Most Singaporeans are effectively giving away thousands in potential savings by letting their SRS funds sit idle. You likely already know that srs tax relief is a powerful tool to lower your chargeable income. Still, the S$80,000 total relief cap often makes the process feel confusing. It's frustrating to see your contributions earning a tiny 0.05% interest while you're trying to build a real retirement nest egg.

We're here to help you change that. This guide shows you how to use the Supplementary Retirement Scheme to slash your YA 2027 tax bill. You'll also learn to secure higher returns than a standard bank account. You'll discover how the shift to a statutory retirement age of 64 on July 1, 2026, impacts your long term planning. We've mapped out everything from the S$15,300 contribution limit for citizens to the S$35,700 cap for foreigners. Let's build a smarter, more tax-efficient future together. Drop us a line to get started!

Key Takeaways

- Master the dollar-for-dollar mechanism to reduce your chargeable income and lower your YA 2027 tax bill.

- Calculate your exact savings using the 2026 tax brackets while staying within the S$80,000 total relief cap.

- Claim your srs tax relief before the July 2026 deadline to lock in a lower statutory retirement age for future withdrawals.

- Stop the "idle cash" trap by shifting funds from 0.05% bank rates into T-Bills, REITs, or blue-chip stocks.

- Learn how to integrate your SRS contributions into a comprehensive legacy and estate plan for long-term wealth protection.

What is SRS Tax Relief and How Does it Benefit You in 2026?

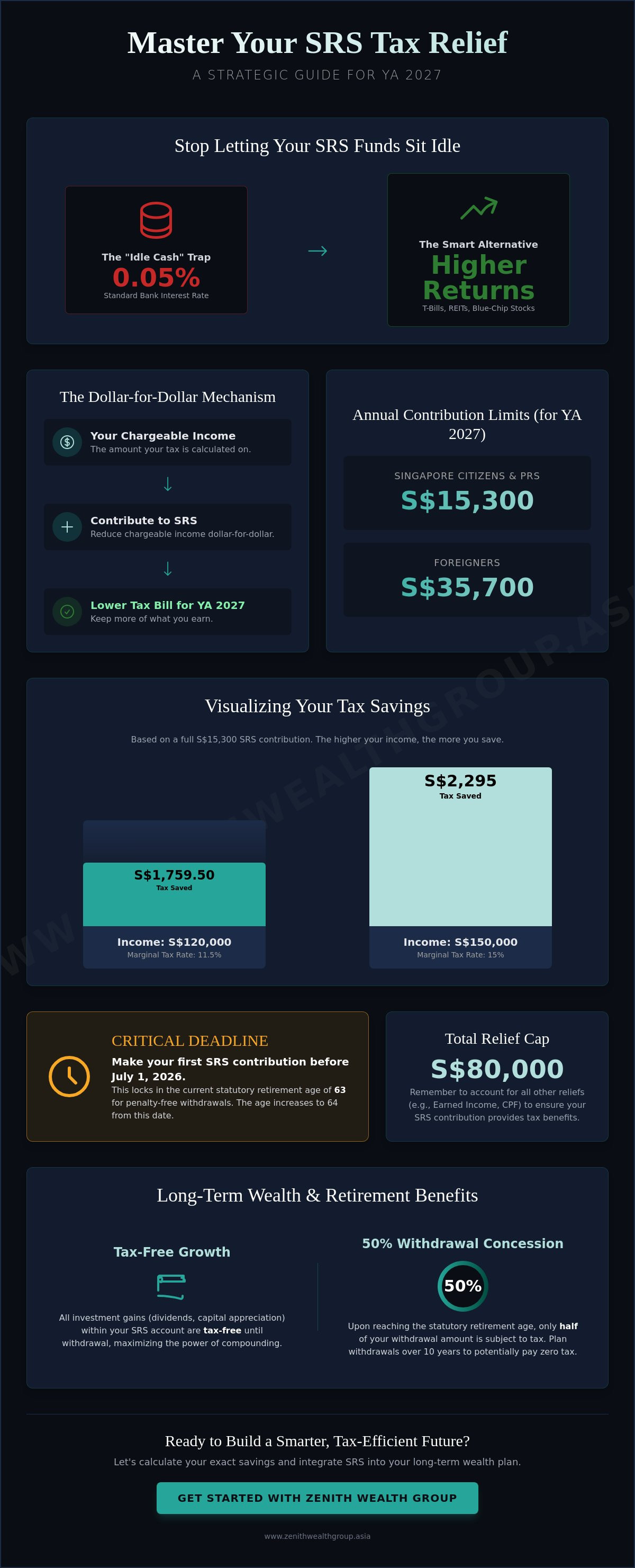

The Supplementary Retirement Scheme (SRS) isn't just another bank account. It's a voluntary pillar of your financial strategy that complements the Central Provident Fund (CPF). While CPF is mandatory, the SRS gives you the flexibility to decide how much you want to save and how to invest it. The biggest draw is the immediate srs tax relief. For every dollar you contribute, the government reduces your chargeable income by the same amount. It's a straightforward, dollar-for-dollar reduction that puts money back in your pocket during the next tax season.

Beyond the initial savings, your money works harder inside the SRS. Any investment gains you earn, whether from dividends or capital appreciation, are tax-free until you withdraw them. This creates a powerful compounding effect that isn't possible in a standard taxable brokerage account. When you finally reach the statutory retirement age, you'll enjoy a 50% tax concession. This means only half of your total withdrawal amount is subject to tax. If you manage your withdrawals over the 10-year period, you might end up paying zero tax on your retirement income.

Eligibility and Contribution Limits for 2026

Opening an SRS account is simple for any Singapore Citizen, Permanent Resident (PR), or foreigner earning income here. For 2026, the contribution caps remain steady. Singapore Citizens and PRs can contribute up to S$15,300 annually. Foreigners have a higher cap of S$35,700 to account for the lack of mandatory CPF benefits. You must make these contributions by December 31, 2025, to qualify for relief in the Year of Assessment 2026. Contributions made throughout the 2026 calendar year will apply to your YA 2027 tax bill. Don't wait until the last minute; bank systems often get congested on New Year's Eve.

The Long-Term Value of Compounded Tax Savings

Think of your tax refund as a bonus for your future self. If you're in the 15% tax bracket and contribute S$15,300, you save S$2,295 in taxes. Reinvesting that S$2,295 every year can shave years off your working life. It's a core part of effective retirement planning singapore. By integrating these savings into a broader strategy, you aren't just saving money; you're building a legacy. Drop us a line if you're ready to see how these numbers look for your specific income level!

Step-by-Step: How to Calculate Your SRS Tax Savings

Calculating your srs tax relief isn't just about plugging numbers into a spreadsheet. It's about understanding how the Singapore tax system layers your income. To start, find your total assessable income. This is your gross pay minus your employee CPF contributions. For the Year of Assessment 2026, you'll be looking at your 2025 earnings. Once you have that number, check the IRAS tax brackets to see how much of your income falls into your highest tax tier. Contributions to your account are eligible for tax relief on a dollar-for-dollar basis, effectively reducing your chargeable income.

Your marginal tax rate is the specific tax percentage applied to the very last dollar you earn. If you earn S$125,000, your last S$5,000 is taxed at 15%. By contributing S$15,300 to your SRS account, you wipe out that S$5,000 at 15% and another S$10,300 at the 11.5% bracket. This strategy moves your taxable income into a lower tier, resulting in immediate cash savings. It's a simple way to keep more of what you earn without changing your lifestyle.

Using the Tax Bracket Method

Let's look at two scenarios to visualize the impact. A professional earning S$120,000 sits at the top of the 11.5% bracket. A full S$15,300 SRS contribution saves them roughly S$1,759.50 in taxes. Now, consider someone earning S$150,000. Their top income tier is taxed at 15%. For them, the same S$15,300 contribution results in a S$2,295 reduction in their tax bill. The higher your income, the more valuable every dollar of srs tax relief becomes. You're essentially choosing to pay your future self instead of the tax office.

Factoring in Other Tax Reliefs

Singapore has a hard ceiling on personal tax relief. Total reliefs, including SRS, Earned Income Relief, and Spouse Relief, are capped at S$80,000 per year. If you're a working mother with multiple children or you're already claiming significant relief for life insurance and parent maintenance, you might hit this cap sooner than you think. Adding SRS funds beyond this S$80,000 limit won't give you extra tax savings. It's vital to tally your existing reliefs before making your contribution. If you're unsure where your total stands, feel free to reach out for a quick check on your tax roadmap.

Strategic SRS Planning: Avoiding Common Pitfalls

Many Singaporeans think the job is done once the money hits the account. It isn't. If you leave your funds as cash, you're earning a measly 0.05% per year. Inflation will eat your savings before you even reach retirement. You must actively invest those funds to make the srs tax relief truly worth it. Another critical factor is the date of your first contribution. From July 1, 2026, the statutory retirement age rises from 63 to 64. Making your first contribution before this date locks in the age of 63 for penalty-free withdrawals. This single decision gives you earlier access to your money. It's a small move that pays off a year sooner.

Once you reach that age, you have a 10-year window to withdraw your funds. Only 50% of these withdrawals are taxable. If you have no other income, you can withdraw up to S$40,000 annually without paying a cent in tax. This requires careful planning. Taking it all at once could push you into a high tax bracket, defeating the purpose of the scheme. Spread your withdrawals to keep your taxable income low. It's about playing the long game with your savings.

The S$80,000 Tax Relief Cap Trap

Singapore imposes a strict S$80,000 limit on total personal tax reliefs. This includes SRS, CPF top-ups, and life insurance reliefs. If you've already hit this cap through other schemes, your SRS contribution won't lower your tax bill. It's just locked-up cash with no immediate benefit. Check the official SRS tax relief guidelines to see where you stand. High-income earners should prioritize SRS over CPF cash top-ups if they want more investment flexibility. CPF funds are restricted, but SRS funds can be moved into various assets. Don't waste your contribution limit on accounts that don't serve your growth goals.

Early Withdrawal Risks and Penalties

Life happens, but tapping into your SRS account early is expensive. You'll face a 5% penalty on the withdrawn amount. Worse, 100% of that withdrawal becomes taxable in the year you take it. This could result in a massive tax bill if you're still in a high income bracket. Exceptions only apply for specific medical grounds or terminal illness. This is why having a separate emergency fund is vital. Proper wealth protection ensures you never have to touch your retirement nest egg prematurely. Keep your retirement funds for retirement. Drop us a line if you're unsure how to balance your liquidity needs!

How to Invest Your SRS Funds for Maximum Growth

Securing your srs tax relief is only the first half of the battle. The real magic happens when you move those funds out of the 0.05% interest "idle cash" trap. Over a 20-year horizon, even a modest 3% inflation rate can slash your purchasing power by nearly 45%. To combat this, you need a portfolio that outpaces the cost of living. Many investors start with low-risk Singapore Government Securities (SGS) or T-Bills. These offer significantly better yields than a standard savings account while maintaining high security. They're excellent for the portion of your portfolio you can't afford to lose.

For those with a longer runway, blue-chip stocks and Real Estate Investment Trusts (REITs) on the SGX provide a mix of capital growth and steady dividends. Since dividends earned within the SRS are tax-free, reinvesting them accelerates your wealth accumulation. You might also consider unit trusts or insurance-linked products to add a layer of professional management and stability. These vehicles allow you to diversify across global markets without the stress of picking individual stocks. Your goal is to build a robust engine that turns your tax savings into a substantial retirement nest egg.

SRS Strategies for Expats and Foreigners

Foreigners face unique rules but enjoy massive benefits. If you aren't a Singapore Citizen or PR, you can withdraw your SRS funds entirely tax-free after a 10-year holding period. This 10-year clock starts from the date of your first contribution. It's a powerful "clean break" strategy for those planning to leave Singapore eventually. However, you must manage currency risk carefully. Since your investments are likely in SGD, consider how they'll convert to your home currency later. We can help you design a currency-neutral strategy that protects your global mobility.

Balancing Risk and Return

Your investment choice should mirror your proximity to retirement. If you're in your 30s, you can afford higher exposure to equities to capture growth. As you approach the statutory retirement age, shifting toward fixed income protects your gains. Staying invested over several market cycles allows your SRS portfolio to recover from short-term volatility while capturing the long-term upward trajectory of global markets. Don't let fear keep your money in cash. If you're ready to put your tax savings to work, reach out to our guides today!

Optimising Your Total Tax Strategy with Zenith Wealth

Securing your srs tax relief is a great first step, but it shouldn't be your last. True financial clarity comes from looking beyond a single scheme. Our Modern Professional Guides at Zenith Wealth focus on your entire financial ecosystem. We don't just look at how much you save this year; we look at how those savings impact your life ten or twenty years down the road. For high-net-worth individuals, tax efficiency requires a personalized analysis that accounts for multiple income streams and complex relief caps. We strip away the heavy financial jargon to make your retirement path easy to understand and even easier to follow.

Your SRS account is a powerful tool for legacy and estate planning. It isn't just a bucket for tax savings; it's a strategic asset. By integrating your srs tax relief contributions into a broader wealth protection plan, you ensure your family's future is secure. We help you map out how these funds will eventually be distributed or utilized, minimizing the tax burden on your beneficiaries. This proactive approach turns a simple tax break into a cornerstone of your family's financial legacy. It's about building a plan that grows alongside you.

Why Independent Advice Matters

Most people open an SRS account at their primary bank. This often limits your investment choices to what that specific bank offers. As an authorized representative of finexis advisory, we provide a different perspective. We aren't tied to a single institution. This independence gives you access to a significantly wider range of investment products across the market. Whether you're looking for specific unit trusts or specialized insurance-linked products, we find the right fit for your risk profile. You deserve options that align with your goals, not just a bank's sales targets.

Take the Next Step Toward Tax Efficiency

The rules for the 2026 Year of Assessment are already in motion. Don't wait until December to figure out your tax position. We invite you to join us for a discovery session to review your current strategy. We'll look at your income, your current reliefs, and identify gaps where you could be saving more. It's a simple, human-centric conversation designed to give you peace of mind. Your retirement nest egg deserves more than a "set and forget" attitude. Drop us a line to optimize your SRS strategy! Let's build your peak financial future together.

Take Charge of Your 2026 Tax Roadmap

Maximizing your srs tax relief is a timing game that requires more than just a simple bank transfer. You've seen how contributing before July 1, 2026, secures an earlier retirement age of 63 for your future withdrawals. You also know how a 10-year withdrawal window can effectively eliminate taxes on up to S$400,000 of retirement income. These aren't just numbers; they're the building blocks of your financial freedom.

At Zenith Wealth Group, we specialize in Singapore retirement and tax planning. As authorized representatives of finexis advisory, we provide modern, jargon-free professional guidance. We help you navigate the S$80,000 aggregate relief cap and identify investments that outpace the standard 0.05% bank rate. Don't let your tax savings sit idle when they could be building a robust legacy. It's time to move from passive saving to active wealth creation.

Secure your retirement and lower your taxes; contact Zenith Wealth Group today. Your future self will thank you for the clarity you find today. Drop us a line to get started!

Frequently Asked Questions

Is srs tax relief worth it for low-income earners?

The benefits are minimal if your annual chargeable income is below S$40,000. Since the first S$20,000 is tax-free and the next S$10,000 is taxed at only 2%, your actual savings won't outweigh the liquidity lock-in. You're better off keeping your cash flexible or maximizing your CPF interest rates. High-income earners in the 15% bracket or above see the most significant impact from srs tax relief.

Can I use my SRS funds to buy a property in Singapore?

No, you cannot use SRS funds for real estate. Unlike your CPF Ordinary Account, SRS funds are strictly for retirement and cannot be used for property down payments or mortgage installments. These funds must remain in your account or be placed in approved investment products. If you need liquidity for a home purchase, keep those funds in a high-yield savings account instead.

What is the maximum amount I can save in taxes with SRS in 2026?

Your maximum savings depend on your marginal tax rate and residency status. A Singapore Citizen in the top 24% tax bracket can save S$3,672 by contributing the full S$15,300. A foreigner in that same bracket can save up to S$8,568 due to their higher S$35,700 contribution limit. Always check if these contributions keep you under the S$80,000 total personal relief cap.

What happens to my SRS account if I leave Singapore permanently?

Foreigners and PRs can withdraw funds penalty-free after holding the account for at least 10 years. Only 50% of the withdrawn amount will be subject to tax at that time. If you withdraw before the 10-year mark, you'll face a 5% penalty and 100% of the sum becomes taxable. This makes the 10-year holding period a vital part of your exit strategy.

Can I have more than one SRS account to get more tax relief?

No, you are legally allowed only one SRS account at any time. You can choose to open it with DBS, OCBC, or UOB. Attempting to open a second account is a violation of IRAS regulations and won't increase your srs tax relief limits. You can, however, transfer your existing account between these three banks if you find better investment options elsewhere.

How do I claim srs tax relief on my income tax return?

The process is entirely automatic. Your SRS operator bank reports your contribution details directly to IRAS at the end of every year. You don't need to file any receipts or manual claims. You'll see the relief reflected in your tax portal when you check your assessment for the Year of Assessment 2027. This ensures a seamless experience for every contributor.

When is the best time of year to contribute to my SRS account?

Contributing early in the year is the smartest move. This gives your investments more time to grow tax-free within the account. Most Singaporeans wait until the December 31st deadline, but this often leads to rushed investment decisions. Start your contributions in January or February to maximize your "time in the market" and avoid the year-end bank system congestion.

What are the best investment options for SRS funds in 2026?

Avoid leaving your funds as cash, as it earns a negligible 0.05% interest. For 2026, Singapore Government Securities and T-Bills offer a safe way to beat inflation. If you have a longer timeline, blue-chip REITs or diversified unit trusts provide better growth potential. Matching your asset choice to your expected retirement age is the key to building a robust and sustainable nest egg.