What if your biggest retirement risk isn't a market crash, but simply spending your own money in the wrong order? Most Singaporeans spend decades focused on the "climb" of wealth accumulation. It's natural to feel a sense of vertigo when it's finally time to start the descent. With the MAS 2026 inflation forecast reaching up to 2.5%, finding effective decumulation strategies for retirees in Singapore is more critical than ever. It's a challenge that requires more than just a savings account. It requires a strategy.

You'll learn how to transition from building wealth to creating a sustainable, tax-efficient income stream tailored for today's market. This guide provides a clear withdrawal hierarchy to fund your lifestyle regardless of market volatility. We'll look at the 2026 CPF Enhanced Retirement Sum of $440,800, explain how to handle the new SRS withdrawal age of 64, and show how i12 investments can help bridge the gap. Our goal is to give you the peace of mind that comes from a professional financial planner's perspective. Let's start the conversation about your future.

Key Takeaways

- Shift your mindset from building a nest egg to creating a reliable paycheck. Understand why decumulation requires a different strategy than saving.

- Navigate the 2026 CPF retirement sum updates and the new SRS withdrawal age of 64. Learn how to maximize these foundational pillars for a tax-efficient income floor.

- Implement proven decumulation strategies for retirees in Singapore to protect your lifestyle against inflation. Synchronize your assets into a multi-layered payout plan.

- Discover how i12 investments can bridge the gap between basic needs and your ideal retirement lifestyle. Build a resilient portfolio designed for consistent monthly cash flow.

- Learn the optimal withdrawal hierarchy to minimize tax liability and prevent portfolio exhaustion. See why a financial planner is essential for managing complex 2026 regulations.

What is Decumulation and Why Is It Harder Than Saving?

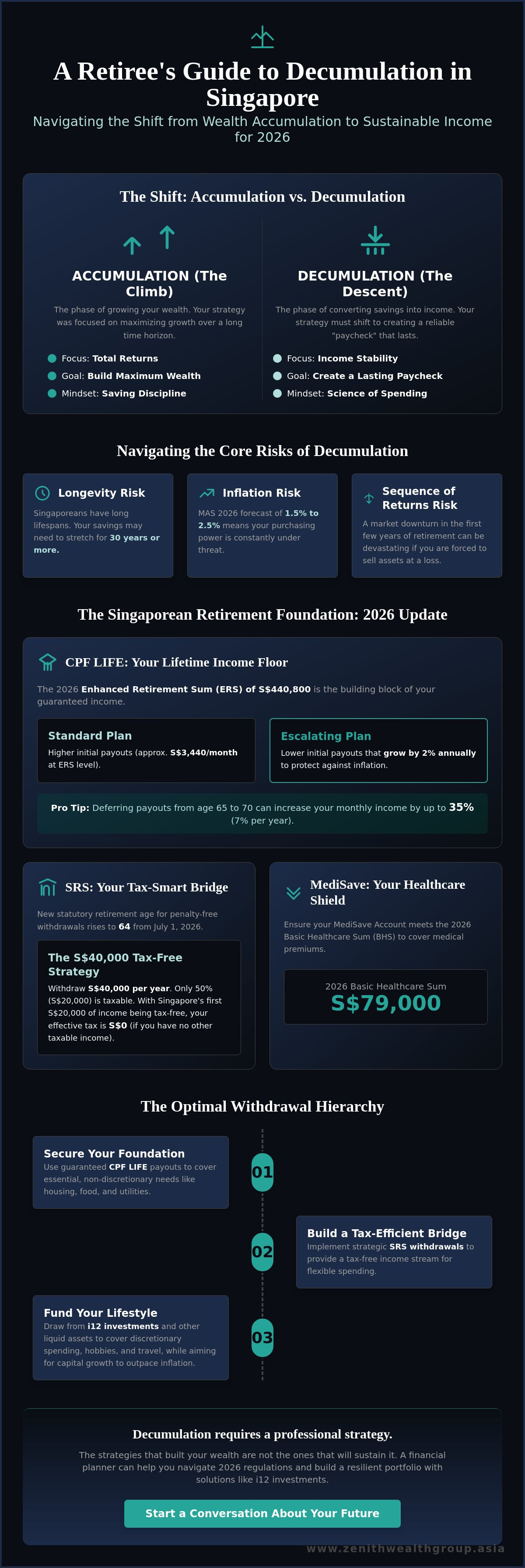

Decumulation is a strategic transition from asset growth to income stability. It's the process of turning a lifetime of savings into a monthly "paycheck" that lasts as long as you do. While the accumulation phase is about the discipline of saving, this new phase is about the science of spending. It's often where the most complex financial decisions begin.

For many Singaporeans, the psychological shift is the hardest part. You've spent decades watching your bank balance climb. Now, you're asked to watch it decrease. This often leads to the "Spend-Down Paradox," where retirees underspend and sacrifice their quality of life out of fear. This is the heart of the Retirement spend-down challenge. Without a plan, the anxiety of a dropping net worth can be paralyzing.

The stakes are also higher because of sequence of returns risk. During your career, a market dip was just a buying opportunity. In retirement, a market downturn in the first few years can be devastating. If you're forced to sell assets at a loss to fund your lifestyle, your portfolio might never recover. This is why effective decumulation strategies for retirees in Singapore must prioritize capital preservation alongside income.

The Core Risks of Decumulation in 2026

Longevity and inflation are your primary hurdles. Singaporeans have some of the longest lifespans in the world, meaning your savings may need to stretch for thirty years or more. At the same time, the MAS 2026 inflation forecast of 1.5% to 2.5% means your purchasing power is constantly under threat. Healthcare costs typically rise even faster, making it vital to have an income stream that keeps pace with the cost of living.

Why Your 'Accumulation' Strategy Won't Work Now

The strategies that got you here won't get you through retirement. In the past, you focused on total returns and long-term growth. Now, the focus shifts to yield and cash flow. You need immediate access to cash without the risk of selling in a down market. This requires a different asset mix, including frameworks like i12 investments, which prioritize resilience and steady payouts.

Liquidity becomes your best friend. You can't wait five years for a stock to rebound when the bills are due today. A professional financial planner can help you structure your assets to ensure you always have cash on hand. Transitioning safely requires an objective perspective to avoid costly tax mistakes or emotional decisions. If you're ready to start this transition, feel free to connect with our team today.

The Singaporean Foundation: Optimizing CPF LIFE and SRS

Effective decumulation strategies for retirees in Singapore begin with the Central Provident Fund (CPF). As of 2026, the Full Retirement Sum (FRS) stands at $220,400, while the Enhanced Retirement Sum (ERS) has reached $440,800. These are the building blocks of your guaranteed lifetime income. By decumulating wisely, you ensure your basic needs are covered before addressing lifestyle goals. It's about securing your floor so you can reach for the ceiling.

CPF LIFE: Your Lifetime Annuity Strategy

The choice between the Standard and Escalating plan is more critical than ever given the MAS 2026 inflation forecast of up to 2.5%. The Standard plan offers higher initial payouts, roughly $3,440 for those at the ERS level. However, the Escalating plan provides payouts that grow by 2% annually. This helps protect your purchasing power as healthcare and living costs rise. If your health is good and you have other liquid assets, deferring payouts from age 65 to age 70 can increase your monthly income by up to 7% for every year you wait. For a deeper dive into these mechanics, see our guide on Understanding CPF Retirement Payouts in 2026.

Strategic SRS Drawdowns

The Supplementary Retirement Scheme (SRS) is your secondary engine. From July 1, 2026, the statutory retirement age for penalty-free withdrawals rises to 64. You have a 10-year window to empty this account. Timing is everything. If you start too early, you might pay unnecessary tax. If you wait too long, you might be forced into a higher tax bracket. If you have no other taxable income, you can effectively withdraw $40,000 per year tax-free. This works because only 50% of the withdrawal is subject to tax, and the first $20,000 of income in Singapore is effectively tax-free. Our article on Mastering the SRS Account: A 2026 Strategic Guide to Tax Savings explains how to invest these funds during the withdrawal phase to stay ahead of inflation.

Don't forget the Retirement Sum Topping-Up (RSTU) scheme. It offers tax relief while building your income floor, though it reduces your immediate liquidity. You must also balance your MediSave Account to meet the 2026 Basic Healthcare Sum (BHS) of $79,000. This ensures your Integrated Shield Plan premiums are covered without dipping into your cash reserves. Coordinating these pillars with i12 investments allows for a more robust retirement. A financial planner can provide the objective perspective needed to synchronize these dates and sums. It's about creating a plan that works as hard as you did.

Comparing Private Decumulation Vehicles and i12 investments

CPF LIFE provides a solid floor, but it rarely funds a premier retirement on its own. If you want to travel, pursue hobbies, or enjoy the best of Singapore's dining scene, you need a strategy for your private wealth. This is where decumulation strategies for retirees in Singapore move beyond government schemes. While the 2026 CPF LIFE Standard plan offers a reliable payout, that amount is largely fixed. In an environment where inflation is forecasted up to 2.5%, your purchasing power will naturally erode over a thirty year retirement. You need an engine that grows.

We use i12 investments as a framework to address this gap. It's designed for resilience and steady cash flow. You may have considered private annuities or Investment-Linked Policies (ILPs) for monthly income. These products have their place, but they often come with high costs or rigid structures. Many retirees now look toward a mix of dividend-paying stocks and Singapore Real Estate Investment Trusts (REITs). These assets can provide the yield necessary to supplement your base income while keeping your capital accessible.

Private Annuities vs. i12 investments

The choice between guaranteed and variable income depends on your personal risk tolerance. Traditional private annuities offer a "set it and forget it" approach. However, they often lack liquidity. If you need a large sum for a family emergency or a sudden healthcare need, your capital is often locked away behind surrender charges. i12 investments provide the growth needed to beat 2026 inflation while offering much better flexibility. This framework allows you to adjust your withdrawals based on your actual spending needs rather than being stuck with a pre-set schedule.

Risk Management in Private Portfolios

Diversification must go beyond Singapore's borders. While our local market is stable, global exposure is vital for a resilient portfolio. You should diversify across different sectors and geographies to protect against localized economic downturns. Using low-volatility assets helps preserve your principal while you draw an income. It's about finding the balance where your money works for you without causing sleepless nights during market swings.

Stress-testing is a crucial step in this process. You should ask a financial consultant to run various scenarios on your portfolio. What happens if there's a significant market correction? What if inflation stays at the high end of the MAS forecast for several years? A professional financial planner can help you build a "buffer" to ensure your lifestyle remains funded. If you're ready to see how these pieces fit together for your specific situation, feel free to connect with our team for a chat.

The 2026 Withdrawal Hierarchy: A Practical Step-by-Step

Success in retirement isn't just about how much you have. It's about the order in which you spend it. A clear "order of operations" helps you minimize taxes and maximize the longevity of your portfolio. Implementing effective decumulation strategies for retirees in Singapore requires a disciplined hierarchy. This prevents the emotional trap of overspending in good years or underspending in bad ones. It keeps your lifestyle on track regardless of market noise.

- Step 1: Calculate your 2026 needs. Separate your "Essential" expenses like food and utilities from "Discretionary" spending like travel. Factor in the MAS 2026 inflation forecast of 1.5% to 2.5% to ensure your budget remains realistic.

- Step 2: Clear high-interest debt. Before you start drawing an income, exhaust taxable cash reserves and pay off any remaining high-interest liabilities. This simplifies your monthly cash flow immediately.

- Step 3: Trigger SRS withdrawals. Aim for the tax-free threshold. With the statutory retirement age rising to 64 on July 1, 2026, you can withdraw up to $40,000 annually tax-free if you have no other taxable income.

- Step 4: Layer in CPF LIFE. Let your guaranteed floor handle the essentials. Whether you choose the Standard or Escalating plan, this is your bedrock.

- Step 5: Use i12 investments for the "bonus." This layer provides inflation-adjusted income for your discretionary goals. It bridges the gap between a basic retirement and the lifestyle you actually want.

The 'Bucket Strategy' for 2026

Managing volatility requires a structured approach to your assets. We recommend a three-bucket system for immediate peace of mind. Bucket 1 should hold 2 years of living expenses in cash or cash equivalents. This ensures you never have to sell assets during a market dip. Bucket 2 focuses on mid-term stability through bonds and i12 investments. Finally, Bucket 3 holds equities for long-term growth. This structure ensures your money lasts 30 years or more, even with the rising standard of living in Singapore.

Adjusting for 2026 Economic Realities

Flexibility is your greatest asset. Use dynamic spending to reduce withdrawals during market downturns. This protects your portfolio's "principal" for the future. You must also budget for healthcare inflation, especially for private hospital care in Singapore. For more details on the broader landscape, read The Complete Guide to Retirement Planning in Singapore (2026 Edition). Ready to build your personalized hierarchy? Connect with a financial planner to start your plan today.

Partnering with a Financial Planner for Your Decumulation Journey

Moving from a saving mindset to a spending mindset is a massive emotional shift. It's often where the most expensive mistakes happen. DIY decumulation can lead to portfolio exhaustion if you don't account for market cycles or inflation. Many retirees also fall into tax traps when withdrawing from their accounts without a clear timeline. Implementing robust decumulation strategies for retirees in Singapore is a high-stakes task. It requires more than just a spreadsheet; it requires foresight.

A financial consultant provides an objective, human perspective that software cannot replicate. They help you stay disciplined when markets are volatile. They also ensure you don't underspend out of fear, which is a common paradox in retirement. At Zenith Wealth, we tailor i12 investments to your specific needs. We focus on creating a resilient income stream that respects your hard work. Our goal is to move you from a place of anxiety to an action-oriented roadmap.

Why Specialized Retirement Advisory Matters

Effective planning goes beyond simple product sales. It involves holistic cash-flow modeling that accounts for your unique lifestyle. We look at how your spending might change over thirty years. This includes budgeting for travel in your early retirement years and healthcare in the later stages. We also ensure your strategy doesn't compromise your children's inheritance. Legacy planning is a core part of our process. We help you balance your current needs with the desire to leave something behind. For more on this, read our guide on Legacy Planning in Singapore: The 2026 Guide to Protecting Generational Wealth.

Start Your Conversation with Zenith Wealth

We're here to act as your modern professional guide. The financial landscape of 2026 is complex, but it doesn't have to be overwhelming. We specialize in refining decumulation strategies for retirees in Singapore to ensure they remain sustainable and tax-efficient. Our team provides transparent guidance to help you navigate CPF changes and SRS regulations. We value personal connection over institutional coldness. We're ready to listen to your story and help you build a future you can trust. Your retirement should be a time of freedom, not a time of worry. Take the first step toward a secure and joyful payout strategy. Book a consultation with our financial planners today.

Build Your Sustainable Retirement Roadmap

Transitioning from years of saving to a lifetime of payouts is a major shift. You now have a framework to synchronize your CPF LIFE, optimize the SRS withdrawal window, and layer in private assets for a resilient income floor. These decumulation strategies for retirees in Singapore are designed to protect your lifestyle against the unique economic landscape of 2026. By following a structured withdrawal hierarchy, you ensure your money works as hard as you did during your career.

It's time to turn these insights into a personalized action plan. At Zenith Wealth, we're authorized representatives of finexis advisory Pte Ltd and specialists in the i12 investments framework. We build tailored legacy and retirement roadmaps that prioritize your peace of mind and long-term security. Don't let complex regulations or market volatility cloud your vision for the future. Secure your retirement income with a professional financial planner at Zenith Wealth. We're ready to start the conversation and guide you through this next chapter. Your best years are just ahead.

Frequently Asked Questions

What is the best age to start decumulation in Singapore?

The ideal age depends on your personal liquidity, but age 65 is the standard starting point to align with CPF LIFE payouts. If you have sufficient cash reserves, deferring your payouts until age 70 can increase your monthly income by roughly 7% for every year you wait. This delay creates a much stronger income floor for your later years. It’s a strategic choice that a financial planner can help you model based on your health and goals.

Can I rely solely on CPF LIFE for my retirement income?

CPF LIFE is designed to cover your basic essential needs, but it is rarely enough for a premier lifestyle. Most retirees find that while CPF LIFE provides a secure floor, they need private decumulation strategies for retirees in Singapore to fund travel, hobbies, and higher healthcare tiers. Integrating i12 investments can help bridge this gap. This ensures your discretionary spending isn't limited by government payout ceilings.

How does the SRS withdrawal tax work in 2026?

Starting July 1, 2026, the statutory retirement age for penalty-free SRS withdrawals rises to 64 for those born on or after July 1, 1963. Only 50% of your withdrawal amount is subject to income tax during the 10-year withdrawal window. If you have no other taxable income, you can effectively withdraw up to $40,000 annually tax-free. This makes the SRS a powerful tool within broader decumulation strategies for retirees in Singapore.

What are i12 investments and how do they fit into retirement?

i12 investments are a specialized framework focused on creating resilient, income-generating portfolios for the decumulation phase. Unlike growth-only strategies, this approach prioritizes yield and capital preservation to ensure a steady monthly "salary." It fits into your retirement by providing the inflation-adjusted income that CPF LIFE lacks. This framework helps you maintain your standard of living even as costs rise in Singapore.

How much can I safely withdraw from my portfolio every year (The 4% Rule)?

The 4% rule is a traditional guideline, but modern retirement often requires a more dynamic approach. While withdrawing 4% of your initial portfolio is a starting point, you should adjust this based on annual market performance to avoid portfolio exhaustion. In years of poor market returns, a financial planner might suggest reducing discretionary withdrawals. This flexibility is key to ensuring your capital lasts for thirty years or more.

Should I pay off my mortgage before starting my decumulation strategy?

Eliminating your mortgage is generally recommended because it significantly lowers your "Essential" monthly spending. Reducing fixed costs gives you more flexibility to manage your portfolio withdrawals during market downturns. However, you should compare your mortgage interest rate against the potential yield from i12 investments. If your investment returns are significantly higher than your loan costs, a financial consultant can help you decide if a slower repayment is more efficient.

How do I protect my retirement income from high inflation in Singapore?

You can combat inflation by choosing the CPF LIFE Escalating plan, which offers payouts that grow by 2% annually. Beyond CPF, it’s vital to hold assets like REITs or i12 investments that have the potential to grow their distributions over time. With the MAS 2026 inflation forecast reaching up to 2.5%, a static income is your biggest risk. Diversifying into global markets also helps protect your purchasing power.

What is the role of a financial consultant in the decumulation phase?

A financial consultant provides the objective perspective needed to manage the complex transition from saving to spending. They specialize in tax optimization, especially regarding SRS withdrawals, and stress-testing your portfolio against various economic scenarios. Their role is to act as a proactive partner. They ensure your decumulation roadmap remains on track so you can focus on enjoying your retirement years without financial anxiety.