What if the person you trust with your retirement is actually the biggest obstacle to your wealth? Many investors find themselves wondering exactly when to switch financial advisors in the Philippines as they notice proactive updates dwindling during market shifts. It's frustrating to feel like your portfolio is on autopilot while hidden fees slowly chip away at your net returns. You deserve a financial planner who treats your legacy with the urgency it requires.

We understand that changing your advisory relationship feels like a daunting task. However, staying with a financial consultant who offers generic sales pitches instead of a bespoke plan can be far more costly in the long run. This 2026 strategic guide helps you spot the warning signs of a stagnant partnership and provides a clear path toward a more modern approach. You'll learn how to align your wealth with the i12 investments framework and secure a partner dedicated to transparent, proactive retirement planning. Let's start the conversation about your financial future today.

Key Takeaways

- Identify the critical warning signs of a stagnant relationship, including a lack of proactive communication and opaque fee structures that erode your returns.

- Learn exactly when to switch financial advisors in the Philippines by auditing your current professional standards against SEC compliance and the i12 investments framework.

- Evaluate the "cost of inaction" by comparing traditional commission-based models with modern, fee-based comprehensive planning for better portfolio growth.

- Discover the "No-Awkwardness" method for transitioning to a new financial planner without disrupting your wealth protection or legacy planning goals.

- Explore how a regional perspective across Singapore and the Philippines provides a more robust approach to retirement and business succession planning.

5 Critical Red Flags: When to Switch Your Financial Planner in the Philippines

Choosing a professional to manage your wealth is one of the most significant decisions you'll make for your future. Knowing exactly when to switch financial advisors in the Philippines is a strategic necessity for anyone serious about wealth protection. Your financial planner should be an active participant in your success. If they've become a silent partner, your wealth is likely at risk. Many investors stay in stagnant relationships because they fear the transition process, but the cost of inaction is often far higher than the effort of moving.

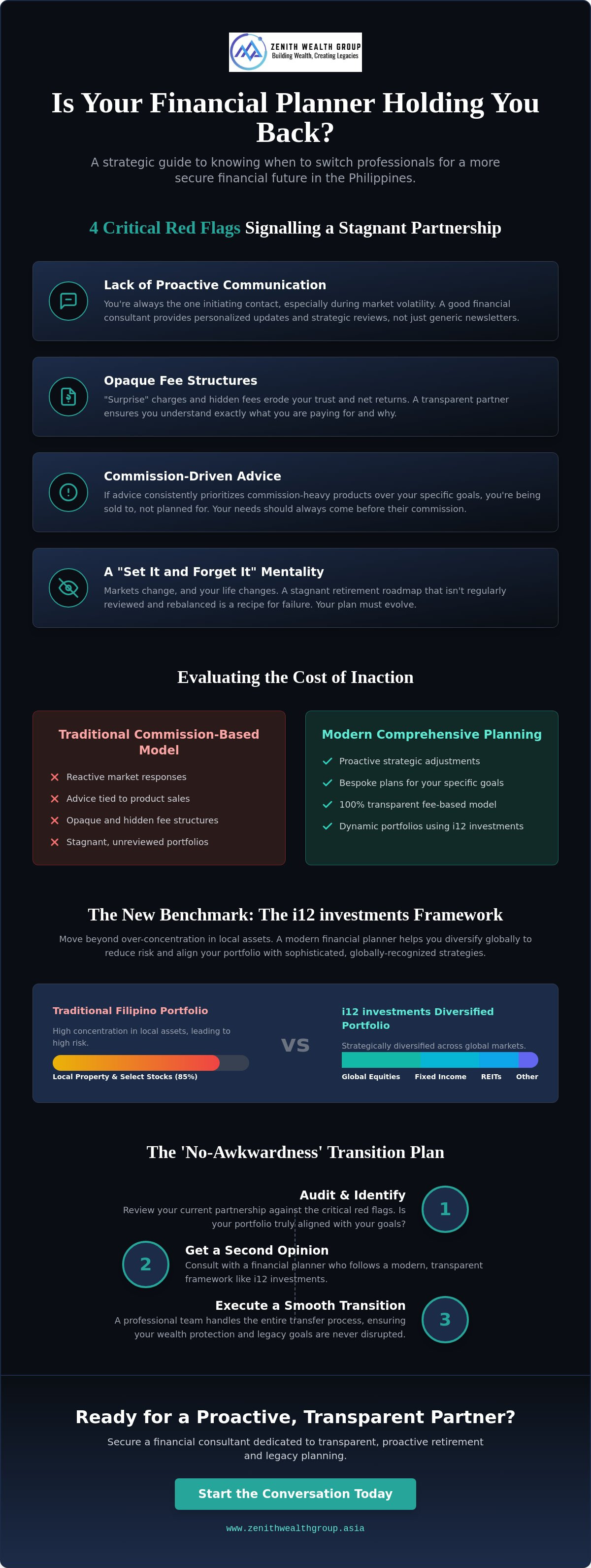

There are four major warning signs that suggest your current partnership has run its course. First, a persistent lack of proactive communication during market shifts is unacceptable. If you're the one constantly reaching out for updates when the PSEi is volatile, your consultant isn't doing their job. Second, opaque fee structures or "surprise" charges that weren't disclosed upfront erode trust and net returns. Third, if the advice you receive consistently prioritizes commission-heavy products over your specific goals, you're being sold to, not planned for. Finally, a "set it and forget it" mentality regarding your retirement roadmap is a recipe for failure. Markets change, and your plan must evolve with them.

The "Ghosting" Effect: Communication vs. Silence

Communication is the heartbeat of a healthy advisory relationship. A dedicated financial consultant should respond to your inquiries within one business day. There is a massive difference between receiving a generic, automated newsletter and a personalized portfolio review that addresses your unique concerns. If you only hear from your planner when a policy is up for renewal or when they have a new product to pitch, it's a major red flag. You deserve a partner who initiates contact to discuss how global trends or local regulatory changes might impact your wealth.

Performance vs. Strategy Misalignment

A single year of bad returns isn't always a reason to switch. Markets fluctuate, and even the best portfolios experience downturns. However, a lack of strategy is a dealbreaker. You need to evaluate if your risk appetite has outgrown your current consultant's tools. In a volatile Philippine market, regular rebalancing is essential. If your portfolio is drifting away from your original goals without a clear explanation or adjustment, it's time to look for a more proactive approach. Modern frameworks like i12 investments focus on this strategic alignment, ensuring your portfolio remains robust regardless of short-term market noise.

If these red flags feel familiar, don't wait for a market crash to take action. You can reach out to us today to discuss a more transparent, proactive approach to your financial future. It's time to partner with a team that values human interaction and professional integrity as much as you do.

Evaluating Professional Standards: From SEC Compliance to i12 investments

Professionalism in wealth management is evolving. It's no longer enough to rely on a "gut feeling" or a long-standing personal connection. As the Philippine financial landscape matures, your expectations should rise accordingly. Knowing when to switch financial advisors in the Philippines often starts with a simple question: Is your consultant following a rigorous, globally recognized framework, or are they just reacting to the news cycle? A modern financial planner must bridge the gap between local regulatory requirements and sophisticated investment strategies.

The shift from basic product intermediation to holistic financial planning is now the industry standard. This means your advisor shouldn't just sell you a policy. They should be managing your transition into a comprehensive wealth strategy that includes retirement planning, wealth protection, and legacy planning. If your current relationship feels transactional, it might be time to explore a more collaborative partnership that prioritizes your long-term objectives over short-term sales targets.

Regulatory Due Diligence in the Philippines

Verifying your consultant's credentials is your first line of defense. Any individual providing financial advice must be registered with the Securities and Exchange Commission (SEC). In 2026, the SEC implemented Memorandum Circular No. 8, Series of 2026, which modernized filing and adjudication procedures to ensure greater transparency. You should also confirm their standing with the Insurance Commission (IC) if they handle your wealth protection needs. A licensed financial consultant has a clear ethical obligation to act in your best interest. The presence of unregistered investment schemes or a lack of verifiable licensing is a non-negotiable reason to walk away immediately.

i12 investments: A Benchmark for Portfolio Quality

i12 investments represents a shift toward structured, portfolio-based advice. This framework moves beyond the traditional Filipino tendency to over-concentrate wealth in local property or a few select stocks. By adopting the i12 investments approach, a financial planner helps you diversify into global equities, fixed income, and REITs. This methodology reduces your exposure to purely local market risks and aligns your portfolio with modern professional standards. When you evaluate when to switch financial advisors in the Philippines, ask if your next partner is familiar with this strategic entity. If they aren't, they might be leaving your wealth vulnerable to avoidable volatility. A framework-driven strategy ensures that every decision is backed by data, not just a hunch.

The Financial Impact of Staying vs. Switching Financial Consultants

Choosing to remain with a subpar advisor isn't a neutral decision. It's a choice that carries a measurable price tag. When you consider when to switch financial advisors in the Philippines, you're looking at more than just a change in personnel. You're analyzing the "cost of inaction." Staying with a consultant who provides generic advice or fails to rebalance your portfolio leads to lost growth opportunities that can never be recovered. Over a decade, even a small lag in performance due to poor strategy can result in millions of pesos of missed wealth.

A proactive financial planner does more than just pick stocks. They look at your entire financial ecosystem, including tax efficiency and estate planning. If your current advisor hasn't discussed how the 2026 tax reforms impact your investment management, you're likely experiencing unnecessary tax leakage. This invisible drain on your resources makes it harder to reach your goals, regardless of how well the market performs. It's time to stop settling for "good enough" and start demanding a strategy that maximizes your net returns.

Fee Transparency: What are you actually paying?

Many investors in the local market don't realize how much they're truly paying for their advice. Traditional commission-based models often include "hidden" management fees and entry loads that aren't immediately obvious. A mere 1% difference in annual fees might seem trivial today. However, over a 20-year retirement horizon, that single percentage point can reduce your final nest egg by significant margins. Opaque fee structures in the Philippines represent a silent tax on your future that transfers your potential wealth directly to the institution instead of your family.

Portfolio Efficiency and i12 investments

Strategic wealth analysis is about more than just chasing the latest trend. It's about building a resilient engine for your wealth. Integrating the i12 investments framework helps reduce unnecessary volatility by ensuring your assets aren't all moving in the same direction at once. This structure is particularly vital for retirement planning and wealth protection. While some worry about the professional fees of a high-quality financial planner, these costs are negligible compared to the price of an unprotected financial crisis. A proactive partner ensures you're prepared for the unexpected, keeping your legacy intact through any market cycle.

How to Transition to a New Financial Planner Without Disrupting Your Wealth

Deciding when to switch financial advisors in the Philippines is only the first step. The actual transition requires a clinical approach to your current contracts. Start by conducting a final audit of your existing agreements. Look for exit clauses or surrender charges, especially within Variable Universal Life (VUL) policies. These insurance-linked investments are notorious for high early-exit costs. Your new financial planner should help you weigh the cost of these charges against the potential for better growth under a new strategy.

The "No-Awkwardness" method for notifying your current consultant is simple: keep it professional and brief. You don't owe a lengthy explanation for wanting to align with modern frameworks like i12 investments. A standard email stating that you're moving your accounts to a firm that better fits your current needs is sufficient. This clarity prevents unnecessary sales pressure and allows you to focus on the future of your wealth protection.

The Paperwork: Navigating Local Transfers

Transferring assets in the Philippine banking system involves specific timelines. Redemptions for local mutual funds usually take three to seven banking days. However, changing the servicing agent on an insurance policy can be more complex. You'll need to coordinate with the Insurance Commission (IC) guidelines to ensure your coverage remains active during the shift. If you own a business with assets over ₱3 million, remember that new SEC rules for 2026 have streamlined filing procedures. This makes it easier to update your resident agent or corporate records if your financial consultant also handles your business succession planning. Contact our team for a seamless transition audit to ensure no asset is left behind.

Onboarding with a New Perspective

Your first session with a new financial consultant should feel like a fresh start. Expect a comprehensive "Fact Find" session that goes beyond just your income and expenses. This is where you align your roadmap with i12 investments principles to ensure global diversification. You should also define your communication cadence on Day 1. Whether you prefer monthly video calls or quarterly in-person reviews, setting these standards early ensures you'll never feel "ghosted" again. This proactive reporting is what distinguishes a modern partner from a traditional salesperson.

Zenith Wealth Group: Proactive Financial Planning for the Modern Filipino Investor

At Zenith Wealth Group, we don't just manage assets. We build lasting partnerships. If you've been questioning when to switch financial advisors in the Philippines, you're likely looking for more than a new name on your account. You're looking for a higher standard of care. Our approach is built on quiet confidence and an open-door policy. We prioritize human interaction alongside professional advisory services, ensuring you never feel like just another number in a corporate database. We're an attentive team that's eager to start a conversation about your future.

Our commitment to the i12 investments framework ensures your portfolio is built for robust growth. We move away from the jargon-heavy atmosphere of traditional firms. Instead, we offer clear, action-oriented advice that makes sense for your life. For pre-retirees, this means having a proactive partner who anticipates market shifts before they impact your retirement roadmap. We value efficiency and clarity, ensuring your path to financial security is unobstructed by unnecessary complexity or hidden fees.

Cross-Border Expertise for Long-Term Security

Our Singaporean roots provide a wider lens for your wealth protection. We understand that modern investors often have interests that span across borders. By integrating global investment management with your local Philippine goals, we offer a level of security that localized firms often miss. This regional perspective is vital for navigating the evolving regulatory landscape of 2026. You can contact our financial planners for a portfolio audit to see how we can align your current assets with a more global strategy. We're ready to engage and grow alongside you.

Your Partner in Generational Wealth

Moving from simple savings to strategic legacy planning requires a shift in mindset. It's about protecting what you've built for the people you love most. We use the i12 investments framework to ensure your family's future is safeguarded against volatility. This isn't just about the here and now. It's about building a bridge to the next generation. If you're interested in how these strategies work in other markets, check out The 2026 Guide to Legacy Planning in Singapore and Beyond. Our role as your Modern Professional Guide is to make this process transparent, approachable, and effective.

We invite you to experience a different kind of advisory relationship. One where your financial planner is as invested in your success as you are. Let's move beyond the coldness of institutional planning. Reach out to us today to start your transition toward a more proactive, human-centered financial future.

Take Control of Your Financial Future

Your wealth deserves more than a "set it and forget it" approach. You've seen how critical red flags, from communication silence to hidden fees, can derail your long-term goals. Transitioning to a strategy built on the i12 investments framework ensures your portfolio remains resilient against market volatility. Deciding when to switch financial advisors in the Philippines is a strategic move that prioritizes your family's security over a stagnant professional relationship.

We're here to make that transition seamless and rewarding. As authorised representatives of finexis advisory, our team brings specialized expertise in multi-stage retirement planning and i12 investments frameworks. We don't just offer advice; we offer a partnership that grows with you. It's time for a transparent, proactive partner who values your legacy as much as you do.

Ready for a more proactive partnership? Book a consultation with a Zenith financial planner today

Let's start building a more secure future together. Our doors are open and we're ready to listen.

Frequently Asked Questions

Do I have to tell my old financial consultant why I am leaving?

You aren't required to provide a detailed explanation when ending your professional relationship. A brief, polite notification that you're moving your accounts to a firm that better aligns with your current needs is standard practice. This approach keeps the transition clean and avoids unnecessary sales pressure. Keeping it professional allows you to focus on your new strategy without the stress of an uncomfortable exit interview.

Will I lose money on my insurance policies if I switch advisors in the Philippines?

Switching advisors doesn't automatically mean losing money, but you must review your surrender charges first. Many Variable Universal Life (VUL) policies have high exit fees in the early years. However, you can often change the servicing financial consultant without liquidating the policy itself. Your new planner will audit these agreements to ensure your wealth protection remains intact while minimizing any potential financial impact from the change.

How long does the process of switching financial planners usually take?

The transition typically takes between two to four weeks depending on the complexity of your portfolio. While notifying your current consultant is immediate, transferring mutual funds or updating beneficiary records with the Insurance Commission can take several banking days. A proactive financial consultant will manage this timeline for you. They'll ensure that your retirement planning and investment management remain stable throughout the administrative handover.

Can a Singapore-based firm like Zenith Wealth Group manage my Philippine assets?

Yes, we provide cross-border expertise that bridges Singaporean financial standards with local Philippine requirements. This regional perspective is a key factor for those deciding when to switch financial advisors in the Philippines. We help you manage local assets while providing a wider lens for wealth protection. Our team ensures that your Philippine-based investments are optimized within a broader, more secure global framework for long-term growth.

What is the difference between a commission-based and fee-based financial planner?

A commission-based financial planner earns income from the specific products they sell to you. In contrast, a fee-based model focuses on comprehensive planning where the consultant's compensation is tied to the value of the advice or assets under management. This often leads to more transparent fee structures. It ensures that your consultant's goals are directly aligned with your portfolio's growth rather than just making a one-time product sale.

Is it possible to have more than one financial consultant at the same time?

You can certainly work with multiple consultants, but it often creates a fragmented strategy. Having different planners manage separate pieces of your wealth can lead to over-concentration in certain sectors or conflicting tax strategies. Most high-net-worth investors prefer a single, proactive partner who understands their entire financial ecosystem. This holistic approach ensures that your retirement planning and legacy planning are fully synchronized for maximum efficiency.

How do i12 investments impact my current retirement strategy?

Integrating i12 investments into your strategy shifts your focus from reactive stock-picking to structured, long-term growth. This framework uses data-driven analysis to diversify your wealth across global markets, reducing your reliance on purely local assets. It's designed to build a more resilient retirement engine. By adopting this approach, your financial planner can better safeguard your legacy against market volatility and ensure your income lasts throughout your golden years.

What documents do I need to prepare before meeting a new financial consultant?

Prepare your latest investment statements, insurance policy contracts, and any existing estate planning documents. You'll also need records of your business assets if they exceed the ₱3 million SEC audit threshold. Having these ready allows your new financial planner to conduct a thorough audit of your current standing. This preparation ensures your first session is productive and focused on aligning your roadmap with modern standards like i12 investments.