When you're looking for the right fit, you can verify the credentials of firms through the list of registered financial consultants provided by Bank Negara Malaysia. This ensures you're getting regulated, professional guidance from a qualified financial planner.

Critical Illness and Life Insurance in 2026

There's a massive difference between having a "basic policy" and having "comprehensive wealth protection." Young parents have a unique advantage: time. By locking in premiums early, you leverage your age to secure lower rates for the duration of the policy. This is a simple move that saves tens of thousands over a lifetime. It's about securing the most value while your health is at its peak. For those with interests across the causeway, you might also find value in our Wealth Protection in Singapore: The 2026 Guide for a broader perspective on regional safety nets.

The Role of i12 investments in Risk Management

Wealth protection isn't only about insurance. It's about how you structure your assets to survive a storm. Through i12 investments, we apply a disciplined approach to asset allocation that balances growth with security. You need liquid emergency funds that are easily accessible, but you also need protection-linked investments that evolve as your family grows. A family with one child has different risk needs than a family with three. Your financial planning for young families Malaysia should be elastic. If you're unsure if your current coverage is keeping pace with your life, it's a great idea to connect with a Zenith Wealth financial consultant to review your foundation.

Securing the Next Generation: Education Funding Strategies

Securing a quality education for your children is likely one of your highest priorities. In 2026, the landscape of private and international primary education in Malaysia has become increasingly competitive and costly. You're probably noticing that tuition fees don't follow the standard Consumer Price Index. This "Education Inflation Gap" means that while general inflation might stay low, the cost of a degree or a private school seat often rises at a much faster rate. Effective financial planning for young families Malaysia requires you to look beyond simple savings. You need a strategy that accounts for the specific trajectory of education costs, whether you're eyeing local private institutions like Taylor’s or Monash Malaysia, or considering the prestige of an overseas degree.

While PTPTN provides a baseline and SSPN-i remains a popular choice with its 4.10% dividend rate, these tools alone often fall short for those seeking a truly international standard of education. Private investment vehicles offer the growth potential necessary to bridge that gap. It's about finding a balance between government-backed stability and market-driven growth. If you're looking for professional standards in this area, the Financial Planning Association of Malaysia provides excellent resources on the ethical benchmarks you should expect from a certified financial planner. They help define the standards that keep your family's interests protected.

Calculating the Real Cost of a Degree

The total cost of a degree isn't just tuition. You have to factor in living expenses, travel, and the often volatile currency exchange rates if you're looking at universities in the UK, Australia, or the US. Timing is your most powerful asset. Starting an education fund when your child is born versus waiting until they are five years old can reduce your required monthly outlay by as much as 40%. This is the power of compounding at work. For a broader regional perspective on these costs, you can explore our Education Funding in 2026: A Comprehensive Guide to see how Malaysian costs compare to regional benchmarks.

Strategic Funding with i12 investments

We use i12 investments to give families access to diversified growth markets that aren't always available through standard retail channels. This is crucial for education funds that need to outpace tuition inflation over the long term. One key strategy is the "Time-Horizon" shift. We help you move from aggressive growth in the early years to capital preservation as your child approaches 18. This protects your hard-earned gains from sudden market swings just when you need the cash. Most importantly, a structured plan prevents the common mistake of withdrawing from your retirement funds to pay for school. If you want to build a dedicated fund that doesn't compromise your own future, it's a great time to connect with a financial consultant today.

Balancing the Present with the Future: Retirement and Legacy

Most young parents in Malaysia view retirement as a distant concern. They prioritize immediate needs like housing and school fees. However, waiting too long to address your own future can create a massive burden for your children later. EPF (KWSP) remains a vital foundation. With employee contribution rates at 11% and employer rates between 12% and 13%, it's a solid start. But is it enough? The 2026 reality is that many Malaysians exhaust their EPF savings within five years of withdrawal. To maintain a middle-class lifestyle, you must calculate the "Retirement Sum" required to beat long-term inflation. Effective financial planning for young families Malaysia means building a secondary pillar of wealth that doesn't rely solely on government schemes.

Legacy planning is the other side of this coin. It isn't just for the wealthy or the elderly. For a young family, it's about protection and guardianship. Have you nominated your beneficiaries in your EPF and insurance policies? This simple act ensures funds reach your loved ones without lengthy legal delays. Beyond nominations, tools like Wills and Hibah allow you to dictate exactly how your assets are distributed and, more importantly, who will care for your children if you cannot. It’s about providing certainty in an uncertain world.

Bridging the EPF Gap

A professional financial planner helps you identify your "Retirement Shortfall" by comparing your projected EPF balance against your actual lifestyle goals. We often look toward global investment management to provide the diversification needed for long-term growth. By using frameworks like i12 investments, you can access international markets that offer a hedge against local currency volatility. For deeper insights into building a resilient portfolio, explore our guide on Strategic Investment Management in 2026. Diversification is your best defense against a shifting economic landscape.

Legacy Planning: Protecting Your Children’s Inheritance

In the Malaysian legal context, there’s a significant difference between a Will and a Trust. A Will is essential for documenting guardianship, while a Trust can provide your family with immediate liquidity for daily expenses. If you hold assets across the border, you should also consider our Legacy Planning in Singapore guide to ensure your cross-border interests are fully protected. Don't leave your children's future to chance. If you're ready to build a roadmap that covers both your retirement and your family's legacy, connect with a financial consultant today to start the conversation.

How a Financial Planner Transforms Your Family’s Financial Health

Many families treat financial decisions as a series of one-off purchases. You buy a medical card here and open a savings account there. This "product buying" approach often leads to fragmented results and missed opportunities. Real financial planning for young families Malaysia is about strategic integration. A financial planner looks at your entire ecosystem. They ensure your protection, education funds, and retirement pillars work together as a single, cohesive unit. At Zenith Wealth, your first discovery session is about listening. We want to understand your specific anxieties and your biggest dreams. We don't start with a sales pitch; we start with a conversation.

Professional oversight is your best defense against common errors. It’s easy to fall into the trap of over-insurance, where you're paying for coverage you don't actually need. Conversely, many young families are under-invested. They leave too much cash sitting in low-yield accounts that lose value to inflation every day. We help you find the "Goldilocks zone." This means having enough protection to sleep at night and enough growth to reach your goals. Our goal is to move you from a place of financial anxiety to a clear, actionable 5-year roadmap. You deserve to feel in control of your family's future.

The Value of Professional Advisory

As authorized representatives of finexis advisory, we have access to a vast range of solutions. We aren't limited to a single provider's catalog. This breadth allows us to tailor the i12 investments framework to your family's unique risk appetite. While AI tools are becoming popular for budgeting, they lack the "Human Element." An algorithm doesn't understand the emotional weight of your child's first day at university or the stress of a major home purchase. A financial consultant provides the empathy and experience that technology cannot replicate. We grow alongside you.

Start Your Journey Today

Proactive planning is always more effective than reactive crisis management. Don't wait for your second child to arrive or your next home purchase to review your strategy. Start today with a complimentary family financial health check. It’s a low-pressure way to see where you stand and identify any hidden gaps in your financial planning for young families Malaysia. You're invited to speak with a Zenith Wealth financial consultant today. Let's build your 2026 strategic roadmap together. We're ready when you are.

Take Charge of Your Family's 2026 Roadmap

Securing your family's future in the evolving 2026 economy doesn't have to be overwhelming. You've seen how a strong foundation of wealth protection and early education funding can change your children's trajectory. By diversifying your strategy with i12 investments and looking beyond basic EPF contributions, you're building a legacy that lasts. The shift from product buying to a holistic, strategic plan is what truly transforms your financial health. It's about moving from simple savings to intentional wealth creation.

Effective financial planning for young families Malaysia requires more than just a bank account; it requires a partner who understands the unique pressures of the Sandwich Generation. As authorized representatives of finexis advisory, we specialize in education and legacy planning. Zenith Wealth offers modern professional guidance tailored specifically for Southeast Asian families. We're here to help you move from uncertainty to action with a plan that fits your life today and your dreams for tomorrow.

Connect with a Zenith Wealth financial consultant to secure your family’s future. Your journey toward generational wealth starts with a single, confident step. We look forward to growing alongside you.

Frequently Asked Questions

Is EPF enough for retirement in Malaysia in 2026?

EPF alone is rarely sufficient for a comfortable middle-class retirement in 2026. While it offers a stable foundation, the rising cost of living and healthcare means most families face a significant "Retirement Shortfall." To maintain your current lifestyle, you'll likely need supplemental private investments that offer higher growth potential. A professional financial planner can help you calculate your specific gap and build a secondary pillar of wealth.

What is the best way to start an education fund for my newborn?

The best way to start is by combining immediate tax benefits with long-term growth vehicles. Open an SSPN account to capture government dividends and tax reliefs, but don't stop there. For financial planning for young families Malaysia, it's essential to use diversified investment frameworks that outpace tuition inflation. Starting at birth allows you to leverage eighteen years of compounding, significantly reducing your required monthly contributions compared to starting later.

How much should a young family in Malaysia spend on insurance premiums?

A general rule of thumb is to allocate around 10% of your take-home pay toward wealth protection. However, this isn't a one-size-fits-all number. Your actual premium should be based on your debt obligations, number of dependents, and specific lifestyle goals. A financial consultant will help you audit your current policies to ensure you aren't over-insured in some areas while remaining dangerously exposed in others.

Can a financial consultant help if I have significant student or housing debt?

Yes, a financial consultant is often most valuable when you're managing significant liabilities like PTPTN loans or a first mortgage. They help you restructure your cash flow to ensure debt repayment doesn't stall your long-term wealth building. By optimizing your interest costs and identifying "leaks" in your budget, they create a path where you can pay down debt while simultaneously funding your family's future.

What are i12 investments and how do they fit into a family plan?

i12 investments represents a strategic framework designed to balance local protection with global growth opportunities. It fits into your plan as the engine that drives your long-term goals, such as education and retirement. By diversifying beyond the Malaysian market, i12 investments helps hedge against local currency volatility. This ensures your family's wealth is resilient and positioned to capture growth in multiple sectors and regions.

Do I need a Will if I only have a small amount of assets currently?

Yes, you need a Will regardless of your current net worth because it legally documents your children's guardianship. If both parents are absent, the state decides who cares for your minors unless a Will is in place. Legacy planning is about more than just money; it's about providing clear instructions for your family's care and ensuring your nominations for EPF and insurance are fully aligned with your wishes.

How does inflation in Malaysia affect my long-term investment goals?

Inflation erodes your future purchasing power, meaning your investment returns must consistently beat the inflation rate to be effective. If your savings only grow at the same rate as inflation, your "real" wealth stays stagnant. This is why financial planning for young families Malaysia focuses on assets that offer real growth. We look for diversified portfolios that protect your lifestyle against the rising costs of daily goods and services.

How often should we review our family financial plan with a professional?

You should review your plan at least once a year to ensure it stays aligned with your evolving goals. Major life milestones, such as a promotion, a home purchase, or the arrival of a second child, also warrant an immediate check-in. These reviews with your financial planner allow for tactical adjustments. It ensures your roadmap remains a living document that adapts to both market changes and your family's changing needs.