What if your "safe" bet on local banks and REITs is actually the biggest risk to your long-term wealth? It's common to feel secure with familiar names, but over-concentration in one sector often leads to unexpected losses when market cycles turn. If you're feeling the pressure of global inflation affecting your local purchasing power, you're not alone. Many investors find themselves stuck between wanting growth and fearing the unknown. Implementing the right diversification strategies for investment portfolio Singapore is the key to moving forward with confidence.

You're about to master a more balanced approach. We'll show you how to protect and grow your wealth using the i12 investments framework, a structured method designed for today's volatile environment. This guide simplifies the process of integrating your CPF and SRS contributions with private holdings. By the end, you'll have a clear roadmap that aligns your assets with your retirement and education goals. Let's look at how a financial consultant can help you build a portfolio that doesn't just survive market shifts, but thrives through them.

Key Takeaways

- Identify and overcome the "home bias" trap that leaves many Singaporean portfolios over-exposed to local banks and REITs.

- Master the i12 investments framework to create a core-satellite structure that prioritises both wealth protection and long-term growth.

- Implement effective diversification strategies for investment portfolio Singapore by strategically expanding into US, China, and Southeast Asian markets.

- Optimise your retirement and education funding by integrating SRS contributions for maximum tax efficiency and geographic reach.

- Learn how a professional financial planner helps you avoid common DIY rebalancing pitfalls to keep your roadmap on track.

Why Portfolio Diversification is Essential in Singapore’s 2026 Market

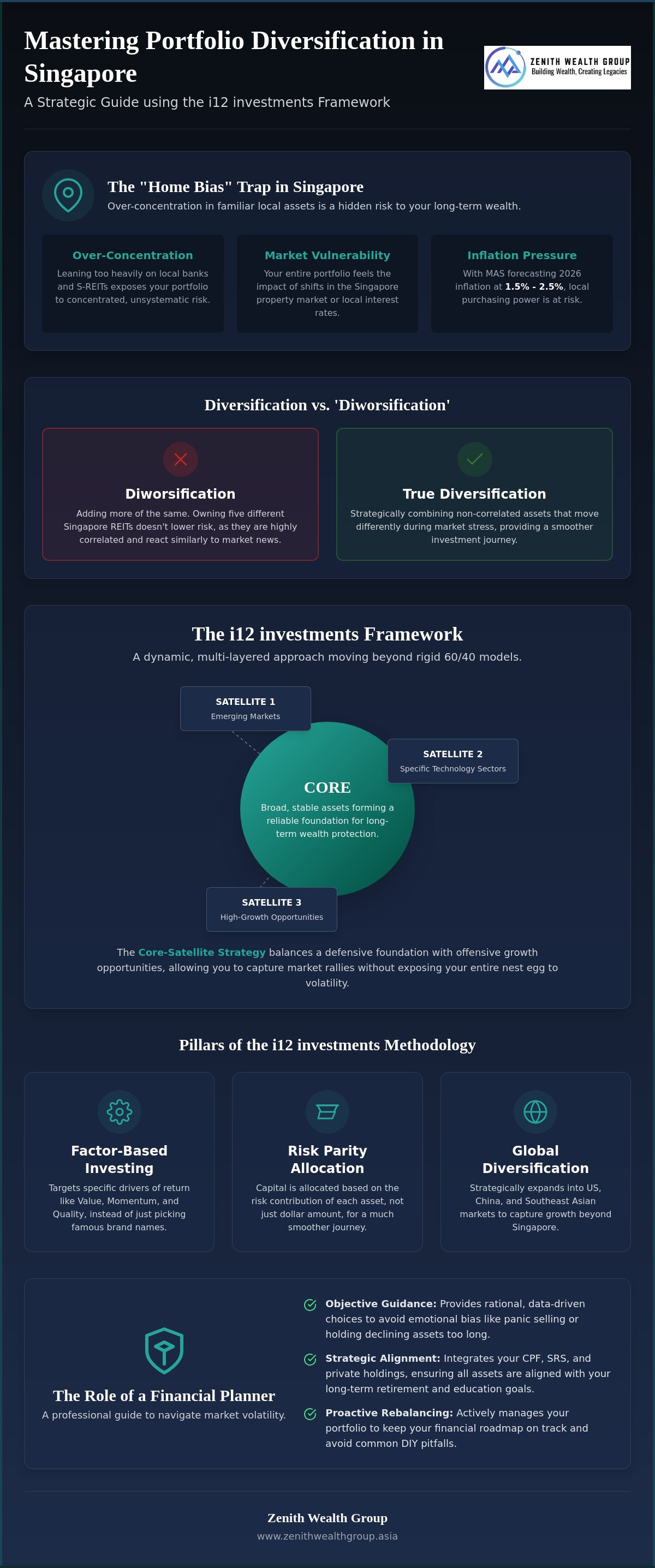

Diversification is the strategic allocation of capital to ensure no single asset dictates your financial fate. It is more than just a safety net. It is a proactive strategy to capture growth while minimizing losses. In Singapore, many investors fall into the "Home Bias" trap. We often lean too heavily on local banks and S-REITs because they feel familiar. This over-concentration creates a significant vulnerability. Relying on a few local sectors exposes you to unsystematic risk. If the Singapore property market or local interest rates shift, your entire portfolio feels the sting. You need a broader perspective to stay protected.

The 2026 economic landscape makes this even more critical. The Monetary Authority of Singapore (MAS) forecasts inflation between 1.5% and 2.5% for the year. Additionally, anticipated easing of global interest rates may put pressure on the profit margins of local banks. Relying solely on the Straits Times Index (STI) is no longer a complete solution. Effective diversification strategies for investment portfolio Singapore require a global view. You must balance the stability of the local market with the high-growth potential of international sectors. This approach ensures your wealth continues to grow even when one region or sector slows down.

The Difference Between Diversification and Diworsification

Adding more assets to your list does not always lower your risk. If you own five different Singapore REITs, you are not necessarily diversified. This is often called "diworsification" because those assets are likely to react to market news in the same way. True diversification relies on concepts found in Modern Portfolio Theory. This framework suggests combining assets that move in opposite directions during market stress. In a Singaporean stock portfolio, correlation refers to the statistical measure of how two different investments move in relation to each other when market conditions change. Your goal is to find non-correlated assets that provide a smoother ride through volatile cycles. Don't just collect assets; select them based on how they interact.

Managing Market Volatility with a Professional Guide

Navigating these shifts alone is difficult. Emotional bias often leads to panic selling or holding onto declining assets for too long. A financial planner acts as your Modern Professional Guide. They provide the objective distance needed to make rational, data-driven choices. By using the i12 investments framework, they ensure your assets stay aligned with your long-term vision. This proactive partnership is vital for more than just immediate growth. It is a core component of Legacy Planning in Singapore. A financial consultant helps you rebalance as 2026 progresses, keeping your financial roadmap on track and your wealth protected for the next generation.

The i12 investments Framework: A Holistic Approach to Asset Allocation

Traditional investment models, like the classic 60/40 split between stocks and bonds, often fall short in complex markets. The i12 investments framework moves beyond these rigid structures. It provides a more dynamic, multi-layered approach to building and sustaining wealth. Instead of simply spreading money across different sectors, this methodology focuses on how different assets behave under various economic conditions. It’s about building a portfolio that is both offensive for growth and defensive for protection. This is a shift from passive collecting to active, strategic management.

A central feature of this framework is the Core-Satellite strategy. Your "core" consists of broad, stable assets designed to provide a reliable foundation over decades. Around this core, your "satellites" consist of targeted, high-growth opportunities. These might include emerging markets or specific technology sectors that offer higher potential returns. This balance is a cornerstone of effective diversification strategies for investment portfolio Singapore. It allows you to participate in market rallies without exposing your entire nest egg to extreme volatility.

The i12 investments approach also utilizes factor-based investing. Rather than just picking famous brand names, it targets specific drivers of return such as value, momentum, and quality. By focusing on these factors, you’re investing in proven economic characteristics that historically outperform the broader market. Combined with risk parity, which allocates capital based on the risk contribution of each asset rather than just the dollar amount, you get a much smoother investment journey. If one asset class is twice as volatile as another, the framework adjusts your exposure accordingly to maintain a steady risk profile.

The Pillars of the i12 investments Methodology

The i12 investments methodology relies on a systematic selection process for global equities and fixed income. It removes the guesswork that often leads to poor DIY results. In 2026, as interest rates are expected to ease, the yields on traditional savings and T-bills are shifting. The framework adapts to these changes by identifying where the next cycle of growth will likely emerge. It brings the same institutional-grade logic used by major funds to your personal wealth. You can explore these 4 Portfolio diversification strategies to see how various asset classes can be layered to provide better security.

Customising i12 for Your Specific Goals

Every investor has a unique destination. Your roadmap for retirement planning should not look the same as a plan for your child’s education funding. A financial planner helps you dial the i12 framework up or down based on your specific timeline and risk appetite. They ensure your Strategic Investment Management in 2026 stays focused on what matters most to you. If you're looking for a partner to help navigate these choices, connecting with a financial consultant can help you build a plan that feels both professional and personal.

Strategic Diversification Beyond the SGX: Geography and Alternative Assets

Limiting your focus to the Singapore Exchange (SGX) restricts your growth potential. While local banks and REITs provide steady dividends, the real engines of innovation often lie elsewhere. In 2026, exposure to the US, China, and Southeast Asia is non-negotiable. These regions offer access to sectors like AI-driven infrastructure and Green Tech that are underrepresented locally. Implementing global diversification strategies for investment portfolio Singapore allows you to capture these tailwinds. It moves your wealth from a single-country risk to a worldwide opportunity set. You aren't just betting on one economy; you're betting on global progress.

Currency management is a vital part of this global shift. The Monetary Authority of Singapore (MAS) manages the Singapore dollar against a basket of currencies to maintain stability. When you hold global assets, you are also managing exchange rate risks. A strong Singapore dollar can eat into your international gains. Conversely, a weaker local currency can boost them. Professional Diversification strategies for retail investors often include tactical currency positioning to protect your purchasing power. A financial consultant can help you navigate these fluctuations using the i12 investments framework. This ensures your global gains actually translate into local wealth.

Alternative investments provide another layer of resilience. Gold, private equity, and private real estate often move independently of the stock market. They act as a buffer during periods of high volatility. In 2026, as geopolitical tensions influence trade, these uncorrelated assets are essential. They ensure that even if equities face a downturn, your total portfolio has a stabilizing force. It is about building a multi-dimensional defense. The i12 investments methodology integrates these alternatives to smooth out the investment journey.

The Role of Global Equities in Growth

The S&P 500 has historically offered higher capital appreciation compared to the income-focused STI. For long-term growth, accessing these markets through institutional-grade platforms is more cost-effective than simple retail apps. Changes in the US trade balance can shift the value of the US dollar, directly impacting the local purchasing power of Singaporean investors holding American assets. Using the i12 investments approach, we look for momentum and quality across these global indices to maximize your returns. We help you find the right balance between local stability and global growth.

Fixed Income and Hedges

Stability remains a priority. Singapore Savings Bonds (SSB) and T-Bills serve as excellent low-volatility anchors for your capital. For July 2026, the 10-year average return for SSBs stands at 2.11% per annum, while 6-month T-bill yields are around 1.50%. These instruments provide a safe harbor while you wait for better entry points in the equity markets. Integrating these with Wealth Protection in Singapore ensures your portfolio survives inflationary spikes and market corrections alike. It's about staying power.

Building Your Diversified Roadmap: Strategies for Every Life Stage

A static portfolio is a vulnerable portfolio. Your financial needs at thirty are vastly different from your requirements at sixty. Effective diversification strategies for investment portfolio Singapore must account for these shifts in timeline and risk tolerance. Building a roadmap requires a step-by-step approach that integrates your private wealth with national schemes like CPF and SRS. This ensures every dollar you earn is working toward a specific life goal. Don't leave your future to chance; structure it with precision.

- Step 1: Define Your Timeline. Are you saving for a child's university fees in ten years or your own retirement in thirty? Shorter timelines require more stable, liquid assets, while longer horizons allow you to capture global equity growth.

- Step 2: Maximise Tax Efficiency. Use the Supplementary Retirement Scheme (SRS) to your advantage. For 2026, Singapore Citizens and PRs can contribute up to S$15,300 to reduce taxable income. Remember that the statutory retirement age for withdrawals has raised to 64 as of July 1, 2026.

- Step 3: Leverage CPF as an Anchor. Your CPF Ordinary Account (2.5% p.a.) and Special Account (4.0% p.a.) act as your "risk-free" bond component. This allows you to be more aggressive with your private investments because your foundation is already secure.

- Step 4: Implement i12 investments. Select the right satellite assets based on your stage. Younger investors might lean toward tech-heavy momentum factors, while those closer to retirement may focus on quality and dividend yield.

- Step 5: Regular Rebalancing. Market conditions in 2026 will not stay the same. By 2028, sector winners will shift. You must adjust your holdings periodically to ensure your risk levels haven't drifted.

For Young Parents: Prioritising Education and Growth

If you're raising a family, you're likely balancing immediate costs with the need for long-term accumulation. The i12 investments framework helps you carve out specific buckets for your children's future. You can explore our guide on Education Funding in 2026 to see how child-specific investment vehicles provide a head start. It's about growing wealth today so they have more opportunities tomorrow.

For Pre-Retirees: Shifting Toward Wealth Preservation

As retirement approaches, the focus shifts from building the pile to protecting it. You need to transition toward income-generating assets that supplement your CPF Life payouts. Private annuities and high-quality dividend stocks become your primary tools. Managing this transition requires a deep dive into your tax position. Check out our resource on Mastering the SRS Account to learn how to draw down your funds efficiently. If you're unsure how to align these moving parts, a financial consultant can help you build a cohesive plan that secures your lifestyle.

Optimising Your Portfolio with a Professional Financial Planner

DIY investing is tempting in an age of high-speed apps. However, many Singaporeans fall into a common trap. They buy assets but fail to manage them over time. Without regular rebalancing, your initial diversification strategies for investment portfolio Singapore can quickly become lopsided. A single winning stock might grow to occupy too much of your portfolio, exposing you to higher risk than you intended. A financial planner provides the discipline needed to stay on track. They remove the emotional weight of decision-making, ensuring your roadmap stays aligned with your original goals.

Choosing Zenith Wealth Group means accessing more than just generic advice. As authorised representatives of finexis advisory, we bring institutional-grade resources to your personal financial planning. We use the i12 investments framework to build portfolios that are resilient across market cycles. This methodology isn't about chasing the latest trend. It's about a systematic, factor-based approach that prioritises both growth and wealth protection. You move from a static savings plan to a dynamic, living investment roadmap that evolves with you.

What to Expect in a Consultation

Our approach starts with a holistic wealth analysis. We don't just look at your stocks; we look at your entire cash flow, insurance needs, and future liabilities. During a consultation, we identify specific gaps in your current diversification strategy. Perhaps your global exposure is too low, or your tax efficiency through SRS hasn't been fully utilised. We invite you to connect for a personalised i12 investments review. It is a conversation focused on your unique situation, providing you with clear action steps to strengthen your financial position.

Achieving Long-Term Financial Security

True financial security is about more than just hitting a specific number. It's about ensuring your wealth lasts for your lifetime and serves your family for generations. By focusing on legacy planning and generational wealth, we help you build a portfolio that stands the test of time. There is a deep peace of mind that comes from knowing your assets are professionally managed and protected against market shifts. Ready to diversify? Contact our financial planners today for a personalised roadmap.

Secure Your Wealth Roadmap for 2026 and Beyond

Building a resilient portfolio is a continuous journey, not a one-time event. You've seen how moving beyond the local "Home Bias" and embracing global markets can transform your long-term security. By using the i12 investments framework, you can balance aggressive growth with essential wealth protection. It's about making your CPF and SRS contributions work in harmony with your private assets to create a truly cohesive plan. Mastering diversification strategies for investment portfolio Singapore ensures you aren't just saving money. You're strategically building a legacy that survives market shifts.

As authorised representatives of finexis advisory Pte Ltd, we specialize in the i12 investments methodology. Our team brings proven expertise in Singapore retirement and education planning to help you navigate every life stage with confidence. Don't let market volatility or global inflation dictate your family's future. Book a consultation with a Zenith Wealth Group financial planner to build your i12 investments roadmap. We're ready to start the conversation and grow alongside you. Let's turn your financial goals into a living reality.

Frequently Asked Questions

What are the best diversification strategies for a Singaporean investor in 2026?

The most effective strategies involve moving beyond a home bias toward a core-satellite structure that includes global equities and alternative assets. By incorporating the i12 investments framework, you can balance the stability of the Singapore market with growth in the US and Southeast Asia. This approach helps mitigate local sector risks while capturing innovation in sectors like AI and green energy.

How does the i12 investments framework differ from traditional asset allocation?

The i12 investments framework differs by focusing on specific drivers of return like quality, momentum, and value rather than just broad asset classes. While a traditional 60/40 portfolio is static, i12 uses risk parity to allocate capital based on the risk contribution of each asset. This results in a smoother investment experience that adapts more effectively to market volatility.

Can I use my SRS account to diversify my investment portfolio?

Yes, your SRS account is a powerful tool for implementing diversification strategies for investment portfolio Singapore while gaining tax relief. You can invest your SRS funds in a variety of global unit trusts, ETFs, or private annuities. For 2026, the contribution limit remains at S$15,300 for citizens and PRs, allowing you to build a tax-efficient global satellite to your local holdings.

Is it better to hire a financial consultant or manage my own diversified portfolio?

Hiring a financial planner is often better because they provide the objective discipline needed to rebalance effectively without emotional bias. While DIY platforms offer accessibility, they lack the institutional-grade methodology found in the i12 investments approach. A financial consultant ensures your portfolio remains aligned with your long-term roadmap and retirement goals as market conditions change.

How often should I rebalance my diversified portfolio in Singapore?

You should review and rebalance your portfolio at least once a year or whenever an asset class drifts significantly from its target allocation. Regular rebalancing ensures you are selling high and buying low, which maintains your desired risk profile. In a fast-moving market like 2026, staying disciplined with these adjustments is crucial for protecting your wealth.

What is the role of CPF in a diversified investment strategy?

CPF serves as your "risk-free" bond anchor, with the Ordinary Account earning 2.5% and the Special Account earning 4.0% per annum as of July 2026. Because these guaranteed returns provide a solid foundation, you can afford to be more strategic with your private investments. This allows you to allocate more toward high-growth global equities within the i12 investments framework.

How do global interest rates affect my local Singaporean investments?

Global interest rate shifts directly impact local REIT valuations and the profit margins of Singapore's major banks. When the Fed eases rates, it typically boosts S-REITs but can compress the net interest margins of local lenders like DBS or OCBC. Diversifying across different geographies ensures your portfolio isn't overly dependent on the interest rate environment of a single country.

What are the risks of being over-concentrated in the Singapore stock market?

Over-concentration in the Singapore market leaves you vulnerable to unsystematic risk and local economic downturns. If the Singapore property market faces headwinds, a portfolio heavy in REITs will suffer regardless of how well global markets are performing. Expanding your reach globally through the i12 investments methodology provides a necessary buffer against these localized shocks.