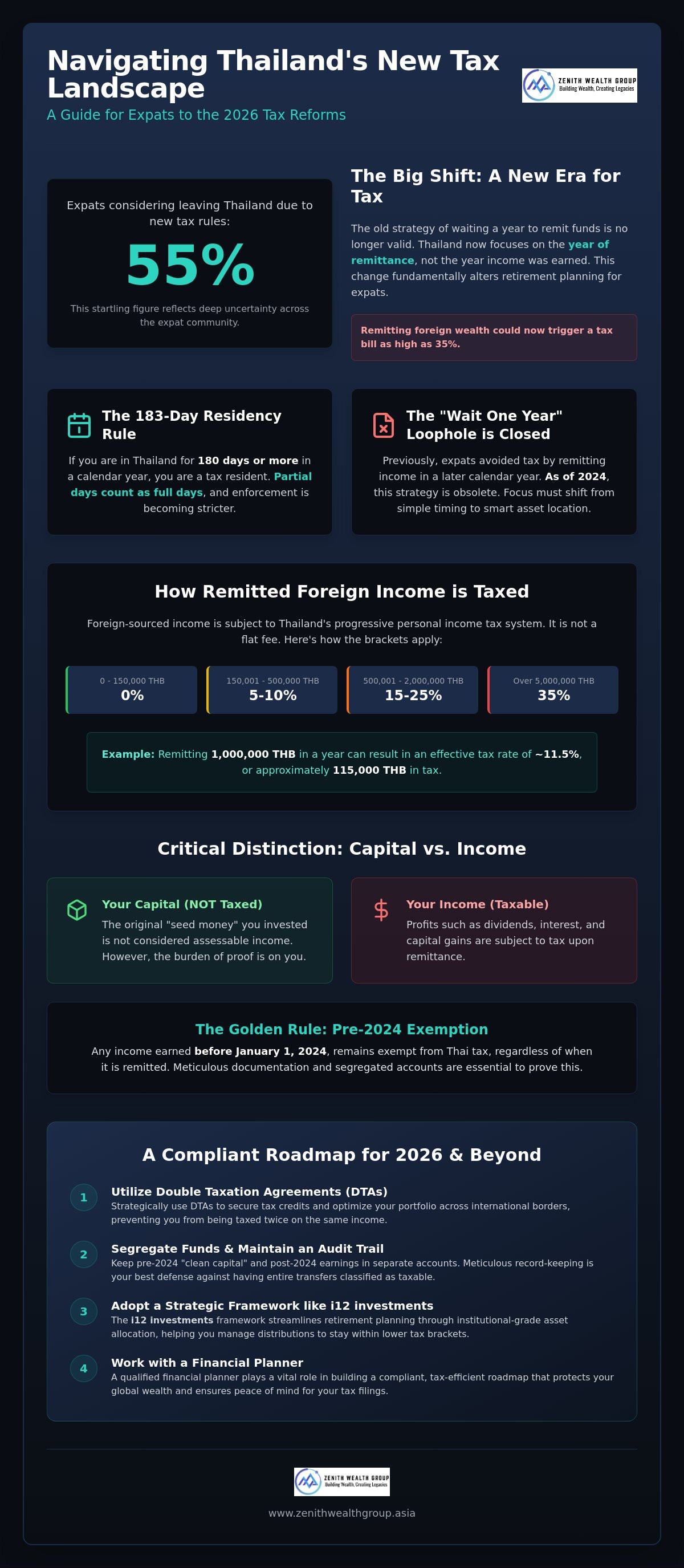

Did you know that 55% of expats have considered leaving Thailand due to the new foreign income tax rules? It's a startling figure that reflects the deep uncertainty felt across the community. You've likely spent years building a global portfolio, only to face a 2026 landscape where remitting your wealth could trigger a tax bill as high as 35%. It's natural to feel concerned about double taxation on your pensions or how to move funds without falling foul of stricter enforcement. Effective retirement planning for expats in Thailand now requires more than just timing your transfers; it demands a sophisticated approach to asset location.

We're here to help you navigate these changes with confidence. You'll discover how to master the 2026 reforms and use the i12 investments framework to structure your assets for maximum efficiency. This guide provides a compliant roadmap for fund remittance and the peace of mind you need for your upcoming tax filings. Let's look at how you can protect your lifestyle while staying fully aligned with the latest regulations.

Key Takeaways

- Master the 183-day residency criteria and the critical shift from year-of-earning to year-of-remittance taxation rules.

- Identify how Thailand’s progressive tax brackets, ranging from 0% to 35%, apply to your remitted foreign investment income.

- Explore how the i12 investments framework streamlines retirement planning for expats in Thailand through institutional-grade asset allocation.

- Learn to utilize Double Taxation Agreements to secure tax credits and optimize your portfolio across borders.

- Understand the vital role of a financial planner in building a compliant roadmap that protects your global wealth.

Navigating the 2026 Thai Tax Landscape for Expats

The ground shifted for retirees in 2024, and the dust is still settling in 2026. For decades, the strategy was simple: wait until the next calendar year to bring your money into the country. That era is over. The Thai Revenue Department now focuses on the moment of remittance rather than the year the income was generated. This change makes retirement planning for expats in Thailand more complex than ever before. You're no longer just managing investments; you're managing a timeline of capital movement that the authorities are watching closely.

The current interpretation of the Revenue Code classifies most foreign earnings as assessable income the moment they cross the border. This includes dividends, interest, and capital gains from your global accounts. While there is a proposed two-year grace period for income earned from 2024 onwards if remitted within a specific window, this remains a proposal as of July 2026. It hasn't been enacted into law yet. Relying on unconfirmed exemptions is a gamble you don't need to take. Instead, using frameworks like i12 investments helps ensure your portfolio is structured to handle these shifts without creating unnecessary tax events.

The 183-Day Rule: Are You a Resident?

Thai tax residency is straightforward but strictly enforced. If you stay in Thailand for 180 days or more in a single calendar year, you're a tax resident. The Revenue Department counts partial days as full days. It doesn't matter if you're just passing through or staying for a long holiday; those days add up quickly. This residency doesn't automatically end your tax liabilities in places like Singapore, which can lead to frustrating overlaps.

While Long-Term Resident (LTR) visa holders may enjoy specific exemptions, most retirees and digital nomads fall under the standard rules. The authorities are increasing cooperation with financial institutions to track these stays. It's a proactive environment. Working with a financial planner is the best way to determine your status before you trigger a surprise bill.

The Death of the Wait One Year Strategy

The "wait one year" loophole relied on a specific historical reading of Section 41. Looking at the History of Taxation in Thailand, we see a clear move toward a more globalized, transparent system. The old tricks simply don't work in 2026. Any foreign-sourced income brought into Thailand by a Thai tax resident is subject to personal income tax in the year it is remitted. This means your strategy must move away from simple timing. You need a robust plan that accounts for progressive tax brackets that can reach 35% on higher amounts. It's about smart asset location, not just waiting for the calendar to flip.

The Remittance Rule: How Foreign Investment Income is Taxed

Understanding the math behind your transfers is the next step in mastering retirement planning for expats in Thailand. When you bring foreign-sourced income into the country, it doesn't face a flat fee. Instead, it's funneled into Thailand's progressive personal income tax system. This means every dollar remitted is scrutinized to determine if it's fresh income or your original savings. Without a clear structure, you risk the Revenue Department classifying your entire transfer as taxable income.

A common concern is whether your initial principal investment is taxable. The short answer is no. Your capital, or the "seed money" you originally invested, is not considered assessable income. However, the burden of proof rests entirely on you. If you remit S$10,000 from a mixed account containing both original capital and accumulated dividends, the authorities may default to taxing the full amount. This is why segregating funds is no longer optional; it's a necessity for 2026 compliance.

Progressive Tax Brackets for 2026

The tax tiers for 2026 remain steep for high earners. While the first 150,000 THB (approximately S$5,500) is tax-free, the rates climb quickly. If you remit 1,000,000 THB in a calendar year to cover your living expenses, your effective tax rate sits around 11.5%, totaling roughly 115,000 THB in tax. For those remitting larger sums for property or luxury lifestyles, the top bracket of 35% applies to any amount over 5,000,000 THB. It's vital to calculate these liabilities before the funds leave your offshore account.

Distinguishing Between Capital and Income

Proving what is capital and what is profit requires a meticulous audit trail. The Revenue Department expects to see clear documentation of when the funds were earned. Remember, any income earned before January 1, 2024, remains exempt from Thai tax regardless of when you remit it. We often recommend using separate accounts to keep your pre-2024 "clean capital" away from new 2026 earnings.

Using the i12 investments framework allows for a more disciplined approach to these distributions. By focusing on rule-based triggers, you can manage your withdrawals to stay within lower tax brackets. A skilled financial planner can help you set up these structures to ensure your lifestyle remains funded without triggering an 35% tax event. Coordinating your portfolio with a professional ensures that your record-keeping meets the stringent standards of the 2026 Thai tax landscape.

Tax-Efficient Portfolio Construction with i12 investments

Building a portfolio that survives the 2026 tax environment requires more than just picking good stocks. It's about how those stocks are held. We use i12 investments as a core framework to help clients manage this complexity. This institutional-grade approach focuses on asset location as much as asset allocation. By using rule-based strategies, we minimize unnecessary "tax events" that occur when you buy or sell assets in a standard retail account.

Traditional retirement planning for expats in Thailand often gets bogged down by the mechanics of remittance. The i12 framework solves this by creating a clear structure for your global wealth. It allows your portfolio to grow in a tax-efficient environment, only triggering Thai liabilities when you decide to bring funds into the country. This level of control is essential when you're facing top tax rates of 35%. You need a system that works as hard as you did to earn the capital in the first place.

Why i12 investments Matters for Thai Expats

One of the biggest headaches for expats is portfolio rebalancing. If you sell a winning position in a DIY account to buy a lagging one, you might create a reportable gain. The i12 investments framework handles rebalancing at the institutional level. This keeps your risk profile on track without creating a messy trail of transactions for the Thai Revenue Department to scrutinize. It's a cleaner way to grow.

Currency hedging is another critical factor. Most expats manage their lives in Thai Baht but keep their wealth in Singapore Dollars (S$) or US Dollars. The i12 framework allows for sophisticated hedging strategies. You can protect your purchasing power against THB volatility while maintaining your core holdings in a stable currency. It simplifies your reporting because you aren't constantly calculating exchange rate gains on every small trade. This proactive management is vital for maintaining your lifestyle long-term.

Institutional Access vs. Retail Trading

Retail trading platforms often leave the heavy lifting of tax reporting to you. This is a high-risk path in 2026. The i12 investments philosophy provides institutional-grade data that makes audit trails transparent and easy to follow. You avoid common pitfalls like wash sale risks, where selling at a loss to offset gains is disallowed or complicated by cross-border rules. Professional frameworks provide the safety nets that retail accounts lack.

Choosing a managed framework over a DIY platform is about more than just convenience. It's about having a professional roadmap. A financial planner uses these institutional tools to ensure your portfolio aligns with your long-term Thai residency goals. You get the benefit of a modern, rule-based algorithm that removes emotion from the equation, providing a steady hand for your wealth protection needs. It's the standard for the modern professional guide.

Maximizing Double Taxation Agreements (DTAs) and Offshore Platforms

While the 2026 remittance rules are strict, Double Taxation Agreements (DTAs) serve as your primary shield against paying tax twice on the same income. Thailand has treaties with over 60 countries, including Singapore, the UK, and the USA. These agreements ensure that if you've already paid tax on your dividends or interest in your home country, you can often claim a tax credit in Thailand. This is a cornerstone of effective retirement planning for expats in Thailand, as it prevents your global portfolio from being eroded by overlapping jurisdictions.

The choice of where you hold your assets is just as important as the treaty itself. Many expats favor offshore jurisdictions like Jersey or Singapore because they offer high levels of regulatory protection and portability. If your career or retirement takes you from Bangkok to another regional hub, a portable offshore platform ensures your i12 investments framework remains intact. You don't have to sell down your positions and trigger a tax bill just because you've crossed a border.

| Income Source | Singapore DTA | UK DTA | USA DTA |

|---|---|---|---|

| Interest | 10% to 15% cap | 15% cap | 15% cap |

| Dividends | 10% cap | 10% cap | 15% cap |

| Capital Gains | Taxed in resident state | Taxed in resident state | Varies by asset type |

Utilizing the Singapore-Thailand DTA

Zenith Wealth is uniquely positioned to help you leverage the Singapore-Thailand treaty. This agreement is particularly powerful for those holding Singaporean assets, as it often allows for tax-exempt dividends or significantly reduced withholding rates. It's a strategic advantage for expats who maintain financial ties to the Little Red Dot. To see how this works with your existing Singaporean assets, read our guide on Mastering the SRS Account. Coordinating these benefits requires a clear understanding of both Thai remittance rules and Singaporean tax law.

Offshore Platforms: Portability and Compliance

Portability is the single most vital feature for a career expat. Using an offshore platform allows you to consolidate your global holdings into a single, compliant structure. Certain offshore bonds can even defer Thai tax liabilities until you actually remit the funds into your Thai bank account. This forms a core part of our approach to Strategic Investment Management. By keeping your growth within a tax-deferred wrapper, you maintain control over when and how you trigger a tax event. If you're unsure how your specific country's treaty applies to your 2026 filings, reach out to a financial consultant today for a personalized review.

Strategic Wealth Planning with a Professional Financial Consultant

Attempting DIY tax planning in Thailand is a high-risk move in 2026. The shift in remittance rules means that a single misstep in how you transfer your S$ savings could trigger an audit or a 35% tax bill. It's no longer just about choosing the right fund; it's about the technical coordination of your global wealth. A professional financial planner acts as the bridge between your investment strategy and the legal requirements of the Thai Revenue Department. We don't work in a vacuum. We coordinate with legal experts to ensure your remittance trail is documented and compliant before the first dollar crosses the border.

The value of this partnership lies in proactive management. While a lawyer might tell you what the law says, a financial consultant shows you how to structure your portfolio to live within it. By integrating the i12 investments framework, we provide a rule-based approach that removes the guesswork from your monthly withdrawals. This level of precision is the only way to navigate the 2026 landscape with total confidence. It's about protecting what you've built while ensuring you have the liquidity to enjoy your life in the Land of Smiles.

Beyond Tax: Integrating Retirement and Legacy

Tax efficiency is a vital pillar, but it's only one part of a complete strategy. True retirement planning for expats in Thailand must account for your long-term legacy and the protection of your family across borders. Many of our clients maintain deep roots in Singapore, which makes coordinating your Thai lifestyle with your Singaporean assets essential. You need to ensure that your wealth protection strategy covers both your current needs and your future estate.

We invite you to explore our broader resources to see how these pieces fit together. You can dive into The Complete Guide to Retirement Planning for a regional perspective. Additionally, understanding how your assets will pass to the next generation is covered in our guide to Legacy Planning in Singapore. A holistic plan ensures no part of your financial life is left to chance.

Your 2026 Action Plan

Success in this new era requires immediate, decisive action. Don't wait for a tax notice to start organizing your affairs. Follow these steps to secure your position:

- Review your residency status: Start tracking your 183-day count immediately to confirm your tax obligations for the current year.

- Audit your global accounts: Identify which funds are "clean capital" (pre-2024 principal) and which are new 2026 earnings to prevent over-taxation.

- Align your portfolio: Schedule a discovery call to see how i12 investments can streamline your rebalancing and reporting.

Ready to start the conversation? We're here to help you build a roadmap that lasts. Contact us today to book a consultation with a Zenith financial planner. Let's ensure your retirement planning for expats in Thailand is robust, compliant, and ready for whatever 2026 brings.

Secure Your Thai Retirement Future Today

The 2026 tax landscape in Thailand is undeniably complex, but it shouldn't stand in the way of your lifestyle goals. Success now depends on moving beyond simple timing and embracing institutional-grade asset location. By mastering the 183-day residency rule and utilizing the i12 investments framework, you can protect your global portfolio from unnecessary tax events. Effective retirement planning for expats in Thailand is no longer a DIY project; it requires a proactive, compliant roadmap tailored to your unique cross-border needs.

As authorized representatives of finexis advisory Pte Ltd, we bring specialized expertise in cross-border Southeast Asian wealth management. Our team uses the i12 investments framework to provide the rule-based precision your portfolio needs in this new regulatory era. Don't leave your 2026 tax filings to chance. Book a discovery call with a Zenith financial consultant to optimize your Thai tax strategy. We're ready to help you build a secure, tax-efficient plan that lets you focus on enjoying your retirement with total peace of mind.

Frequently Asked Questions

Is foreign-sourced income earned before 2024 still tax-free if remitted in 2026?

Yes, any income earned before January 1, 2024, remains exempt from Thai income tax even if you remit it in 2026. The new tax rules are not retroactive. You must keep clear documentation, such as bank statements or portfolio reports, to prove the timing of these funds. This separation of "clean capital" is a vital part of retirement planning for expats in Thailand to avoid unnecessary tax liabilities.

How does the Thai Revenue Department track money remitted from offshore accounts?

The Thai Revenue Department tracks funds through increased reporting standards and closer cooperation with local and international financial institutions. Banks in Thailand report foreign transfers that meet specific thresholds to the authorities. Additionally, Thailand participates in global data-sharing standards. Keeping a meticulous audit trail of your i12 investments distributions ensures your reporting remains transparent and compliant during any potential review.

Can I use the UK-Thailand Double Taxation Agreement to protect my SIPP?

You can utilize the UK-Thailand Double Taxation Agreement (DTA) to prevent your SIPP distributions from being taxed twice. DTAs generally ensure that pension income is taxed in either the source country or the country of residence, or provide tax credits to offset the bill. You'll need to review the specific "pension" articles within the treaty to determine how to apply these credits to your Thai tax filings.

What is the two-year exemption window for remitting foreign income in 2026?

The two-year exemption window is currently only a proposal and has not been formally enacted into law as of July 2026. If passed, it would exempt foreign income earned from 2024 onwards if remitted within the same year or the following calendar year. Since this requires further Cabinet approval, it's safer to base your current strategy on the confirmed remittance rules rather than this pending proposal.

Do I need to file a tax return in Thailand if I remit no money?

You generally aren't required to file a Thai tax return if you have no assessable income and remit no foreign funds into the country. However, being a tax resident for 180 days or more might still trigger certain reporting expectations depending on your visa type. It's best to confirm your status with a professional to ensure you don't face complications with your residency or future visa extensions.

How can a financial consultant help me navigate the new Thai tax laws?

A financial consultant helps you build a technical structure for your global wealth that aligns with the 2026 rules. They implement frameworks like i12 investments to manage asset location and minimize unnecessary tax events. By coordinating with legal experts, a financial planner ensures your audit trail is robust. This proactive approach protects your capital and provides the documentation needed for compliant fund remittance.

Are LTR visa holders exempt from the new remittance tax rules in 2026?

Yes, the Long-Term Resident (LTR) visa program provides specific tax exemptions on foreign-sourced income for certain categories, including wealthy pensioners. This makes the LTR visa a highly effective tool for tax-efficient retirement planning for expats in Thailand. If you hold this visa, you can typically remit your global investment gains without being subject to the standard progressive personal income tax brackets.

Is my initial investment principal taxable when brought into Thailand?

Your initial investment principal is not taxable because it is not classified as assessable income. Only the growth, interest, or dividends earned on that capital face taxation upon remittance. The burden of proof rests on you to distinguish between your original savings and your accumulated profits. If you can't provide clear records, the Revenue Department may default to taxing the entire amount you bring into the country.