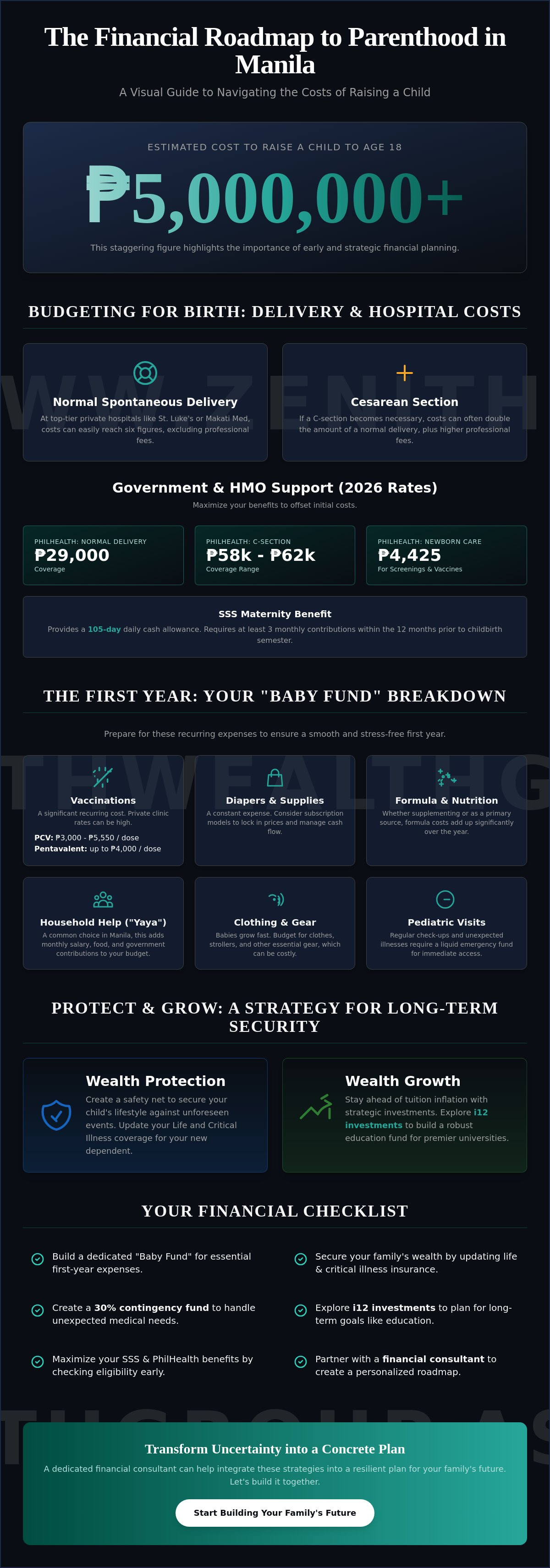

Raising a child in Metro Manila through age 18 can now cost upwards of ₱5 million. It's a staggering figure. You're likely wondering how to financially prepare for a baby in Manila while facing rising tuition fees and high hospital rates at St. Luke’s or Makati Med. It's natural to feel concerned about the shifting 2026 PhilHealth maternity benefits and the removal of traditional tax exemptions. You want the best for your family. You also need to protect your wealth.

This guide provides the clarity you need to master these costs. Build a resilient financial roadmap starting now. We'll break down the latest 2026 delivery expenses and create a sustainable first-year budget. We'll also explore how i12 investments can help secure your child’s future education. By working with a dedicated financial consultant, you can transform these challenges into a structured plan. Let’s start building your family’s future today.

Key Takeaways

- Compare delivery costs between top-tier private hospitals and government facilities to optimize your birth budget.

- Learn exactly how to financially prepare for a baby in Manila by building a dedicated "Baby Fund" for essential first-year expenses.

- Secure your family’s wealth by updating your life insurance and critical illness coverage to protect your new dependent.

- Discover how i12 investments can help you stay ahead of tuition inflation for Manila’s premier universities.

- Partner with a financial consultant to create a personalized roadmap that balances immediate needs with long-term legacy planning.

Budgeting for Birth: Navigating Maternity Costs in Metro Manila

Planning for a birth in Metro Manila requires a clear look at your choices. A natural delivery at a top-tier facility like St. Luke's Medical Center or Makati Medical Center can easily reach six figures. If a Cesarean section becomes necessary, costs often double. Understand these differences. It's the first step in learning how to financially prepare for a baby in Manila. Beyond the hospital bill, you must account for professional fees. OB-GYNs, anesthesiologists, and pediatricians set their own rates. These fees often depend on the complexity of the delivery. Professional fees alone can sometimes equal the hospital's base package.

The Private vs. Public Hospital Divide

Room rates in BGC and Makati reflect the premium service of Tier 1 hospitals. Private rooms can start at several thousand pesos per night. Nursery fees and medical supplies add up quickly. You should also prepare for "incidental" costs. This includes the newborn screening and hearing tests required by law. PhilHealth covers a Newborn Care Package worth ₱4,425. This helps with initial screenings and essential vaccines. However, private clinic follow-ups for vaccines like PCV can cost up to ₱5,550 per dose. Always build a "contingency fund" of at least 30% over your initial estimate. Unexpected medical needs happen. Having this buffer ensures you focus on your baby.

Government Benefits and HMOs

Maximize your available support. The Labor Code of the Philippines establishes the foundation for your leave and benefits. In 2026, PhilHealth has significantly increased its maternity coverage. Here is a quick look at the current rates:

- Normal Spontaneous Delivery: ₱29,000 coverage.

- Cesarean Section: ₱58,000 to ₱62,000 coverage.

- Newborn Care Package: ₱4,425 for essential screenings.

Check your SSS contribution history early. To qualify for the 105-day maternity benefit, you need at least three monthly contributions within the 12-month period before the semester of childbirth. This benefit is calculated based on your Average Monthly Salary Credit. It provides a daily cash allowance while you are unable to work.

Don't forget your corporate HMO. Review your policy for maternity riders. Some plans cover a portion of the hospital bill or professional fees. If you're looking for long-term growth to cover these and future family costs, exploring i12 investments can provide the diversification you need. A financial consultant can help you integrate these benefits into a broader wealth protection strategy. This proactive approach turns uncertainty into a manageable roadmap. Start your conversation now.

The First Year: Managing Cash Flow and Recurring Expenses

The first twelve months of parenthood often bring a flurry of new expenses. Beyond the delivery room, you'll need a dedicated Baby Fund to handle the transition. This fund covers recurring supplies like diapers, formula, and clothing. In Metro Manila, these costs fluctuate due to supply chain shifts and inflation. Imported baby gear also carries a premium in local boutiques. You must also budget for the "helper economy." Hiring a stay-in yaya is a standard choice for many Manila families. This adds monthly salaries, food, and mandatory government contributions to your ledger. Maintaining a liquid emergency fund is non-negotiable. Sudden pediatric visits shouldn't derail your monthly cash flow.

The Monthly Baby Budget Breakdown

Vaccinations are a significant recurring cost in the first year. In private clinics, rates for the PCV (Pneumococcal Conjugate Vaccine) range from ₱3,000 to ₱5,550 per dose. Pentavalent vaccines can cost up to ₱4,000. While the Expanded PhilHealth maternity and newborn packages provide essential support at birth, the first-year maintenance is your responsibility. Consider subscription models for essentials like diapers to lock in 2026 prices. Focus on needs over wants. A high-end nursery looks great, but your baby’s health and safety are the real priorities.

Adjusting Household Cash Flow

Your household financial dynamic will shift. Many couples move from a dual-income lifestyle to a single-income-plus-allowance mindset during maternity leave. Test this early. Start automating your savings six months before the due date. This simulates the new budget and builds necessary liquidity. It's also a great time to check for non-taxable "de minimis" benefits from your employer. As of 2026, the rice subsidy stands at ₱2,500 per month, and the medical cash allowance for dependents is ₱2,000 per semester. These small wins add up when learning how to financially prepare for a baby in Manila.

If you have existing debt, a financial planner can help you restructure payments to free up cash flow. This proactive step ensures you aren't overextended while managing new costs. This is also an ideal time to integrate i12 investments into your strategy. These vehicles offer a way to grow wealth while you manage daily expenses. Preparing for a baby is about balancing today’s needs with tomorrow’s growth. It requires clear numbers and a steady hand. We are here to help you start that conversation.

Protecting Your Growing Family: Insurance and Wealth Protection

Your family's safety net is about more than just paying hospital bills. It's about ensuring your child’s lifestyle remains secure, no matter what happens to your income. For many in Metro Manila, this means balancing the needs of a newborn with the care of aging parents. This "sandwich generation" pressure makes robust wealth protection essential. Updating your life insurance is a critical step in how to financially prepare for a baby in Manila. You're no longer just protecting yourself. You're protecting a future.

Consider maternity insurance early in your pregnancy. These specialized policies often cover congenital conditions and pregnancy complications that standard plans might exclude. It's a proactive way to manage risks that PhilHealth or basic HMOs don't fully address. Secure your peace of mind before the baby arrives.

Life Insurance and Income Replacement

Calculating your "human life value" helps determine exactly how much coverage your family needs to replace your income. In 2026, many young families opt for term insurance to maximize coverage while keeping premiums manageable. Others prefer whole life policies for the built-in cash value component. You can find more foundational strategies in our guide to Wealth Protection. The goal is to create a buffer that covers future education, housing, and daily needs without compromise.

Health and Medical Security

Medical security is your next layer of defense. Corporate HMOs are a great start, but they often have low limits for major illnesses. Prioritize Critical Illness coverage for the primary breadwinner. This provides a lump sum payment upon diagnosis, allowing you to focus on recovery without draining your savings. A financial consultant can help you evaluate multi-carrier options to find the best fit for your health history and budget. Don't overlook the mother’s postpartum health. Ensuring she has access to recovery care and specialist support is part of a complete medical plan.

Finally, look toward legacy planning. This ensures your child’s guardianship is legally clear. It’s a quiet act of love that prevents family disputes and legal hurdles during difficult times. Integrating i12 investments into this plan allows you to build a protected pool of assets that grows over time. This approach secures your child’s future and your family’s long-term wealth. It’s about building a legacy that starts from day one. If you're ready to review your current coverage, a financial planner can provide a personalized assessment to close any gaps in your protection.

Strategic Long-Term Planning: Education Funds and i12 Investments

Education is a long-term commitment. You aren't just saving for a degree; you're funding a lifetime of opportunity. Understanding how to financially prepare for a baby in Manila means looking far beyond the first year. Tuition for top universities in the city increases by about 10% every year. Based on current trends, a four-year degree in 2040 could easily exceed ₱2 million at premier institutions. Simple savings accounts won't keep up with this level of inflation. You need a strategy that grows faster than the rising cost of living.

The Cost of Education in Manila

Choose your path early to set realistic targets. Local private school paths offer excellent foundations, but international school tracks carry a much higher price tag. Starting at birth is the only way to truly leverage the power of compound interest. Every year you wait significantly increases the monthly amount you need to set aside. For a deeper look at planning frameworks and how to structure your goals, explore our guide on Education Funding. It provides the structure needed to hit these ambitious long-term targets.

Leveraging i12 Investments

Move beyond traditional educational plans. These older products often lack the flexibility modern families need in a fast-changing world. Instead, focus on i12 investments for a professional edge. This approach emphasizes diversified, long-term growth across global markets. It allows you to invest in assets outside of local Manila markets, which is vital for risk management. By spreading your wealth across different sectors and regions, you protect your family from local economic downturns. It's about building a robust portfolio that stands the test of time and market shifts.

Use dollar-cost averaging to your advantage. By investing a fixed amount regularly into your i12 investments, you mitigate market volatility. You buy more units when prices are low and fewer when they are high. It's a disciplined, steady way to build wealth without the stress of trying to time the market. A financial planner can help you monitor performance and adjust your asset allocation as your child nears college age. This ensures your roadmap stays on track despite changing life circumstances. Start your long-term planning today to give your child the best possible start.

Building Your Family’s Roadmap with a Financial Consultant

You have the data. You know the hospital rates and the vaccination schedules. But a list of costs is just a snapshot. It isn't a strategy. Learning how to financially prepare for a baby in Manila requires moving from a reactive mindset to a proactive one. 2026 is the year to shift from simple saving to strategic wealth management. You are building a foundation for a new life. Do it with precision. A personalised roadmap ensures every peso works toward your child’s future while protecting your current lifestyle.

Execution is where many parents feel overwhelmed. The transition from a dual-income household to a growing family involves many moving parts. You need to balance immediate liquidity with long-term growth. This is why a strategic approach is vital. It’s about more than just surviving the first year. It’s about thriving for the next twenty. Let’s look at how to bridge that gap.

Why a Financial Consultant is Essential

Generic online advice can't account for your specific family goals or cross-border assets. A financial consultant provides the objective perspective needed to balance immediate nursery needs with long-term growth. Zenith Wealth supports parents across the Philippines and Singapore. We help you navigate complex regional regulations and bridge the gap between where you are and where your family needs to be. This clarity allows you to invest with confidence. Contact Zenith Wealth for a consultation to start your journey.

Next Steps for Expectant Parents

Don't let your new arrival derail your future. Schedule a 2026 family wealth audit now. While you focus on the baby, we'll ensure your Retirement Planning remains on track. It is about securing your future so you can fully enjoy theirs. Use this final checklist to stay organised:

- Finalise your Birth Fund: Ensure your 30% contingency buffer is liquid and ready.

- Complete an Insurance Audit: Verify that your wealth protection covers your new dependent and potential legacy needs.

- Set up i12 investments: Start your long-term growth journey today to stay ahead of education inflation.

The best time to start was yesterday. The second best time is now. Your family’s roadmap is unique. It should reflect your values and your aspirations. We are ready to engage and grow alongside you. Let's start the conversation and build a legacy that lasts for generations.

Start Your Family’s Financial Journey Today

A resilient financial plan is the greatest gift you can provide for your child. You now have the roadmap to handle the rising costs of delivery, manage first-year cash flow, and protect your growing family from unexpected risks. Mastering how to financially prepare for a baby in Manila is not just about meeting immediate expenses. It is about shifting your mindset toward strategic wealth management that secures your child’s future opportunities through every stage of life.

Zenith Wealth is here to guide you through these transitions. We are authorized representatives of finexis advisory, specializing in Education Funding and Legacy Planning. Our team brings deep expertise in i12 investments to ensure your family's portfolio remains robust and diversified. Don't leave your wealth to chance as you enter this exciting new chapter. Book a consultation with a Zenith Wealth financial consultant today. We look forward to helping you build a legacy that lasts for generations. Congratulations on your growing family.

Frequently Asked Questions

How much does a normal delivery cost in a private Manila hospital in 2026?

Private hospital packages for normal delivery in 2026 often range from ₱100,000 to ₱150,000. This figure depends on your choice of room and doctor. PhilHealth provides a ₱29,000 case rate for these deliveries to help reduce your out of pocket costs. It's vital to canvass specific rates at facilities like St. Luke’s or Makati Med early. Always account for professional fees separately as they vary significantly by specialist.

Does PhilHealth cover maternity expenses for voluntary members?

PhilHealth covers maternity expenses for all member types, including voluntary members, provided they meet specific contribution requirements. You must have at least three monthly contributions within the 12 month period before the semester of childbirth. This coverage includes the ₱4,425 Newborn Care Package for your baby. Understanding these benefits is a key part of learning how to financially prepare for a baby in Manila effectively.

What is the best way to save for my child’s college education in the Philippines?

The best way to save for college is through a diversified investment portfolio that outpaces the 10% annual tuition inflation in Manila. Moving away from traditional fixed plans toward i12 investments allows your capital to grow in global markets. Starting at birth is essential. This gives your money the longest possible time to benefit from compound interest before your child reaches university age in 2040 or beyond.

Should I get maternity insurance if I already have a corporate HMO?

You should consider maternity insurance if your corporate HMO has low coverage limits or excludes pregnancy complications. Most standard HMOs don't cover congenital conditions or neonatal intensive care expenses in full. Maternity insurance acts as a critical supplement. It provides a lump sum or higher reimbursement for specific risks that basic plans often overlook. This ensures your family wealth remains protected during the transition.

How much should a "Baby Emergency Fund" contain for Manila residents?

A "Baby Emergency Fund" should ideally contain three to six months of anticipated recurring expenses for your child. In Metro Manila, this includes the cost of formula, diapers, and yaya salaries. You should also maintain a 30% contingency buffer on top of your estimated birth costs. This liquidity protects you from sudden pediatric visits or unexpected medical needs that often arise during the first year of parenthood.

What are i12 investments and how do they benefit new parents?

i12 investments refer to a strategic investment framework focused on diversified, long-term growth for family portfolios. These investments benefit new parents by providing access to global assets that help hedge against local economic shifts. Working with a financial planner to set up these accounts ensures your strategy remains aligned with your child’s future education. This approach provides a professional edge that simple savings accounts cannot match.

Is it better to invest in USD or PHP for a child’s future education?

The choice between USD and PHP depends on where you expect your child to attend university. If you are eyeing international school tracks or education abroad, investing in USD helps mitigate currency risk. For local Manila universities, PHP investments are standard. However, a balanced approach using i12 investments can provide exposure to both. This diversification protects your purchasing power over the next two decades as costs rise.

When is the best time to hire a financial consultant when expecting a baby?

The best time to hire a financial consultant is during your first trimester. Early planning allows you to audit your insurance and adjust your cash flow before the baby arrives. It also gives you more time to set up i12 investments and maximize the power of compound interest. A proactive approach ensures your family’s roadmap is solid before you shift your focus entirely to your newborn’s care.