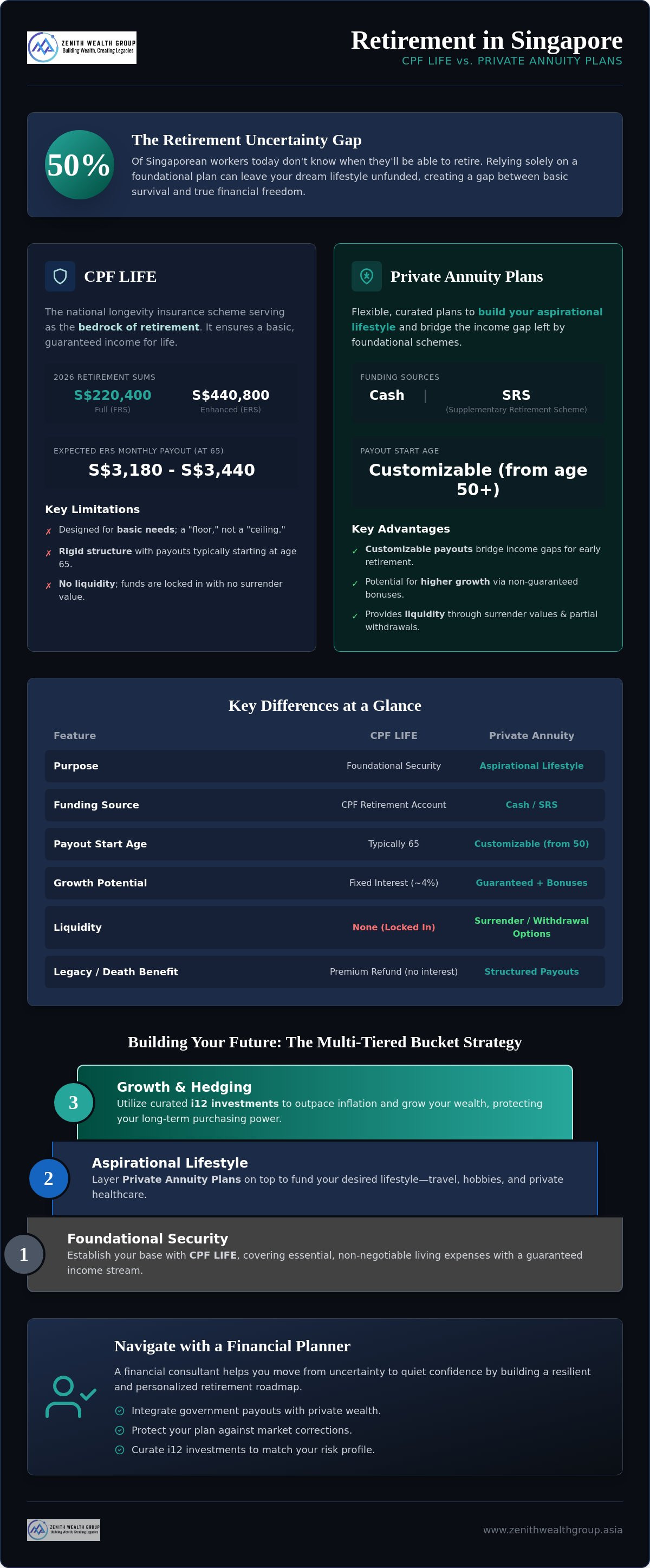

Did you know that 50% of Singaporean workers today still don't know when they'll actually be able to retire? It's a heavy thought. You've spent years building your career. Yet the fear of outliving your savings or watching inflation erode your purchasing power remains. When you start comparing CPF LIFE vs private annuity plans Singapore, the complexity of dozens of insurance options can feel overwhelming.

You deserve more than just a survival fund. You want a lifestyle that reflects your hard work. Learn exactly how to bridge the gap between basic CPF payouts and your dream retirement. We'll use curated private annuity strategies and i12 investments to get you there. Our focus is moving you from uncertainty toward quiet confidence.

This article provides a clear roadmap for your future. We'll break down the 2026 retirement sums and explore how to hedge against rising costs. See how a financial planner can help you build a retirement income that is both guaranteed and aspirational. Let's start building your ceiling above the CPF floor.

Key Takeaways

- Recognize why CPF LIFE is your foundational security and how to build a robust income stream that outpaces 2026 inflation.

- Compare the mechanics of CPF LIFE vs private annuity plans Singapore to identify the best funding mix using cash or SRS contributions.

- Explore the i12 investments advantage, where human-led curation replaces generic automation for more precise wealth management.

- Build a multi-tiered 'Bucket Strategy' that seamlessly connects your government payouts with private wealth for a dream lifestyle.

- Understand why partnering with a financial planner ensures your retirement roadmap remains resilient against market corrections.

The 2026 Retirement Landscape: Is CPF LIFE Enough?

CPF LIFE serves as the bedrock of retirement for almost every Singaporean. It's essentially a national longevity insurance scheme managed under the Central Provident Fund (CPF). Its primary goal is simple: ensure you don't run out of money, no matter how long you live. However, as we look at the costs of living in 2026, many are realizing that a "floor" isn't the same as a "ceiling." Relying only on this mandated scheme might keep you afloat, but it won't necessarily fund the lifestyle you've worked so hard to build.

For many professionals, the debate between CPF LIFE vs private annuity plans Singapore boils down to the "Lifestyle Gap." While the government provides a safety net, it's designed for basic needs. If your dream retirement includes travel, dining out, or private healthcare, the math starts to look different. In 2026, we're seeing inflation continue to pressure purchasing power, making a single income stream look increasingly risky.

Understanding the Payout Ceiling

Your monthly payout depends entirely on the Retirement Sum you've set aside at age 55. The Full Retirement Sum (FRS) for 2026 is set at S$220,400. If you hit the Enhanced Retirement Sum (ERS) of S$440,800, you can expect monthly payouts between S$3,180 and S$3,440 starting at age 65. While that sounds substantial, a financial planner will tell you that for a high-income earner, this often covers less than half of their current monthly expenses. The "Basic" plan is even more restrictive, often falling short for those used to a middle-class lifestyle in a high-cost city like Singapore.

The Role of Longevity Risk in Singapore

We're living longer than ever. With the statutory retirement age rising to 64 in July 2026, the period you'll need to fund is stretching. There's a real danger that inflation will outpace the 4% interest rate on your Retirement Account. This is where the synergy of private wealth comes in. You can explore The Complete Guide to Retirement Planning in Singapore to see how different assets work together to protect your purchasing power.

Relying solely on CPF means you're locked into a rigid payout structure that doesn't account for early retirement or sudden lifestyle changes. To truly hedge against 2026's economic realities, you need a strategy that combines government guarantees with the flexibility of private curation, such as i12 investments. This approach allows you to build a ceiling that matches your aspirations. If you're ready to see how these pieces fit your specific numbers, you can reach out to us for a conversation.

Key Differences: CPF LIFE vs. Private Annuity Plans

Choosing between CPF LIFE vs private annuity plans Singapore isn't about picking a winner. It's about understanding how they function differently to serve your specific needs. While CPF LIFE relies on your Retirement Account (RA) balance, private plans are funded through cash or the Supplementary Retirement Scheme (SRS). This distinction is vital. You cannot use your CPF savings for private annuities, which means these plans must be part of your broader cash flow strategy.

Flexibility is where private plans often shine. CPF LIFE payouts generally begin at age 65. If you plan to stop working at 55 or 60, you'll face an income void. Private annuity plans allow you to select payout start ages as early as 50. This customization lets you bridge the gap before your government payouts kick in. Additionally, death benefits differ significantly. CPF LIFE refunds the remaining premium without interest, while private plans often provide a structured legacy payout for your beneficiaries, ensuring your wealth protection goals are met.

Payout Predictability and Growth

CPF LIFE provides a stable, government-guaranteed floor. In contrast, private annuities often feature a participating structure. This participating nature means the insurer pools your premiums with other policyholders' funds to invest in a diversified portfolio, sharing the profits with you. Your total monthly income consists of a guaranteed base and a non-guaranteed bonus. These bonuses depend on the performance of the insurer's life fund. A reliable source dispels common myths about CPF LIFE regarding its sustainability, but private plans offer the potential for higher growth through these dividends. Integrating i12 investments into this mix can further enhance your portfolio's risk-adjusted returns by curating specific fund selections that align with your risk appetite.

Liquidity and Surrender Values

One major trade-off involves liquidity. CPF LIFE is an "all-in" commitment. Once you're in, there's no surrender value or option to withdraw a lump sum for emergencies. Private plans provide a safety net through surrender values or partial withdrawal features. While you might sacrifice some guaranteed return for this flexibility, it provides peace of mind for unexpected life events. Balancing these two requires a careful look at your total assets. If you're unsure how to layer these benefits, a financial planner can help you map out a tiered income strategy that keeps you liquid and secure.

The i12 investments Advantage: Curation Over Automation

While the debate over CPF LIFE vs private annuity plans Singapore often centers on guaranteed income, true retirement security in 2026 requires a growth engine. Guaranteed payouts provide your floor, but they rarely provide your ceiling. This is where i12 investments come in. It's a sophisticated layer for your retirement wealth that moves beyond the basic "set-and-forget" mentality. We don't believe in leaving your hard-earned savings to the mercy of a cold, automated algorithm. Instead, we focus on curation to ensure your portfolio works as hard as you did.

In the volatile market environment of 2026, active management isn't just a luxury; it's a necessity. Zenith Wealth utilizes i12 investments to supplement your annuity income, creating a balanced ecosystem of safety and growth. By selecting funds that prioritize risk-adjusted returns, we help you capture market upside without exposing your retirement foundation to unnecessary danger. This human-led approach provides a level of precision that generic indexes simply can't match.

Why Curation Beats Generic Algorithms

Many investors today are lured by the promise of low-cost robo-portfolios. However, these platforms often lack the nuanced oversight required for retirees who can't afford a major drawdown. i12 investments focus on manager quality and robust downside protection. We look for fund managers who've proven their ability to navigate turbulent cycles. This proactive stance is essential for protecting your purchasing power against 2026's economic shifts. For more on how we approach these complexities, read our guide on Strategic Investment Management in 2026.

Portfolio Synergy with Annuities

The magic happens when you combine these tools. Your private annuity provides a predictable monthly check, while i12 investments offer the potential for capital appreciation. This synergy allows you to draw from your growth assets during bull markets and rely on your "floor" during corrections. We tailor the i12 approach to your specific risk tolerance, ensuring your strategy remains personal and proactive. Every fund chosen for i12 inclusion must undergo a rigorous vetting process that evaluates long-term consistency and institutional-grade management. This isn't just about picking products; it's about building a resilient future. If you're ready to see how this curation fits your plan, we're ready to start the conversation.

Strategic Integration: Building a Multi-Tiered Income

Integrating your retirement assets isn't just about picking products. It's about building a multi-tiered income stream that survives market shifts. The "Bucket Strategy" is a practical way to organize this. You allocate your funds across three distinct layers: your CPF LIFE floor, your private annuity bridge, and your i12 investments growth engine. This structure ensures you have guaranteed cash for essentials while keeping some capital liquid for lifestyle upgrades. It's a proactive way to manage your wealth rather than just letting it sit.

One often overlooked obstacle is the "accrued interest trap." If you've used your CPF Ordinary Account to fund your home, selling that property in retirement means you must refund the principal plus 2.5% compounded interest back into your CPF. This can significantly reduce the cash proceeds you planned to live on. A financial planner helps you navigate these nuances. We ensure your property decisions don't derail your retirement cash flow. When comparing CPF LIFE vs private annuity plans Singapore, we look at how these moving parts affect your total liquidity.

Mastering SRS and Tax Relief

Your Supplementary Retirement Scheme (SRS) account is a powerful tool for 2026 tax planning. Contributions reduce your taxable income dollar-for-dollar. This is especially effective if your salary has hit the new S$8,000 monthly ceiling. By using SRS funds to purchase a private annuity, you're essentially funding your future with money that would have otherwise gone to taxes. It's a win-win for your current and future self.

Strategic withdrawal is key. You can refer to our guide on Mastering the SRS Account for a deeper dive. The goal is to spread withdrawals over a 10-year window to minimize the tax impact. This layer of income provides extra flexibility that you won't find in government schemes alone. It helps you stay in a lower tax bracket while maintaining a high standard of living.

Legacy Planning with Annuity Assets

Retirement isn't just about you. It's about the people you leave behind. While CPF LIFE provides lifelong income, the refund is limited to the remaining premium. Private annuities can be structured to provide a more robust inheritance. Through proper nomination and estate structuring, you can ensure your wealth protection goals extend to the next generation. This ensures your hard work benefits your family for years to come.

Effective Legacy Planning in Singapore requires a holistic view of all your assets. A financial planner ensures your annuity payouts align with your broader estate plan. This prevents legal hurdles and ensures a smooth cross-generational wealth transfer. If you're ready to integrate your tax savings with a lasting legacy, book a discovery session with us today. We're here to help you build a plan that's as unique as your family.

Why a Financial Planner Outperforms Digital Platforms

Digital platforms offer efficiency, but they can't handle the complexity of human emotion. When markets dip in 2026, a robo-advisor won't be there to provide behavioral coaching. A financial planner does more than just pick products. We look at your life goals first. This human connection is what sets Zenith Wealth apart. As authorized representatives of finexis advisory, we provide insights across multiple providers. We aren't tied to a single insurance brand. This independence is crucial when weighing CPF LIFE vs private annuity plans Singapore. It ensures your roadmap is built on objective data and personal context.

We combine this human touch with sophisticated tools like i12 investments. While an algorithm might group you into a generic risk category, we curate your strategy based on your actual retirement needs. We've seen how market corrections can rattle even the most disciplined investors. Having a partner to guide you through these transitions makes all the difference. We move beyond simple "product picking" to create a comprehensive, goal-based strategy that adapts to your life.

The Zenith Wealth Approach

Our process starts with a deep dive into your current financial health. We audit your CPF balances and existing private insurance policies to find hidden gaps. Most online calculators give you a generic "Retirement Number" that ignores your specific lifestyle aspirations. We customize this number to reflect your real-world costs and inflation expectations for 2026. Zenith Wealth provides the boutique, localized expertise needed to navigate Singapore's unique regulatory environment with a personal touch. We don't just hand you a report; we build a living document that evolves alongside your family.

Take the Next Step Toward Security

Ready to move from uncertainty to clarity? Preparing for your first consultation with a Zenith Wealth financial consultant is straightforward. To get the most out of our session, bring along your latest CPF statements and any existing insurance policy summaries. This allows us to perform a truly holistic retirement review. We'll look at how your curated assets can complement your annuity floor to create a resilient income stream. It's time to stop guessing and start planning with a partner who values your future as much as you do. Contact a Zenith Wealth financial planner for a personalized retirement review to begin your journey toward a secure, inflation-hedged lifestyle.

Take Control of Your Retirement Future

Your retirement strategy shouldn't be left to chance or cold algorithms. Balancing CPF LIFE vs private annuity plans Singapore requires a proactive approach that layers guaranteed income with curated growth. By integrating the security of government schemes with the flexibility of private wealth and i12 investments, you can build a lifestyle that actually beats inflation. We focus on human connection to ensure your roadmap is as unique as your personal goals.

As an authorized representative of finexis advisory, Zenith Wealth offers a boutique, human-centric experience. We specialize in i12 investment curation to help you find the right risk-adjusted returns for the 2026 landscape. A dedicated financial planner can help you navigate these complex wealth transitions with quiet confidence. Don't let complexity hold you back from the security you've worked so hard to achieve. It's time to bridge the gap between basic payouts and your dream lifestyle.

Secure Your Future with a Custom Retirement Strategy today. We're ready to start the conversation whenever you are.

Frequently Asked Questions

What is the main difference between CPF LIFE and a private annuity plan?

The primary difference lies in the funding source and flexibility. CPF LIFE uses your CPF Retirement Account savings and is a mandatory national scheme for most Singaporeans. Private plans are funded using cash or SRS contributions. While CPF LIFE provides a government-guaranteed floor, private plans offer customizable payout ages and the potential for higher growth through participating fund dividends.

Can I use my SRS funds to purchase a private retirement annuity?

Yes, you can use your Supplementary Retirement Scheme (SRS) funds to purchase licensed private annuity plans. This is an effective way to lower your 2026 tax bracket while putting your idle SRS cash to work. Since SRS funds in a bank account earn very little interest, moving them into an annuity can help you build a more robust income stream for the future.

Is it possible to have both CPF LIFE and a private annuity plan?

It's absolutely possible and often recommended for a comprehensive retirement strategy. Having both allows you to use CPF LIFE as your foundational security for basic needs while the private annuity covers your "lifestyle gap." This combination ensures you have a guaranteed floor and a flexible ceiling to fund your desired retirement activities.

Do private annuity plans in Singapore provide better returns than CPF LIFE?

Private plans don't necessarily offer higher guaranteed returns, but they provide non-guaranteed bonuses that can boost your total payout. When comparing CPF LIFE vs private annuity plans Singapore, it's important to note that private plans are designed for flexibility and growth potential. They complement the government's risk-free floor by offering dividends that help your income keep pace with 2026 costs.

What happens to my private annuity if the insurance company goes bust?

Your private annuity is protected under the Policy Owners’ Protection (PPF) Scheme. This scheme is administered by the Singapore Deposit Insurance Corporation (SDIC) and covers all licensed life insurers in Singapore. It provides a safety net for your guaranteed benefits, ensuring that your retirement security remains intact even if an insurer faces financial failure.

Can I start my private annuity payouts before the age of 65?

Yes, one of the biggest advantages of private plans is that you can choose an earlier payout start age. Most private annuities allow you to begin receiving monthly income at age 50 or 55. This makes them a vital tool for bridging the income gap if you plan to stop working before your CPF LIFE payouts begin at 65.

Are i12 investments suitable for conservative retirees?

i12 investments are very suitable for conservative retirees because they focus on human-led curation rather than generic algorithms. These investments prioritize manager quality and downside protection to help safeguard your capital. A financial planner can help you select specific i12 funds that match your risk tolerance while still providing a hedge against 2026 inflation.

How does inflation in 2026 affect my CPF LIFE payouts?

Inflation can reduce the real-world value of your monthly payouts over time. While the CPF LIFE Escalating Plan offers a 2% annual increase, this might not fully cover the rising costs of private healthcare or lifestyle expenses in 2026. Supplementing your CPF with private annuities or i12 investments helps ensure your purchasing power remains strong throughout your retirement years.