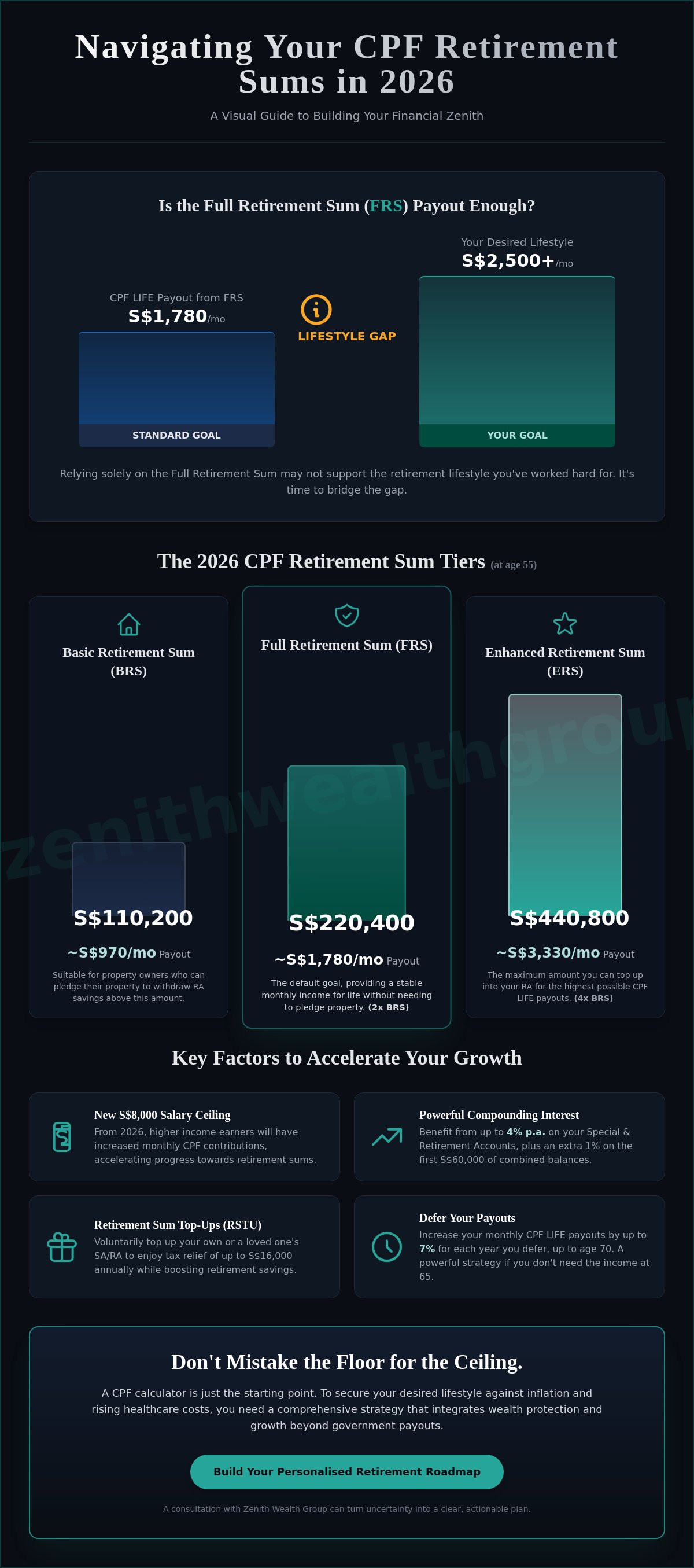

What if your retirement goal isn't just a number, but a lifestyle that your current CPF trajectory can't quite reach? Many Singaporeans assume hitting the Full Retirement Sum of S$220,400 in 2026 is the finish line. However, that only secures a monthly payout of about S$1,780. If you're aiming for S$2,500 or more, relying solely on a cpf retirement sum calculator might reveal a gap you weren't expecting.

It's understandable to feel uneasy about the steady 3.5% annual increase in retirement sums or the jump in the salary ceiling to S$8,000. You've worked hard. You deserve a plan that offers more than just the bare minimum. We're here to help you turn that uncertainty into a clear, actionable roadmap that prioritizes your comfort.

This guide breaks down the 2026 retirement tiers, from the BRS of S$110,200 to the new ERS of S$440,800. You'll learn how to optimize your Ordinary and Special Accounts while building a strategy to supplement your CPF LIFE payouts. Let's move beyond the government floor and start building your retirement ceiling together.

Key Takeaways

- Identify the 2026 retirement sum benchmarks, including the S$220,400 Full Retirement Sum, to establish your baseline for lifelong income.

- Use a cpf retirement sum calculator to project your future payouts by factoring in the latest salary ceiling increase to S$8,000.

- Compare the BRS, FRS, and ERS tiers to select a target that matches your housing status and monthly spending needs.

- Explore topping-up strategies like the RSTU scheme to maximize your tax relief while growing your retirement nest egg effectively.

- Go beyond basic government payouts by integrating professional wealth protection to ensure your lifestyle remains secure against rising healthcare costs.

Navigating the 2026 CPF Retirement Sum Landscape

When you turn 55, your financial journey hits a significant milestone. The CPF Board automatically creates your Retirement Account (RA), which serves as the engine for your future monthly payouts. This account is funded by transferring savings from your Special Account and Ordinary Account. Understanding how the Central Provident Fund (CPF) system structures these sums is vital if you're reaching this age in 2026. The goal isn't just to meet a regulatory requirement, but to ensure your golden years are funded with precision.

The annual 3.5% increment in retirement sums is a deliberate move to keep pace with the rising cost of living in Singapore. It ensures that the purchasing power of your payouts doesn't erode over time. If you're turning 55 in 2026, these figures are no longer abstract projections; they're the concrete benchmarks you need to plan around. Using a cpf retirement sum calculator helps you see where you stand, but you need to know what those numbers actually mean for your daily life.

Projected 2026 Retirement Sum Benchmarks

For the 2026 cohort, the benchmarks have been clearly defined. The Basic Retirement Sum (BRS) is set at S$110,200. This tier is generally for those who own a property and are willing to pledge it to meet their retirement needs. The Full Retirement Sum (FRS) stands at S$220,400, which is double the BRS. This is the default target for most Singaporeans who want a stable, mid-range payout without relying on property equity.

The most significant shift involves the Enhanced Retirement Sum (ERS). Starting from 2025, the ERS cap was raised to four times the BRS. In 2026, this brings the ERS to S$440,800. This change allows you to voluntarily commit more to your RA to secure much higher monthly payouts, which is a powerful tool for those aiming for a more affluent lifestyle.

Why a Calculator is Only the Starting Point

A cpf retirement sum calculator is excellent for providing a snapshot of your trajectory, but it has limitations. It often focuses on the "estimated payout" in today's dollars without fully accounting for your specific inflation concerns or changing lifestyle needs. For instance, a payout of S$1,780 from the FRS might feel sufficient now, but will it cover your desired travel or healthcare preferences in fifteen years?

Many calculators also overlook the nuances of property pledges. If you choose the BRS, you're essentially betting on your property's value to bridge the gap, which requires a more complex strategy than a simple online tool can provide. Don't fall into the psychological trap of "hitting the FRS" and stopping your retirement efforts. Treating the government minimum as your maximum potential is a common mistake. If you want a plan that goes beyond the basics, reach out to us for a personalized advisory session.

How to Use a CPF Retirement Sum Calculator for Accurate Projections

Getting an accurate retirement projection requires more than just plugging in a single number. A cpf retirement sum calculator is a powerful tool, but its output depends entirely on the quality of your inputs. Start by gathering your latest Ordinary Account (OA) and Special Account (SA) balances from the CPF portal. Remember that your SA and RA funds currently benefit from a 4% floor interest rate, while your OA earns 2.5%. These rates are confirmed through March 2026, and they form the bedrock of your compounding growth.

You also need to account for the 2026 salary ceiling increase to S$8,000. This change means higher monthly contributions if your income sits above the previous caps. These extra funds can significantly accelerate your progress toward the Full Retirement Sum. Finally, decide on your payout start age. While you can begin receiving money at 65, deferring your payouts until age 70 can increase your monthly income by about 7% for every year you wait. If these variables feel overwhelming, speak with a consultant to refine your numbers.

Step-by-Step Input Guide

- Step 1: Determine your timeline. Calculate exactly how many years you have left until age 55 and age 65 to understand your contribution window.

- Step 2: Project your account growth. Factor in the 4% interest on your SA and the 2.5% on your OA. Don't forget to include the extra 1% interest on the first S$60,000 of your combined balances.

- Step 3: Benchmark your results. Compare your projected RA balance against the 2026 targets: S$110,200 for BRS, S$220,400 for FRS, or S$440,800 for ERS.

- Step 4: Select your CPF LIFE plan. Choose between the Standard Plan for steady payouts, the Escalating Plan to hedge against inflation, or the Basic Plan if you wish to leave a larger legacy.

Common Calculator Pitfalls to Avoid

Many users overestimate their future payouts by ignoring the impact of housing withdrawals. If you've used your OA to pay for your property, that principal and the accrued interest you "owe" yourself will reduce the amount available for your RA. It's a common gap that simple tools often miss.

Another critical factor is the 2025 closure of the Special Account for members aged 55 and above. From that point forward, only your RA and OA will exist. Any funds in excess of your Full Retirement Sum will reside in your OA, earning 2.5% instead of 4%. This shift can lower your overall interest yield, so ensure your cpf retirement sum calculator accounts for this new reality to avoid an unpleasant surprise at 65.

Comparing BRS, FRS, and ERS: Choosing Your Retirement Payout Goal

Your choice of retirement sum determines your quality of life for decades. While a cpf retirement sum calculator provides the math, you need to provide the vision. The three tiers, Basic, Full, and Enhanced, aren't just regulatory hurdles. They're different levels of financial freedom. Deciding which one to aim for depends on your housing situation and your expected monthly expenses.

The Basic Retirement Sum (BRS) of S$110,200 is designed for those who own their home and are comfortable with a property charge. It yields about S$950 a month for those turning 55 in 2026. This is a subsistence level. It covers essentials like hawker meals and basic utilities, but leaves little room for leisure. If you have significant private savings or a rental income stream, the BRS might suffice as a secondary floor.

Most Singaporeans target the Full Retirement Sum (FRS) of S$220,400. It's the "safety net" that provides roughly S$1,780 monthly. This supports a more typical middle-income lifestyle. It allows for occasional restaurant visits and local travel without constant stress. However, if you're used to a higher standard of living, you'll likely find this amount restrictive.

The Lifestyle Match: Payouts vs. Reality

Payouts are only useful if they match your reality. A S$950 monthly payout from the BRS covers basic survival. It's the "room and board" tier. Moving up to the FRS provides a comfortable baseline, but it's rarely enough to replace a professional salary. For many, the Enhanced Retirement Sum (ERS) is the only tier that feels like a true retirement. With a projected payout of S$3,440, the ERS starts to look like a sustainable replacement for a working wage. It's built for those who want to maintain their hobbies and social lives without compromise.

The 2026 ERS Expansion: A New Opportunity

The recent policy shift to set the ERS at four times the BRS is a game-changer. In 2026, this allows you to top up your RA to S$440,800. This is an incredible opportunity for high-earners. It offers a risk-free 4% return that is backed by the government. Very few private annuity options can match the cost-efficiency and reliability of CPF LIFE at this scale. Even if you have a robust investment portfolio, the ERS serves as a powerful, non-correlated asset. It guarantees income as long as you live. It's the ultimate hedge against outliving your capital. If you aren't sure how to balance these top-ups with your other investments, it's worth exploring how this fits into your broader portfolio.

Closing the Retirement Gap: Strategies When Your CPF Savings Fall Short

Identifying a shortfall in your retirement funds can be a sobering moment. If the cpf retirement sum calculator shows a projected monthly payout that doesn't align with your lifestyle goals, you aren't alone. This "retirement gap" is common, especially as the 2026 benchmarks for the Full Retirement Sum reach S$220,400. Fortunately, you have several levers to pull. The Retirement Sum Topping-Up (RSTU) scheme is a primary tool. It allows you to make cash top-ups to your RA for tax relief of up to S$8,000 per year for yourself and another S$8,000 for loved ones.

Another indirect method is making Voluntary Contributions (VC) to your Medisave Account. Since your Medisave has a cap, specifically the S$79,000 Basic Healthcare Sum for 2026, any excess funds often flow into your Special or Retirement Account. Don't forget the Supplementary Retirement Scheme (SRS). It offers a dollar-for-dollar tax deduction and allows for private investment growth, serving as a flexible third pillar alongside your CPF. These tools help you build a more robust floor for your future.

Cash Top-ups vs. Investment Growth

Deciding where to put your next S$1,000 is a strategic choice. While CPF offers a guaranteed 4% in the RA, those funds are effectively locked away. Private wealth accumulation offers liquidity that CPF doesn't. If you need funds for an emergency or a child's education before 65, locking everything in CPF might be a mistake. You can use a Retirement Planning Calculator to simulate how different monthly contributions to private portfolios might impact your long-term wealth compared to CPF top-ups. Balancing safety with accessibility is key to a stress-free plan.

Property Pledging: Unlocking Cash Without Selling

If you're short on cash but own your home, property pledging is a viable alternative. By pledging your property, you can opt for the Basic Retirement Sum of S$110,200 instead of the Full Retirement Sum. This frees up cash for immediate needs, but it comes with a trade-off. Your monthly payouts will be lower, roughly S$950 instead of S$1,780. Additionally, the pledge must be repaid with accrued interest upon the sale of the property. For legacy planning, this means your beneficiaries might receive a smaller inheritance from the home sale. It's a complex decision that requires a look at your entire estate. If you're struggling to choose between these paths, book a strategy session to find the right balance for your family.

Optimizing Your Payouts with Zenith Wealth’s Strategic Advisory

A cpf retirement sum calculator provides a helpful starting point, but it shouldn't be your final destination. It calculates a baseline. It doesn't build a life. It certainly doesn't account for your specific aspirations or the risks that could derail your plans. At Zenith Wealth, we help you move beyond generic numbers to create a personalized financial roadmap. This journey involves more than just hitting the Full Retirement Sum of S$220,400. It's about ensuring every dollar works toward your specific vision of freedom.

One critical piece often missing from basic tools is Wealth Protection. A sudden medical shock can deplete your savings faster than any payout can replenish them. We integrate robust protection strategies to safeguard your future against rising healthcare costs. By balancing your CPF LIFE payouts with private annuities and global investments, we build a resilient portfolio. This multi-layered approach ensures you aren't over-reliant on a single government scheme. Professional oversight is vital as we navigate the 2026 regulatory shifts, including the Special Account closure for those 55 and above.

The Zenith Advantage: Holistic Retirement Planning

Our advisory services provide a customized cash flow analysis that simple government tools can't replicate. We look at your lifestyle today and project it into the future, accounting for your unique inflation concerns. We also dive deep into tax efficiency. By optimizing your SRS contributions and timing your CPF top-ups, we help you maximize your take-home retirement income. Legacy planning is another pillar of our approach. We ensure your CPF nominations and private assets align perfectly, so your wealth is distributed exactly as you wish without unnecessary legal friction.

Start Your 2026 Retirement Audit

Preparing for the 2026 regulatory landscape requires proactive steps. During a consultation, we perform a deep dive into your current CPF balances and existing investment portfolio. We'll examine the impact of the increased S$8,000 salary ceiling and the shifting retirement ages on your specific timeline. You'll walk away with actionable takeaways and a clear "Yes/No" on whether to proceed with specific top-ups or investment shifts. Don't leave your golden years to chance. Secure your retirement future with a personalized audit at Zenith Wealth today. Let's start a conversation about your legacy.

Secure Your Future Beyond the Numbers

Planning for 2026 requires more than just meeting the government's benchmarks. You've seen how the different retirement tiers impact your daily life and why a simple cpf retirement sum calculator can only tell half the story. True retirement readiness comes from bridging the gap between those government minimums and the lifestyle you've worked hard to build. It's about making your money work as hard as you do while ensuring your legacy is protected for the next generation.

At Zenith Wealth Group, we don't just look at accounts; we look at your life. As authorized representatives of finexis advisory, we specialize in navigating Singapore's unique retirement landscape. Our holistic approach covers everything from your CPF and SRS to private wealth and protection strategies. We're ready to help you turn these complex regulations into a clear, confident path forward. We'll help you decide exactly when to top up, when to invest, and how to safeguard what you've built.

Ready to see the full picture? Book a Comprehensive CPF & Retirement Audit with Zenith Wealth Group today. Let's start a conversation about your goals and build a plan that's as unique as you are. Your future is waiting!

Frequently Asked Questions

What is the projected CPF Full Retirement Sum (FRS) for 2026?

The Full Retirement Sum for members turning 55 in 2026 is S$220,400. This figure is part of a planned 3.5% annual increase designed to help your retirement savings keep pace with inflation and the rising cost of living. Knowing this specific target allows you to use a cpf retirement sum calculator with much greater accuracy for your long term projections.

Can I use my CPF Ordinary Account to top up my Retirement Account to the ERS?

Yes, you can transfer savings from your Ordinary Account (OA) to your Retirement Account (RA) to reach the Enhanced Retirement Sum (ERS). For the 2026 cohort, the ERS cap is S$440,800. This strategy is popular because it moves your funds from the 2.5% OA interest rate to the 4% RA interest rate, effectively boosting your lifelong monthly payouts.

How does the 2025 closure of the Special Account for those 55+ affect my 2026 planning?

From 2025, the Special Account (SA) closes for everyone aged 55 and above. Your SA savings will automatically transfer to your RA up to the Full Retirement Sum. Any remaining SA balance moves to your OA. This change means excess funds will earn the OA interest rate of 2.5% instead of the 4% SA rate, so you may need to adjust your investment strategy to cover the 1.5% yield gap.

Is it better to top up my CPF RA or invest in the Supplementary Retirement Scheme (SRS)?

The choice depends on whether you prioritize guaranteed returns or investment flexibility. Topping up your RA provides a risk free 4% return and higher CPF LIFE payouts for life. The SRS offers a dollar for dollar tax deduction and lets you invest in a wider range of global assets. Many retirees use both to balance a secure income floor with the potential for higher market growth.

What happens to my CPF Retirement Sum if I continue working after age 65?

Your CPF contributions from work will continue to flow into your accounts even after you reach the payout eligibility age. You can choose to start your payouts at 65 or defer them until any age up to 70. Deferring is a powerful move. Your monthly payouts increase by about 7% for every year you wait, providing a much larger monthly check if you don't need the cash immediately.

Can I withdraw my CPF savings in 2026 if I have already met the Full Retirement Sum?

You can withdraw any amount in excess of your Full Retirement Sum starting from age 55. If you own a property with a remaining lease that lasts until you are at least 95, you can also choose to meet the Basic Retirement Sum of S$110,200 and withdraw the rest. These withdrawals provide the liquidity needed for immediate post retirement goals or debt repayment.

How does property pledging work if I only want to hit the Basic Retirement Sum?

Property pledging allows you to use your home's value to meet the difference between the BRS and the FRS. By pledging your property, you lower the cash requirement in your RA to S$110,200 for the 2026 cohort. This frees up more cash for withdrawal at 55. However, you must repay the pledged amount plus accrued interest from the sales proceeds if you sell the property in the future.

What is the difference between the CPF LIFE Standard and Escalating plans?

The Standard Plan offers a level, steady payout for life, while the Escalating Plan starts about 20% lower but increases by 2% every year. The Escalating Plan is specifically designed to protect your purchasing power against inflation over time. A cpf retirement sum calculator can help you compare how these two paths will affect your monthly cash flow as you reach your 80s and 90s.