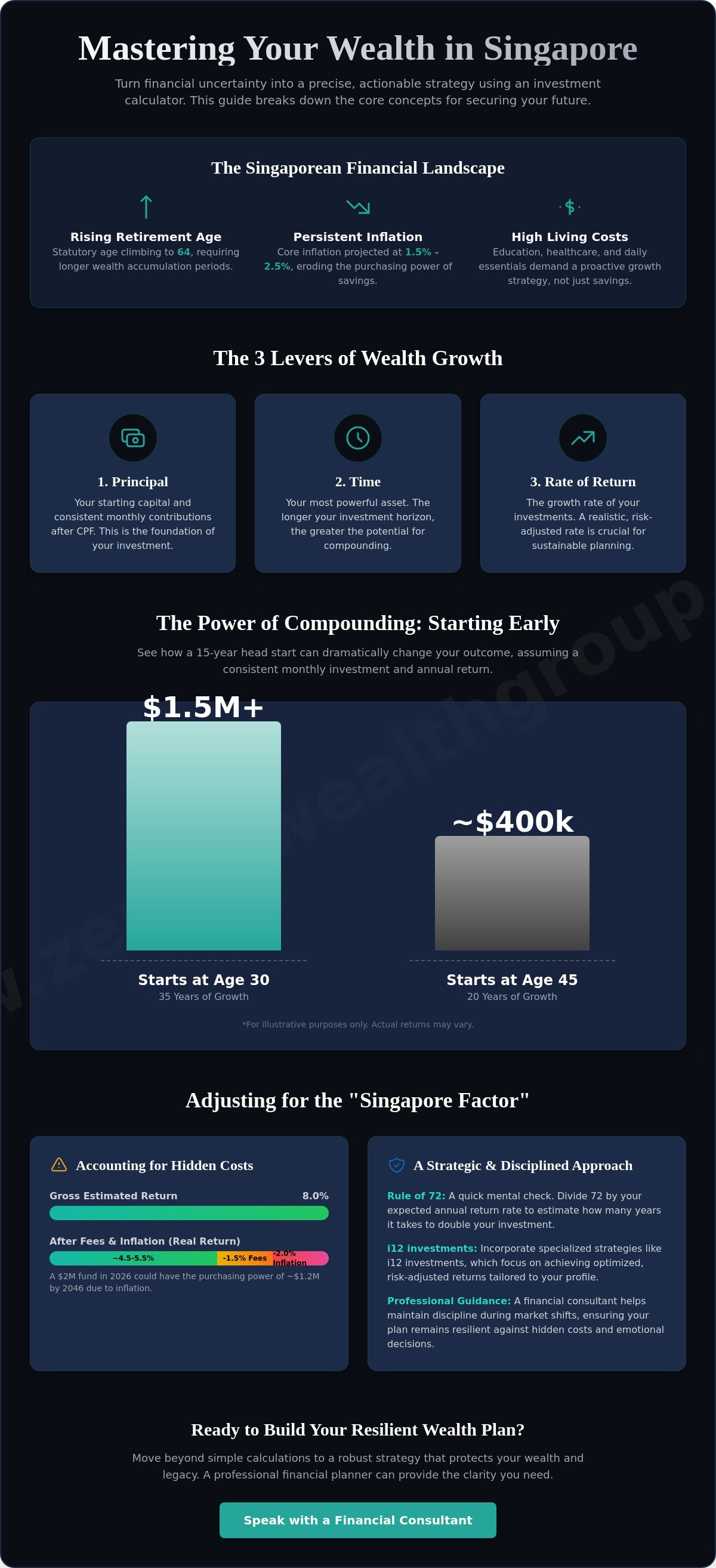

What if the "safe" savings target you have been aiming for is actually leaving you short as Singapore’s statutory retirement age climbs to 64 this July? Mastering an investment calculator singapore is the first step toward answering that question with certainty. It is natural to feel the pressure of rising costs, from daily essentials to tuition fees at institutions like the Singapore American School. You might worry if your current portfolio can truly go the distance or if inflation, currently projected to average between 1.5% and 2.5%, will erode your hard-earned wealth.

We are here to help you trade that uncertainty for a concrete plan. This article will teach you how to use these digital tools to project your wealth over 20 years and determine the exact monthly contribution required to meet your goals. We will also look at how to evaluate the impact of i12 investments within your broader strategy. You will gain the same clarity a professional financial planner uses to ensure your education funding and retirement plans remain resilient, no matter how the market shifts.

Key Takeaways

- Turn financial guesswork into a precise monthly target using an investment calculator singapore.

- Learn to balance high-cost education funding with your personal retirement strategy.

- Identify common pitfalls in linear growth models and adjust for Singapore's specific inflation rates.

- Discover how a financial planner and i12 investments help maintain discipline during market shifts.

- Move beyond simple calculations toward robust wealth protection and legacy planning.

What is an Investment Calculator and Why Do You Need One in Singapore?

An investment calculator is more than just a digital tool. It’s a mathematical engine designed to model the future of your wealth. Think of it as a bridge between your current bank balance and your long-term aspirations. By using an Financial calculator, you move away from the anxiety of "hoping" you have enough for the future. Instead, you gain the confidence of "knowing" your exact financial trajectory. This clarity is essential for anyone living in Singapore, where the cost of living and high-tier education expenses require precise planning.

Singaporeans face a unique set of financial pressures. We deal with specific inflation rates, currently projected to stay between 1.5% and 2.5%, alongside rising healthcare costs. A simple savings calculator only shows you what you've put away; it doesn't account for the growth needed to outpace these rising costs. A strategic investment calculator singapore allows you to visualize how your portfolio, including specialized options like i12 investments, can grow over time. It transforms abstract numbers into a concrete roadmap for your family’s security.

The Core Variables: Principal, Time, and Rate

To get the most out of your projections, you must understand the three levers that drive growth. Your "Principal" is your starting point. In a local context, this isn't just your savings account. It includes your initial investment capital and the monthly surplus you have available after accounting for your CPF contributions. Next is "Length of Time." This is your most powerful lever. The longer your money stays invested, the less heavy lifting you have to do yourself. Finally, there is the "Estimated Rate of Return." We encourage a realistic approach here. While it's tempting to plug in high double-digit numbers, a professional financial planner will tell you that a conservative, steady rate is the key to a resilient strategy.

The Role of Compounding in Wealth Preservation

Compounding is often called the eighth wonder of the world. It’s the "snowball effect" where your earnings start generating their own earnings. Imagine a professional starting their journey at age 30 versus age 45. The 30-year-old has a significant advantage because time does the work for them. In Singapore, we can maximize this effect through tax-advantaged accounts like the Supplementary Retirement Scheme (SRS). When you reinvest those tax savings into your strategy, the growth accelerates. Comprehensive retirement planning in Singapore relies heavily on these compounding projections. It ensures that your lifestyle remains protected long after you stop receiving a monthly salary.

Step-by-Step: How to Use an Investment Calculator for Your Goals

Before you open an investment calculator singapore, define your primary objective. Are you solving for education funding, building a retirement nest egg, or structuring legacy planning? Each goal requires a different timeline and risk appetite. Once your goal is set, gather your data. Look at your current liquid assets and determine your realistic monthly surplus after your CPF contributions. It’s vital to be honest about your spending habits so your projections remain grounded in reality.

An investment calculator is a powerful starting point for visualizing your future. However, you must adjust the inputs for the "Singapore Factor." This means accounting for local currency stability and our specific cost of living. While the calculator provides a "Total Balance" figure, your focus should be on your future purchasing power. A million dollars today won't buy the same lifestyle in 20 years. By adjusting your expected return to account for inflation, you get a clearer picture of what your wealth will actually provide.

Setting Realistic Interest Rate Benchmarks

Choosing the right interest rate is where many plans go off track. For context, historical S&P 500 returns often average around 10%, while conservative Singapore government bonds typically range between 2% and 4%. Within this spectrum, i12 investments strategies focus on achieving optimized, risk-adjusted returns that align with your specific profile. If you want a quick way to check your progress, use the Rule of 72 by dividing 72 by your expected interest rate to find how many years it takes to double your wealth. It's a simple mental shortcut that keeps you focused on the power of growth.

Accounting for Fees and Taxes

Precision requires looking at what you keep, not just what you earn. You should typically subtract 1% to 2% from your estimated rate of return to account for management fees and transaction costs. The impact of inflation is equally significant. With the MAS and MTI projecting core inflation to average between 1.5% and 2.5% for 2026, the value of your money shifts over time. For example, a $2 million retirement fund in 2026 could feel closer to $1.2 million by 2046 in terms of what it can actually buy. You may find it helpful to speak with a financial consultant to refine these variables and ensure your strategy remains resilient against these hidden costs.

Scenario Planning: Education Funding vs. Retirement Goals

Scenario planning is where an investment calculator singapore truly shines. It allows you to move beyond a single number and look at your life in phases. Most Singaporean professionals face a "Dual-Goal" challenge: funding a child’s high-tier education while simultaneously building a retirement fund that lasts. By running different scenarios, you can see how a choice today impacts your lifestyle 20 years from now. For example, if you aim to send your child to the Singapore American School or an overseas university, you need to account for tuition inflation that often outpaces core inflation.

We recommend using variance ranges to see your "Best Case" and "Worst Case" market scenarios. If the market underperforms for three years, how does that change your monthly savings target? This exercise highlights why a robust wealth protection strategy is vital. It acts as the safety net for your projections. Without it, a sudden health crisis or job loss could render your calculator results meaningless. A financial planner can help you build these buffers into your plan, ensuring your strategy remains resilient through every market cycle.

The Education Funding Sprint

Education funding is a sprint because the timeline is fixed. You can't delay university. Using a calculator helps you visualize the "Cost of Delay." If you start investing when your child is five years old, your monthly requirement is significantly lower than if you wait until they are ten. We often see families use i12 investments as a targeted growth engine for these education pots. This approach aims for higher growth during the early years to combat the 4% to 6% annual increase in global tuition fees. It's about making your capital work harder so you don't have to.

The Retirement Planning Marathon

Retirement is a marathon with a shifting finish line. With the statutory retirement age rising to 64 in July 2026, your "Years of Growth" input in the calculator needs to be precise. Start by modeling the gap between your projected CPF LIFE payouts and your desired monthly spend. Many clients find that CPF LIFE provides a solid foundation but falls short of a premium lifestyle. This is where the "Annuity Effect" comes in. By modeling how private annuities complement your investment portfolio, you can ensure a steady stream of income that isn't entirely dependent on market performance. Adjusting your years of growth for early retirement aspirations allows you to see if your current strategy can support a finish line earlier than age 64.

Common Pitfalls When Using Financial Calculators

Using an investment calculator singapore provides a fantastic baseline, but it can also lead to a false sense of security if you aren't careful. The most significant trap is the Linear Growth Fallacy. Real markets do not move in the perfectly smooth, upward line that a calculator displays. They fluctuate. A calculator shows you a mathematical average, but it cannot account for the emotional volatility you might feel during a market dip. If you rely solely on a straight line, you may not be mentally or financially prepared for the years when the "line" goes down.

You must also consider the "Sequence of Returns" risk. This is a critical factor for those nearing the new statutory retirement age of 64. If the market experiences a sharp drop just as you begin to withdraw funds, your portfolio's longevity is significantly reduced. This is why a "set and forget" mentality is dangerous. Your financial life is dynamic. We suggest you re-calculate your goals every 12 months. This ensures your strategy accounts for life changes, such as a career shift or a change in family circumstances, keeping your projections rooted in your current reality.

The Danger of Over-Optimistic Returns

Inputting a 15% annual return might make your future look bright on screen, but it is often a recipe for a funding shortfall. Over-optimism can lead you to under-save in the present. A financial planner uses "Stress Testing" to validate your results. They look at how your plan performs under various market conditions rather than just the best-case scenario. It is important to remember that historical performance is a guide, not a guarantee of future i12 investments results. Staying conservative with your return estimates helps ensure your plan remains resilient when the market is volatile.

Inflation: The Silent Wealth Eroder

Inflation is the silent thief of your future purchasing power. While the MAS projects core inflation to average between 1.5% and 2.5% for 2026, your personal lifestyle inflation could be much higher. Modeling a 3% versus a 5% inflation rate in your investment calculator singapore reveals how quickly your "Nominal Returns" can lose their actual value. Only "Real Returns"—what you have left after inflation—truly matter for your long-term security. Proper legacy planning ensures that the wealth you calculate today actually maintains its purchasing power when it reaches the next generation.

Need a professional eye to stress-test your numbers and ensure your strategy is truly on track? Connect with a financial planner today to refine your variables for a more secure future.

Beyond the Tool: When to Consult a Financial Consultant

An investment calculator singapore is a fantastic compass, but it isn't the captain of your ship. It provides the data points you need to start, but it can't navigate the emotional or legal complexities of your life. For instance, a tool won't understand how your estate tax nuances might impact your legacy planning. It won't account for the unique family dynamics that influence how you want to distribute your wealth. This is where the "Human Alpha" comes into play. A professional helps you maintain your discipline when market volatility strikes. They act as a steady hand, ensuring you don't abandon a sound strategy during a temporary downturn.

Moving from a generic online tool to a customized i12 investments portfolio strategy is a significant upgrade for your financial health. It shifts the focus from "what might happen" to "what we are making happen." We recommend taking your initial calculator results to a professional for a "Sanity Check." This process validates your assumptions about rates of return and inflation. It ensures your roadmap is actually drivable before you start the journey. It's about turning a mathematical possibility into a lived reality.

Personalized Strategic Wealth Analysis

There is a world of difference between a DIY calculation and professional financial roadmapping. A calculator is a snapshot; a roadmap is a live document. At Zenith Wealth, we integrate your daily cash flow management with your long-term projections. This holistic approach ensures your immediate needs never compromise your wealth protection goals. We also specialize in tailoring plans for complex milestones. If you are preparing for business succession or a strategic property acquisition, your plan needs to be as unique as your situation. We bridge the gap between your digital data and your real-world goals.

Executing Your i12 Investments Strategy

Data is only useful if you can act on it. Once your investment calculator singapore gives you a target, you need the right investment vehicles to get there. A consultant assists you in selecting options that align with your risk-adjusted return goals. Unlike a static tool, a professional provides ongoing portfolio rebalancing. This is crucial because market movements can shift your asset allocation away from your original intent. Staying on track requires proactive adjustments that a calculator simply cannot suggest. We invite you to connect with a financial consultant for a portfolio review to ensure your current strategy is truly built to last.

Take the Next Step Toward Your Financial Clarity

Harnessing an investment calculator singapore provides the essential data to begin your journey, but numbers alone don't build a legacy. You've seen how to identify your targets and avoid the common traps of over-optimism and linear projections. Now, it's time to move from theoretical growth to a tangible, stress-tested reality. True financial confidence requires a plan that adapts as quickly as the Singapore market does.

At Zenith Wealth, our team acts as authorized representatives of finexis advisory, specializing in the i12 investments framework. We offer boutique, personalized wealth management designed to bridge the gap between digital projections and human aspirations. Let's work together to ensure your education funding and retirement strategies are as resilient as they are ambitious.

Book a Consultation with a Zenith Financial Consultant today. We look forward to starting this conversation and growing alongside your family.

Frequently Asked Questions

What is a realistic rate of return to use in a Singapore investment calculator?

A realistic rate typically ranges between 4% and 7% for a diversified, balanced portfolio. While some years deliver higher returns, a conservative estimate ensures your plan remains resilient against market shifts. Using an investment calculator singapore with these benchmarks helps you avoid the trap of under-saving. Your financial planner can help you align these rates with specific strategies like i12 investments to match your personal risk tolerance.

Does the investment calculator account for Singapore’s CPF and SRS contributions?

Most basic online tools do not automatically include these localized schemes. You must manually input your CPF Ordinary Account at 2.5% and Special Account at 4.0% to see a complete financial picture. For SRS, remember the 2026 contribution cap is $15,300 for Singapore citizens and PRs. Adding these manual entries to your investment calculator singapore provides a much more accurate projection of your total retirement nest egg.

How do I factor in the cost of education for my child in Singapore?

You should factor in a 4% to 6% annual increase in tuition fees to stay ahead of rising costs. Base your initial target on current fees at institutions like the Singapore American School or specific overseas universities. A financial planner can help you calculate the "real cost" by adjusting for both inflation and potential currency fluctuations. This ensures your education funding strategy is robust enough to meet future demands without compromising other goals.

Can an investment calculator help me plan for early retirement?

Yes, you can model early retirement by reducing the "Years to Invest" and increasing the "Years of Withdrawal" inputs. Keep in mind that the statutory retirement age increases to 64 on July 1, 2026. This change might affect your CPF LIFE payout timeline and overall cash flow. Adjusting your calculator inputs allows you to see exactly how much extra monthly surplus you need to bridge the gap for an earlier exit.

Why do my calculator results look different from my actual bank statements?

Calculators assume smooth, linear growth, but real markets are volatile and move in unpredictable cycles. Your bank statements also reflect deductions for management fees, GST at 9%, and transaction costs that a simple tool might ignore. This discrepancy is why professional stress testing is vital. It helps you understand the difference between a mathematical model and the actual liquid wealth you'll have available.

How often should I update my investment calculations?

You should update your calculations at least every 12 months to stay on track. Regular reviews allow you to adjust for changes in Singapore's core inflation, which is projected to average between 1.5% and 2.5% for 2026. Major life events like a career change, marriage, or a new child also require a fresh look at your numbers. Staying proactive ensures your investment management strategy remains aligned with your current life stage.

What is the difference between simple and compound interest in these tools?

Simple interest is calculated only on your initial principal, while compound interest includes earnings on your accumulated interest over time. Most modern financial tools use compounding because it reflects how wealth actually grows over 10 to 20 years. This "snowball effect" is the primary driver of long-term wealth protection. It's the reason why starting your journey early is often more important than the specific amount you first invest.

Is it better to use a monthly or annual compounding frequency?

Monthly compounding is generally better as it more closely mirrors how most people save and how markets operate. If you make regular monthly contributions, this frequency provides a more precise look at your actual growth. It accounts for the interest earned on each new deposit throughout the year. This level of detail helps you set a more accurate monthly savings target for your retirement or legacy planning.