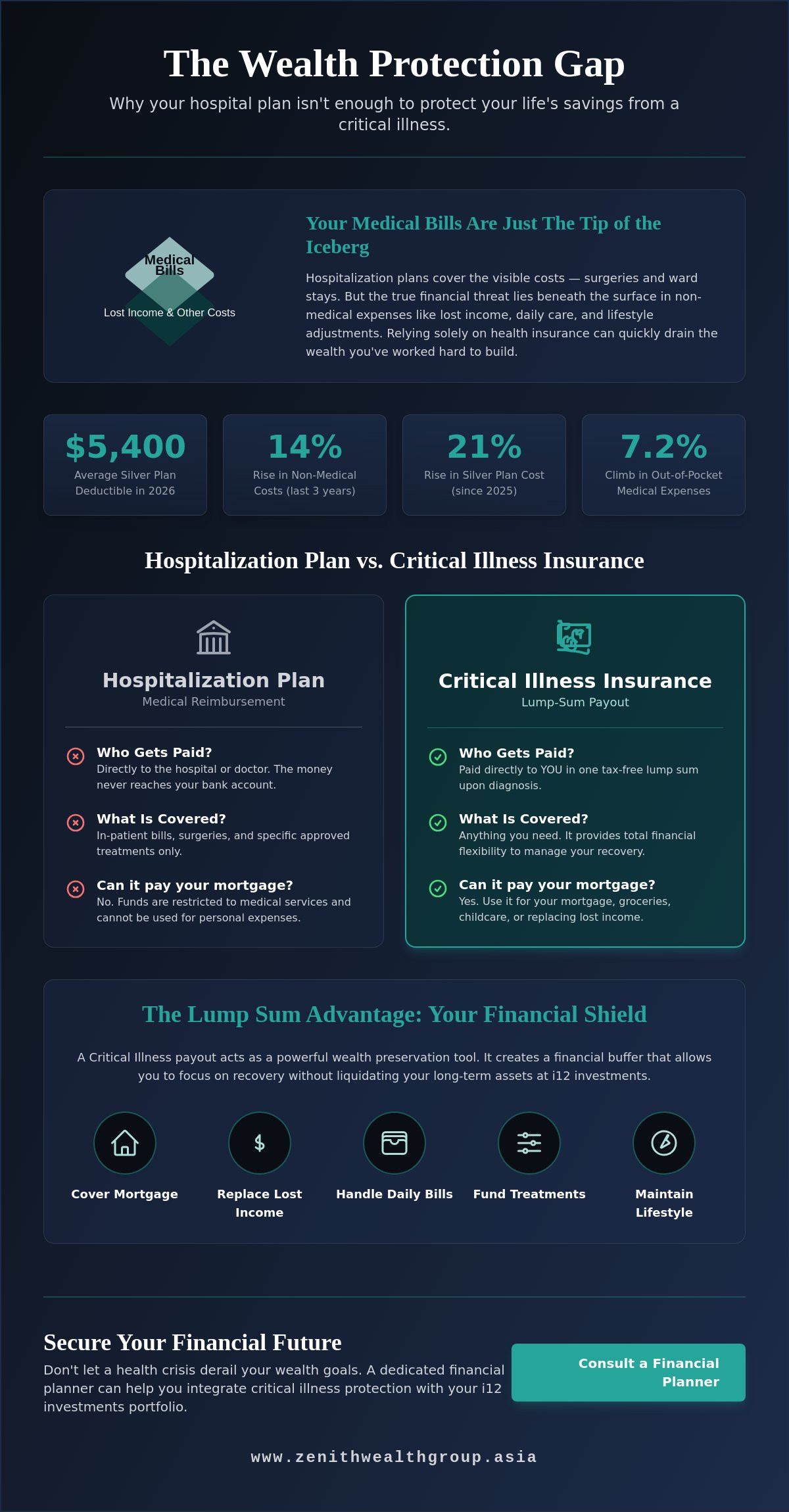

What if your hospitalization plan is actually leaving your life savings vulnerable? Many people believe that medical coverage is enough to handle a major diagnosis, but medical bills are often just the tip of the iceberg. In 2026, the average silver plan deductible has reached $5,400, and non-medical costs like lost income and daily care have risen by 14% over the last three years. Relying solely on health insurance can quickly drain the wealth you've worked so hard to build.

At i12 investments, we see critical illness insurance as a vital wealth preservation tool, not just a medical supplement. You likely feel that your current coverage is sufficient, but the gap between reimbursement and real-world recovery costs is widening. This article provides a comprehensive checklist to help you identify coverage gaps and secure your financial future against major health setbacks.

We'll clarify the difference between medical reimbursement and lump-sum payouts while providing a framework to calculate your ideal sum assured. Our financial planners will show you how to choose a plan that aligns perfectly with your long-term wealth goals.

Key Takeaways

- Learn why traditional health insurance isn't enough to cover lost income and how critical illness insurance provides the cash injection needed for a full recovery.

- Discover the hidden risks of relying on corporate coverage and how to bridge the "wealth protection gap" with portable, personal plans.

- Use our 5-step checklist to calculate your specific 'Income Replacement Number' based on three to five years of annual expenses.

- Identify why early-stage coverage is essential in 2026 for modern diagnostics and how it prevents minor health setbacks from becoming financial crises.

- See how integrating protection with i12 investments creates a robust foundation for your long-term wealth management and legacy planning.

What is Critical Illness Insurance and Why Does it Matter in 2026?

Understanding What is Critical Illness Insurance is the first step toward building a resilient financial plan. Unlike hospitalization plans that reimburse specific medical bills, critical illness insurance provides a one-time, lump-sum cash payout upon the diagnosis of a covered condition. Think of it as an income replacement tool rather than a bill-paying tool. In 2026, this distinction is vital. With the average Silver health insurance plan cost rising 21% since 2025 and out-of-pocket medical expenses climbing by 7.2%, your cash reserves face significant strain.

For families, this insurance serves as the bedrock of wealth protection. While MediShield Life and Integrated Shield plans handle the hospital ward, they don't address the mortgage, groceries, or school fees while you're unable to work. At Zenith Wealth, we view this payout as a strategic asset that keeps your retirement trajectory on track. It stops you from liquidating long-term investments at i12 investments just to cover daily living costs. A dedicated financial planner can help you integrate this with your broader portfolio to ensure no gaps exist.

The Lump Sum Advantage: Flexibility Beyond Hospital Bills

Once the payout arrives, the money is yours to use as you see fit. You can pay down your mortgage, cover childcare costs, or seek experimental treatments not covered by standard plans. This financial liquidity provides massive psychological relief. Instead of worrying about how to keep the lights on, you can focus on your recovery. It's about maintaining your family's lifestyle during a crisis. Traditional savings are often insufficient because the average silver plan deductible in 2026 has reached $5,400. Additionally, non-medical costs have risen by 14% compared to three years ago. This flexibility is why we consider it the foundation of any serious wealth protection plan.

LIA Definitions: The 37 Standard Severe Illnesses

In Singapore, the Life Insurance Association (LIA) provides standard definitions for 37 severe-stage illnesses. This standardization ensures transparency across different providers. You know exactly what qualifies for a claim. Major cancers, heart attacks, and strokes are the most common conditions covered. However, these definitions often require a severity threshold to be met. This is why a financial planner will often recommend looking beyond the standard list to include early-stage coverage. You shouldn't have to wait for a condition to worsen before receiving financial support. Standardized definitions protect you from fine-print surprises, but they're just the starting point for a comprehensive critical illness insurance policy.

The Wealth Protection Gap: CI Insurance vs. Hospitalisation Plans

Many Singaporeans believe their Integrated Shield Plan is a complete safety net. It isn't. Hospitalization plans are designed to pay the doctors and the wards. They don't put a single cent into your bank account for daily expenses. This creates a dangerous wealth protection gap. If a major illness strikes, your medical bills might be covered, but your mortgage, school fees, and grocery bills still need to be paid. Without critical illness insurance, you're forced to dip into your retirement savings or your portfolio at i12 investments to survive.

The most common objection we hear is that "company insurance is enough." This is a risky assumption. Corporate coverage is rarely portable. If you're too ill to work, you may lose your job and your insurance simultaneously. Relying on an employer for your primary protection is like building a house on a foundation you don't own. A comprehensive guide to critical illness insurance highlights that personal ownership of your policy is the only way to ensure the buffer remains intact regardless of your employment status.

US inflation also plays a silent role in your long-term strategy. It erodes the purchasing power of your future payout. If your plan doesn't account for these rising costs, your recovery runway might be shorter than you think. Our financial planners at Zenith Wealth can help you stress-test your current coverage against these future realities.

Comparing Coverage: Medical vs. Critical Illness

Who gets paid?

- Hospital Plan: Paid directly to the medical institution or doctor.

- CI Insurance: Paid directly to you in cash.

What is covered?

- Hospital Plan: In-patient bills, surgeries, and specific outpatient treatments.

- CI Insurance: Mortgage, groceries, supplements, and general lifestyle maintenance.

When does support end?

- Hospital Plan: Usually ends upon discharge from the hospital.

- CI Insurance: Continues through your recovery until the policy term ends or the sum is paid.

The Hidden Costs of Recovery

Recovery is expensive. It's not just about the surgery. It's about the recovery runway your family needs to stay afloat while you focus on getting better. You may need to hire domestic help or specialized caregivers during home recovery. You might need expensive nutritional adjustments or home modifications that standard medical plans won't cover. These costs require immediate cash flow that hospitalization plans simply don't provide. A critical illness insurance payout ensures that your long-term wealth goals stay on track while you handle these immediate needs.

Early Stage vs. Severe Stage: Choosing the Right Depth of Cover

Traditional critical illness insurance often contains a "severity gap." This means the policy only pays out when a condition reaches an advanced or life-threatening stage. In the past, this was the standard. Today, medical technology allows us to detect illnesses much earlier. If your plan only covers severe stages, you might find yourself in a difficult position. You're sick enough to need time off work, but not "sick enough" to trigger a payout. This is why many people in 2026 are shifting toward more comprehensive depth of cover.

As of January 2026, there has been an 18% increase in people seeking critical illness insurance to supplement their existing basic coverage. This trend is driven by a desire to close that severity gap. Many modern plans are expanding their reach. They now include conditions like early-stage Parkinson's and severe organ failure. Choosing the right depth of cover involves a trade-off. While broader coverage stages usually mean higher premiums, the protection they offer during the early, most treatable phases of an illness is often worth the investment.

Early Stage CI: Catching it Before it Escalates

Early detection is a medical blessing but can be a financial challenge. For example, Stage 0 cancer or "carcinoma in situ" often requires immediate treatment and rest. However, standard plans typically won't cover these diagnoses. Taking a six-month sabbatical for treatment can devastate your cash flow. A financial consultant can help you evaluate whether your current portfolio at i12 investments can weather such a storm or if an early-stage rider is necessary. It's about ensuring you have the funds to stop working and focus on recovery the moment you get the news, not six months too late.

Multi-Pay Policies: Protection for the Long Haul

Modern medicine is keeping people alive longer, but this also increases the risk of relapses or secondary illnesses. Traditional policies often terminate after a single major claim. Multi-pay policies solve this by allowing for multiple claims over time. These plans use "reset" and "survival" periods to manage how often you can claim. For parents, this is a game-changer. It ensures lifelong insurability for children, even if they face a health hurdle early in life.

There is also a direct link between these robust plans and legacy planning. A multi-pay plan ensures that a recurring illness doesn't consume the inheritance you intend to leave behind. It keeps your primary wealth intact while the insurance handles the recurring costs of care. Talk to your financial planner about how to layer these protections into your long-term strategy.

Your Critical Illness Planning Checklist: 5 Steps to Secure Your Future

Securing your wealth requires more than just buying a policy. It demands a tactical approach. Use this checklist to ensure your critical illness insurance strategy is actually robust enough for 2026.

- Audit your current coverage: Look at your personal plans, corporate benefits, and what you've set aside for dependents.

- Calculate your 'Income Replacement Number': Aim for three to five years of annual income to provide a proper recovery window.

- Assess your family medical history: Identify specific risks like heart disease or cancer to tailor your coverage depth.

- Review your cash flow: Ensure you can maintain premium payments comfortably into your 60s.

- Consult a professional: Align your coverage with your strategy for i12 investments to prevent portfolio erosion.

Step 1: The Income Replacement Formula

The standard rule of thumb is to secure a sum assured equal to five times your annual income. This isn't just a random number. It factors in your outstanding debts, mortgage balance, and future education funding for your children. You must also adjust this figure for projected 2026 inflation rates. With out-of-pocket medical costs rising by 7.2% this year, a payout that felt large in 2020 might be insufficient today. Your goal is to keep your family's lifestyle unchanged while you recover.

Step 2: Evaluating Policy Features

Not all policies are equal. A 'Waiver of Premium' rider is a non-negotiable feature. It ensures that if you are diagnosed, your future premiums are waived while the coverage continues. You should also distinguish between 'accelerated' and 'additional' payouts. An accelerated benefit deducts the CI payout from your death benefit, while an additional benefit pays out separately. Finally, decide between Term and Whole Life. Term plans often provide higher coverage for lower costs during your peak earning years. Whole Life plans offer permanent protection and cash value. A financial planner can help you decide which structure fits your retirement timeline best.

Ready to bridge the gaps in your coverage? Speak with a financial consultant today to build a plan that protects your wealth for the long haul.

Integrating Protection with Zenith Wealth and i12 Investments

At Zenith Wealth, we view wealth management as a pyramid. Critical illness insurance sits at the very base. Without this foundation, the rest of your financial structure remains vulnerable to sudden collapse. While your portfolio at i12 investments works to grow your capital, your insurance ensures you never have to liquidate those assets prematurely. It's about creating a closed loop of protection. This way, your long-term wealth goals remain intact even if your health takes an unexpected turn.

i12 investments provides a strategic edge in this ecosystem. It helps you grow a secondary emergency fund that works in tandem with your insurance payouts. This dual-layered approach is essential in a market where medical inflation continues to outpace general savings. By integrating your protection and investment strategies, you ensure that a medical crisis doesn't become a financial one. Regular reviews with a dedicated financial planner keep this balance precise as your life stages change.

The Role of a Financial Consultant

Comparing providers like Singlife and other major insurers can be a complex task for any individual. A financial consultant simplifies this process by providing a clear, side-by-side analysis of policy fine print. We don't just look at the premiums; we look at how the definitions align with your specific risks. Your plan must evolve as you move from a young professional to a pre-retiree. We focus on ensuring your CI strategy complements your retirement planning. This coordination prevents insurance overlap where you pay for coverage you don't need while leaving major gaps elsewhere.

Secure Your Legacy Today

The greatest risk in wealth protection is waiting too long. Uninsurability is a real threat; a single minor health discovery during a routine check-up can make it impossible to get coverage later. Committing to a plan now locks in your insurability and keeps your premiums manageable. Furthermore, a well-protected portfolio gives you the psychological freedom to pursue more aggressive investment strategies. You can afford to take calculated risks with your capital because you know your family's basic needs are already secured.

Don't leave your hard-earned wealth to chance. Transitioning from awareness to a secured plan is a straightforward process when you have the right guide. Book a consultation with a Zenith financial consultant today to review your CI gap and ensure your legacy is protected for 2026 and beyond.

Secure Your Financial Resilience for 2026

Protecting your wealth is a continuous journey. You now understand that critical illness insurance isn't just another monthly expense; it's the safety net that keeps your long-term goals on track. By calculating your income replacement number and bridging the gap between hospitalization plans and real-world recovery costs, you've taken a vital step toward true financial security. Integrating these protections with your i12 investments ensures that a health setback never forces you to compromise on your family's future or your retirement dreams.

Our team members are authorised representatives of finexis advisory. We specialize in i12 investments and creating customized retirement and legacy roadmaps that adapt as your life evolves. Don't wait for a medical diagnosis to discover the gaps in your coverage. We're here to help you build a plan that is both robust and sustainable. Secure your wealth protection strategy with a Zenith financial consultant today. We're ready to start the conversation and grow alongside you.

Frequently Asked Questions

Is critical illness insurance compulsory for Singaporeans?

No, critical illness insurance is not compulsory for Singaporeans. While MediShield Life is mandatory for all citizens and permanent residents, it only covers hospital bills and specific outpatient treatments. CI insurance is a voluntary supplement designed to provide a cash payout for living expenses, ensuring your family stays financially stable if you can't work.

Can I use MediSave to pay for my critical illness insurance premiums?

Generally, you cannot use MediSave to pay for standalone CI insurance premiums. MediSave is reserved for Integrated Shield Plans, ElderShield, and CareShield Life. Most CI policies require cash payments. It's best to speak with a financial planner to see if any of your existing life insurance riders have different payment structures.

What is the difference between early stage and severe stage CI?

The difference lies in the severity of the diagnosis required to trigger a payout. Early-stage plans pay out for minor conditions, such as Stage 0 or Stage 1 cancer, allowing for immediate treatment. Severe-stage plans only pay out when the illness reaches an advanced state. Having both ensures you have financial support at every point of your recovery.

How much critical illness coverage do I actually need in 2026?

A reliable rule of thumb is to secure a sum assured equal to three to five years of your annual income. This provides a sufficient buffer to cover daily expenses and specialized care without needing to liquidate your i12 investments. Your specific needs will depend on your current debts and the number of dependents you support.

Does critical illness insurance cover pre-existing medical conditions?

Most insurers exclude pre-existing medical conditions from new policies. If you have a chronic illness or a previous major diagnosis, the insurance company may apply an exclusion or a premium loading. This is why it's vital to secure coverage while you're healthy to ensure your wealth protection remains comprehensive and affordable.

What happens to my CI policy if I never make a claim?

This depends on the type of policy you've selected. Term plans typically expire with no value at the end of the coverage period. However, whole life policies often accumulate a cash value or include a death benefit. This ensures that even if you never make a CI claim, the policy still contributes to your legacy planning.

Is company group CI insurance enough for my family?

Company insurance is rarely enough because it isn't portable. If you're forced to leave your job due to illness, your coverage usually ends when you need it most. Personal policies provide a permanent safety net that stays with you regardless of your career moves, offering much more reliable protection for your family's future.

How does US inflation affect my long-term CI payout value?

US inflation erodes the purchasing power of your future payout over time. Since global costs and many investment assets are influenced by the dollar's value, a fixed sum set today may not cover the same lifestyle needs in the future. A financial consultant can help you review and adjust your sum assured to keep pace with these economic shifts.