Will your CPF LIFE payouts actually be enough to sustain you, or are you just funding a bare-bones existence? With the 2026 Enhanced Retirement Sum now at S$440,800, many Singaporeans realize that even hitting the maximum cap might not provide the lifestyle they envisioned. It's normal to feel a sense of urgency when inflation eats into your projected savings. Finding the best life insurance for retirement planning Singapore has to offer is the most effective way to bridge this gap and ensure your hard work translates into a comfortable reality.

We understand that the sea of Whole Life, Term, and Annuity options can feel overwhelming, especially when you're looking for honest advice rather than a sales pitch. This guide provides a clear framework to rank the top private plans available in 2026, from the capital-guaranteed Manulife WealthGen to NTUC Income's Gro Retire Ease. You'll learn how to layer these products with your SRS contributions to create a guaranteed income floor that outlasts any market cycle. Let's look at the data so you can move forward with quiet confidence.

Key Takeaways

- Understand why guaranteed income floors are now more critical than speculative growth in the 2026 economic climate.

- Compare top providers like Singlife and Manulife to find the right balance between flexibility and early breakeven points.

- Build a robust "Retirement Pyramid" by selecting the best life insurance for retirement planning Singapore to bridge the gap left by CPF LIFE.

- Maximize your SRS contributions by using them to fund private annuities. This reduces your tax bill while securing your future.

- Discover why independent advice is essential to access a wider range of solutions compared to single-brand tied agents.

##Why Life Insurance is the Engine of Singaporean Retirement in 2026

Life insurance has evolved. It's no longer just a "death benefit" meant for those you leave behind. In 2026, it serves as a dual-purpose engine for both protection and wealth accumulation. Retirement Income Insurance is a financial contract that provides guaranteed lifelong or fixed-term payouts to ensure you never outlive your savings. This shift in focus allows you to build a private pension that works alongside government schemes.

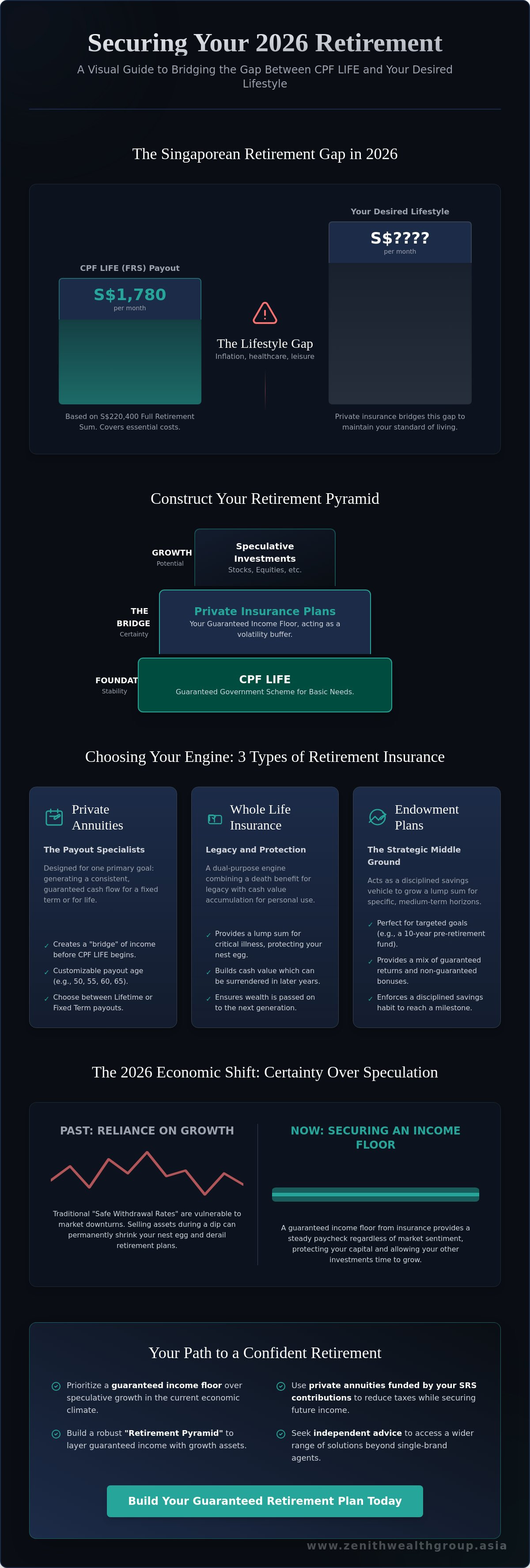

Relying solely on the Central Provident Fund (CPF) is a risky strategy for your desired lifestyle. The 2026 Full Retirement Sum (FRS) is set at S$220,400, which yields an estimated monthly payout of only S$1,780. While this covers essential costs, it doesn't account for the 2026 inflation rates that have pushed up the price of healthcare and leisure. Securing the best life insurance for retirement planning Singapore offers is the most effective way to bridge this "lifestyle gap" and maintain your standard of living.

2026 has changed how we view risk. Investors now value a "guaranteed income floor" much more than the "potential growth" of aggressive portfolios. You need certainty when you're no longer drawing a salary. Private insurance plans provide that certainty by locking in returns that aren't tied to the daily whims of the stock market.

The 2026 Economic Context for Retirees

The current interest rate environment is in a state of flux. The recent Fed rate cut has started to influence the yields of new insurance policies across Singapore. While bond yields might soften, insurance participating funds use a "smoothing" process to keep your bonuses stable. This makes capital-protected insurance a sanctuary for those moving away from the volatility of equities in 2026.

Insurance vs. Pure Investing

The traditional "Safe Withdrawal Rate" is hard to manage when markets are down. Selling your stocks during a dip can permanently shrink your nest egg. Insurance acts as a vital volatility buffer for your overall portfolio. It provides a psychological advantage because you'll receive a steady check every month regardless of market sentiment. This stability allows your other investments the time they need to recover and grow. If you're ready to see how these layers can work for you, drop us a line to start your plan.

##Comparing the 3 Best Insurance Vehicles for Retirement

Not all policies are built the same. To find the best life insurance for retirement planning Singapore, you must first decide which financial "engine" will drive your future payouts. In the 2026 market, three main vehicles dominate the landscape: Private Annuities, Whole Life Insurance, and Endowment plans. Each serves a distinct purpose, and the right choice depends on whether you value immediate cash flow, long term protection, or targeted savings milestones.

Understanding these differences is vital because your choice determines your "guaranteed income floor." While some plans focus on high potential returns through non-guaranteed bonuses, others prioritize capital preservation. Recent academic research on Singaporean retirement preparedness highlights that many residents still struggle to estimate their post-retirement expenses accurately. Selecting the wrong vehicle can lead to a shortfall when you need funds the most.

Private Annuities: The Payout Specialists

These plans are designed for one primary goal: consistent, monthly cash flow. Products like Singlife Flexi Retirement II offer incredible flexibility in the 2026 economic environment. You can customize your payout age to start at 50, 55, 60, or 65. This allows you to create a "bridge" of income before your CPF LIFE payouts begin. You'll need to choose between "Lifetime" payouts, which protect you against outliving your money, and "Fixed Term" payouts, which typically provide a higher monthly sum for a set duration, such as 10 or 20 years.

Whole Life Insurance: Legacy and Protection

Whole life policies are the heavy lifters for legacy planning. They combine a death benefit with cash value accumulation. In 2026, retirees often favor these plans for their "Critical Illness" multipliers. This feature ensures that if a health crisis occurs during your retirement years, you receive a significant lump sum. This protects your retirement nest egg from being depleted by medical bills. You can eventually surrender the policy for its cash value or keep it active to pass on wealth to your family.

Endowment plans act as a strategic middle ground. They are perfect for specific horizons, such as a 10 year window before you stop working. While they don't offer the lifelong income of an annuity, they provide a disciplined way to grow a lump sum. When comparing these options, always check the illustrated yield against the guaranteed portion. If you want to see how these different vehicles stack up for your specific age and goals, drop us a line for a personalized breakdown.

##The 2026 Showdown: Singlife vs. AIA vs. Income vs. Manulife

Choosing the right insurer is about more than just the brand name. It's about how their participating fund performs and how much flexibility they offer during your "golden years." In the current 2026 landscape, various leading providers dominate the market. Each has carved out a niche to address the specific fears of retirees, from inflation spikes to unexpected health costs. Finding the best life insurance for retirement planning Singapore requires a side by side look at the distinct strategies from leading providers.

The 2026 economic environment, marked by recent Fed rate adjustments, has forced insurers to be more competitive with their "guaranteed" components. While

##Strategic Integration: Layering Insurance with CPF LIFE and SRS

A successful retirement isn't about picking one "perfect" product. It's about how you layer different assets to create a resilient income stream. We call this the "Retirement Pyramid." At the base, you have CPF LIFE, providing a lifelong, inflation-hedged foundation. However, to truly secure your future, you need a middle layer. This is where the best life insurance for retirement planning Singapore comes into play. It fills the gap between basic survival and the lifestyle you actually want.

Many clients ask if private insurance is redundant since they already have CPF LIFE. It's a fair question. The reality is that CPF LIFE has limits. For someone turning 55 in 2026, the Enhanced Retirement Sum (ERS) is capped at S$440,800. If your desired monthly spending exceeds the estimated S$3,440 payout, you face a shortfall. Finding the best life insurance for retirement planning Singapore provides the additional guaranteed income floor you need. It also offers something CPF LIFE doesn't: the ability to start payouts as early as age 50 or 55, bridging the "early retirement" gap before government payouts begin at age 65.

The SRS-Insurance Hack

Using your Supplementary Retirement Scheme (SRS) funds to purchase a single-premium annuity is a favorite strategy in 2026. As of July 1, 2026, the statutory retirement age for penalty-free SRS withdrawals is 64. By investing your SRS cash, which only earns 0.05% p.a. in a bank account, into a private retirement plan, you potentially increase your yield significantly. This move is tax-efficient. Only 50% of your SRS withdrawals are taxable after age 64. If you spread these withdrawals over the 10-year window alongside your insurance payouts, you can often keep your tax liability at zero.

Annuity vs. CPF LIFE: The Balanced Approach

Think of private annuities as a way to customize your cash flow. While CPF LIFE is excellent for longevity risk, private plans offer flexible terms. You can choose a 10 or 20-year payout period if you want more money during your active "go-go" years. When you reach age 65, the sequence of withdrawals becomes critical. Typically, you'd start your CPF LIFE payouts first. Next, you supplement this with your private insurance income. Finally, you draw from your SRS or cash investments to cover any remaining "wants."

This order protects your most stable, lifelong income sources while allowing your more volatile investments extra time to grow. For a deeper look at how these pieces fit together, check out The Complete Guide to Retirement Planning in Singapore. If you're ready to build your personal pyramid, drop us a line for a tailored strategy session.

##Why Independent Advice is Crucial for Life Insurance Selection

Buying insurance from a tied agent is like visiting a car dealership that only sells one brand. You'll hear plenty of reasons why their models are the best, but you won't hear a word about the better engine or lower price across the street. In Singapore's 2026 financial landscape, this limitation can be a costly mistake. Finding the best life insurance for retirement planning Singapore offers requires a bird's eye view of the entire market, not a narrow look at a single brochure.

Your financial consultant must represent you, not the insurance company. At Zenith Wealth, through our partnership with finexis advisory, we access a vast range of insurers. This "product agnostic" approach means we aren't incentivized to push one brand over another. Instead, we focus on finding the highest yield and the most robust features for your specific situation. We compare the math, not the marketing.

The 2026 interest rate environment has made this comparison even more vital. Some insurers have adjusted their participating fund projections more aggressively than others. If you're only looking at one brand, you might miss out on a plan that offers a significantly better "guaranteed" floor. Our role is to filter through the noise and identify which plans actually deliver on their promises.

The Zenith Wealth Approach

We believe in building roadmaps, not just selling policies. Our process begins with a deep dive into your current assets and future goals. We evaluate insurer solvency and par fund strength with a critical eye. In 2026, understanding the health of an insurer's underlying investments is the only way to gauge the reliability of your future bonuses. We don't just set up your plan and disappear. Retirement is a decades-long journey, and our commitment includes regular policy reviews to ensure your coverage stays aligned with your life changes.

Secure Your 2026 Retirement Plan Today

Time is a retiree's greatest ally or their most persistent enemy. Don't wait for inflation to erode the purchasing power of your S$ savings. The earlier you secure your guaranteed income floor, the less you have to worry about market volatility or rising costs. We're here to help you conduct a comprehensive gap analysis of your current coverage and find the missing pieces in your retirement puzzle.

You deserve a plan that is as unique as your goals. Get a personalized comparison of the best life insurance for retirement planning Singapore has available today. Let's look at the data together and build a future you can look forward to. Speak with a Zenith Wealth advisor to build your custom retirement plan and take the first step toward a secure, guaranteed future!

##Take the Next Step Toward a Secure Retirement

Retirement in 2026 requires more than just passive saving. It demands a strategy that layers the stability of CPF LIFE with the flexibility of private annuities. You've seen how top providers like Singlife and NTUC Income can bridge your income gap. Now, it's time to find the specific combination that fits your lifestyle. Identifying the best life insurance for retirement planning Singapore offers is a personalized process that shouldn't be left to chance or limited by single-brand agents.

Zenith Wealth Group provides the clarity you need. As authorized representatives of finexis advisory, we give you access to over 30 insurance providers. This ensures your 2026 wealth protection strategy is built on the best available market yields. Don't let inflation dictate your future comfort. Let's build a roadmap that gives you a guaranteed income floor and total peace of mind.

Book a Comprehensive Retirement Review with Zenith Wealth Group today. We're ready to help you start this new chapter with confidence. Drop us a line!

##Frequently Asked Questions

Is private life insurance for retirement better than CPF LIFE?

They aren't competitors; they're partners. CPF LIFE provides a lifelong income floor, but its payouts are capped by the Retirement Sum. Private insurance fills the gap for higher lifestyle needs and luxury expenses. It's often the best life insurance for retirement planning Singapore residents use to fund early retirement before age 65. This layering ensures your basic needs are met while your lifestyle goals remain funded.

Can I use my SRS funds to buy any life insurance plan?

You can only use SRS funds for specific single-premium products approved by the Ministry of Finance. These are usually annuities or retirement income plans that align with the 2026 statutory retirement age of 64. Regular premium life insurance typically doesn't qualify for SRS. Using your SRS cash this way is a smart move to earn more than the 0.05% bank interest while deferring taxes.

What happens to my retirement insurance if I leave Singapore?

Most Singaporean policies remain valid even if you relocate. You can continue paying premiums and receive payouts in S$ via bank transfer to your designated account. However, you should check the tax laws of your new country, as they might tax your insurance income. It's vital to update your contact details with your insurer to ensure you receive all policy updates and payout notifications.

How much coverage do I actually need for a comfortable retirement in 2026?

Most experts suggest aiming for 70% to 80% of your pre-retirement monthly income. In 2026, with rising costs, a couple might need at least S$3,000 to S$5,000 monthly for a moderate lifestyle. Subtract your projected CPF LIFE payout from this target. The remaining balance is the amount your private insurance or investments need to cover to maintain your current standard of living.

What is the difference between an annuity and an endowment plan?

The main difference lies in the payout structure and duration. An annuity is designed to provide regular, monthly income, often for life or a long fixed term. An endowment plan is a savings-focused policy that pays a lump sum at the end of a specific period. If you want a monthly "salary" in retirement, an annuity is better. If you're saving for a specific goal, an endowment works well.

Is the payout from my life insurance policy taxable in Singapore?

Payouts from life insurance policies are generally not taxable in Singapore for individuals. This includes both the guaranteed and non-guaranteed portions of your retirement income. This tax-free status makes it a highly efficient way to build wealth compared to other taxable investment vehicles. It's one reason why many seek the best life insurance for retirement planning Singapore offers to maximize their net take-home income.

Can I change my payout start age after the policy has commenced?

This depends entirely on your specific policy's terms and conditions. Modern plans like Singlife Flexi Retirement II allow you to shift your payout age if you haven't started receiving income yet. Older or more rigid plans may not offer this option once the policy is in force. Always check the flexibility clause in your policy document before signing, as your retirement timeline might change over time.

What are "Non-Guaranteed" bonuses and how are they calculated?

These are extra payouts based on the performance of the insurer's participating fund. The insurer invests your premiums in a mix of stocks, bonds, and property. If the fund performs well, they distribute a portion of the profits to you as bonuses. These aren't certain and can fluctuate based on market conditions. Insurers use a smoothing process to keep these payments relatively stable for policyholders over the long term.