Is your savings account actually costing you money? With Thai inflation forecasted to reach 2.8% in 2026, a 0.75% return from a standard 12-month deposit at Bangkok Bank means your purchasing power is actively retreating. It's a common frustration for expats and locals alike. You want the security of a major bank like Kasikorn or SCB, but the math simply doesn't add up anymore.

We understand that moving away from traditional banks feels daunting, especially with complex tax laws and shifting regulations. This guide highlights the 7 best alternatives to fixed deposits for income in Thailand to help you secure a higher yield without unnecessary risk. We'll explore how a balanced approach, combining local stability with institutional-grade i12 investments, can transform your portfolio. Our financial planners see how moving beyond low-yield accounts creates a path to a more resilient retirement. It's time to stop settling for the bare minimum and start building a strategy that actually grows.

Key Takeaways

- Learn why traditional savings accounts are struggling to outpace 2026 inflation and how that affects your long-term purchasing power.

- Identify the top alternatives to fixed deposits for income in Thailand, including high-yield dividend stocks and national infrastructure funds.

- Discover how the i12 investments framework uses 12 distinct asset classes to create a diversified, resilient income stream.

- Understand the risk-yield spectrum to better align your asset choices with your required payout frequency.

- See how a financial consultant can navigate complex regional regulations to optimize your Thai income strategy.

Why Fixed Deposits in Thailand are Losing Their Appeal in 2026

A fixed deposit is often seen as the ultimate financial security blanket. You lock your money away for a set term, and the bank promises to return your principal plus a sliver of interest. For decades, this was the standard way to preserve wealth. However, the reality of 2026 has flipped the script. With the Bank of Thailand's policy rate holding steady at 1.00%, the "safe haven" is starting to feel more like a trap. When major commercial banks offer just 0.75% on 12-month terms, your money isn't growing; it's barely breathing.

Many savers fall into a psychological trap with Thai Baht savings accounts. It feels good to see the same number in your passbook every month. It feels safe to know the principal won't fluctuate. But "zero risk" to your principal often translates to a "guaranteed loss" in real value. Understanding Thailand's Economic Landscape is vital here. The country's major banks are currently flush with liquidity. They simply don't need your deposits to fund their operations, which keeps the rates they offer you frustratingly low.

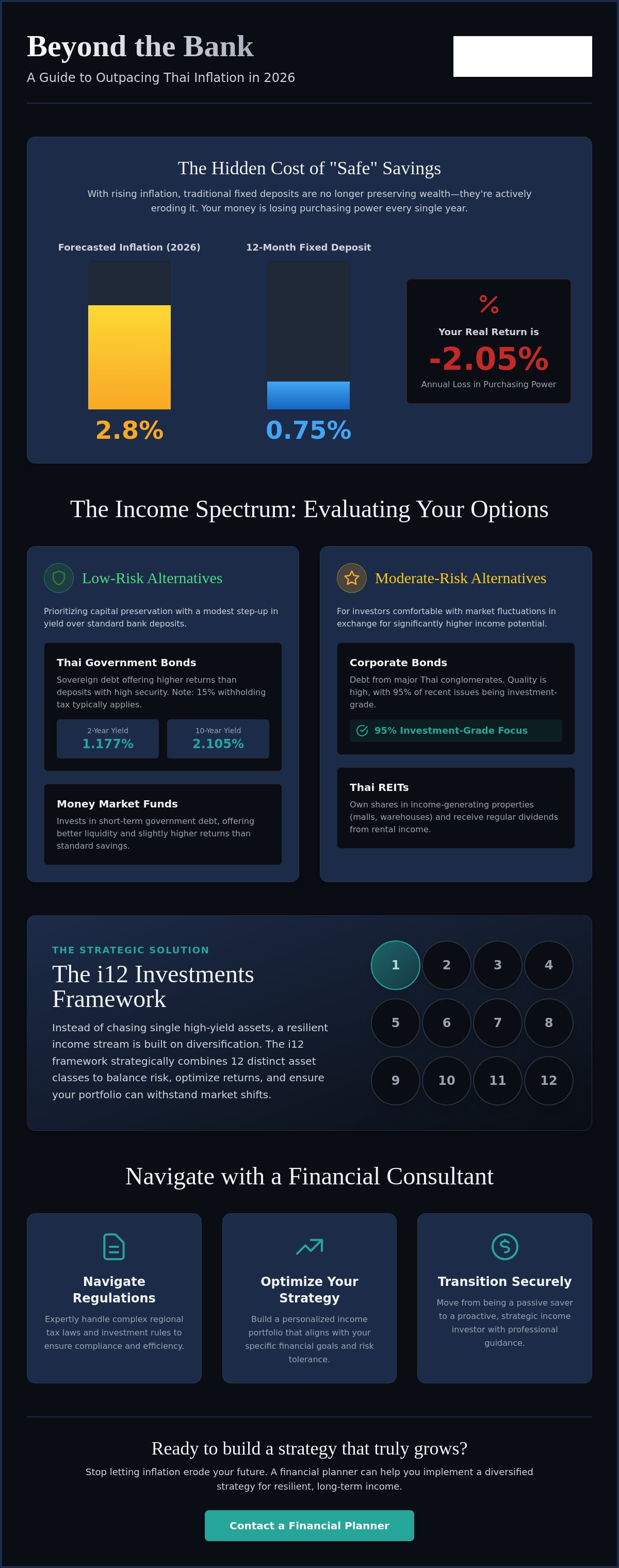

The Hidden Cost of 'Safe' Savings

Inflation is the silent thief of the Thai middle class. With headline inflation forecasted to average 2.8% in 2026, the math is brutal. If you hold 1 million THB in a fixed deposit earning 0.75%, you're effectively losing 2.05% of your purchasing power every year. Over five years, that 1 million THB will buy significantly less than it does today. Global rate shifts often pressure the Bank of Thailand, but domestic factors keep local deposit rates anchored to the floor. Your "safe" choice is actually a slow erosion of your future lifestyle.

Fixed Deposits vs. Income Investing

The year 2026 requires a proactive approach to cash management. We're seeing a massive shift from simple capital preservation to active income generation. This is where the yield gap becomes impossible to ignore. Savers are tired of watching their wealth stagnate while the cost of living in cities like Bangkok or Phuket climbs. Exploring alternatives to fixed deposits for income in Thailand is no longer a luxury for the wealthy; it's a necessity for anyone wanting to maintain their standard of living. By utilizing frameworks like i12 investments, you can begin to bridge that gap. A financial consultant can help you transition from a passive saver to a strategic investor, ensuring your capital actually works to support your goals.

The Risk-Yield Spectrum: Evaluating Your Income Options

Risk isn't a one size fits all concept. It's a spectrum where security and payout frequency often pull in opposite directions. When you look for alternatives to fixed deposits for income in Thailand, you must first distinguish between volatility and permanent loss of capital. Volatility is the price you pay for higher returns; it's the temporary up and down of market value. Permanent loss is what happens when an investment fails. Understanding this difference allows you to build a portfolio that provides consistent cash flow without keeping you awake at night.

Liquidity risk is another vital factor. How fast can you get your money back if your circumstances change? While a fixed deposit is liquid at the cost of your interest, other assets might require days or weeks to sell. For expats, currency diversification adds another layer of complexity. Earning in Thai Baht is great for local expenses, but your long term wealth protection strategy should consider how the Baht performs against your home currency. While the government offers Official Investment Incentives to attract foreign capital into the country, your personal strategy should focus on diversified cash flow.

Low-Risk: Thai Government Bonds and Money Market Funds

Sovereign debt remains the bedrock of stability. As of June 2026, a 2-year Thai government bond yields 1.177%, while the 10-year yield sits at 2.105%. These offer a clear step up from the 0.75% you'll find at major banks. Money market funds provide a similar edge, often investing in these short term government instruments to provide better liquidity than a standard deposit. Just remember that bond interest in Thailand typically carries a 15% withholding tax for individual investors, which a financial planner can help you factor into your net return calculations.

Moderate-Risk: Corporate Bonds and REITs

If you're willing to move slightly further along the spectrum, corporate debt from major Thai conglomerates offers attractive yields. In the first five months of 2026, investment-grade bonds accounted for 95% of all corporate issuances, showing a strong focus on quality. Thai Real Estate Investment Trusts (REITs) are another powerful tool. These trusts own income-generating properties like malls or warehouses and pay out a large portion of their rent as dividends. This creates a regular income stream that often exceeds inflation. The i12 investments framework is specifically designed to balance these moderate-risk assets to ensure no single market dip wipes out your gains. If you want to see how these assets fit your specific goals, you can reach out to a financial planner for a personalized review.

Top Alternatives for Passive Income in Thailand

The investment climate in Thailand is evolving as savers look for yield beyond the bank teller's window. Finding alternatives to fixed deposits for income in Thailand means looking at assets that produce cash flow regardless of the Bank of Thailand's policy rate. While many retail investors stick purely to the local stock market, a sophisticated strategy looks further. You need a mix that provides stability, growth, and regular payouts. This includes everything from infrastructure funds to regional equity income funds that balance out local market swings.

Thai Infrastructure Funds (IFFs) and REITs

Infrastructure funds (IFFs) are a standout defensive play. These funds collect revenue from essential services like power grids, toll roads, and telecommunications. It's a reliable model because people pay their utility bills even when the broader economy slows down. When you compare the yields of top tier Thai REITs against current fixed deposit rates, the difference is stark. Real Estate Investment Trusts (REITs) are a way to own property without the management headache. They offer a direct path to rental income without the need to find tenants or fix leaky roofs yourself.

Dividend Growth Investing

Dividend growth investing is another pillar of a strong income strategy. Don't just chase the highest yield you see on a screen today. Instead, select Thai companies with a 10 year history of increasing their payouts. A vital metric here is the payout ratio. It tells you if a company's dividend is sustainable or if they're paying out more than they can afford. By focusing on quality, you ensure your income grows over time. Reinvesting these dividends in the early stages can also accelerate your compounding, turning a modest portfolio into a significant income engine.

A truly resilient portfolio doesn't stop at the Thai border. Competitors often ignore the benefits of regional diversification in markets like Singapore or Malaysia. Regional equity income funds provide a necessary buffer against domestic volatility. This is a central theme within the i12 investments framework. By spreading your capital across various asset classes and geographies, you protect your lifestyle from single market risks. Working with a financial planner allows you to access these institutional grade funds and structured products like annuities. These tools provide the long term security that a simple savings account just can't match in 2026. If you want to explore these options, you can connect with a financial consultant to start your plan.

Building Your Income Portfolio with i12 Investments

Building a resilient income stream isn't about finding a single "magic" stock. It's about structure. The i12 investments framework provides this by balancing 12 distinct asset classes. This approach minimizes the risk of a single market downturn ruining your retirement plans. While we have explored individual alternatives to fixed deposits for income in Thailand, the real power lies in how these pieces fit together. Institutional-grade management offers a level of oversight that DIY investing simply can't match. It ensures your portfolio remains balanced even when global markets shift unexpectedly.

Managing 12 separate asset classes requires significant time and expertise. Most people don't want to spend their retirement staring at spreadsheets or tracking technical market indicators. A professional financial consultant takes that burden off your shoulders. They monitor the yield gaps we've discussed and adjust your holdings proactively. This strategic oversight ensures you aren't just moving money from one account to another, but actually building a system for wealth protection. It's about moving from a passive saver to a strategic owner of global assets.

Diversification Beyond the Thai Border

Relying 100% on the Thai economy is a significant risk for any retiree. Local shifts in policy or changes in regional trade can impact your domestic income. By using i12 investments, you gain exposure to more mature markets like Singapore and other global hubs. This regional diversification acts as a shield against Thai Baht currency fluctuations. If the Baht weakens against global benchmarks, your international holdings provide a necessary buffer. It's about creating a global income stream that supports your lifestyle in Thailand regardless of local economic cycles.

Strategic Wealth Analysis

A customized roadmap is always better than a "hot tip" or a single product. Your income needs depend entirely on your specific life stage. A pre-retiree focused on aggressive growth has different requirements than a retiree needing immediate, monthly cash flow. This is where a financial planner adds the most value. They align your assets with your personal timeline and risk tolerance. You can dive deeper into this approach by reading our guide on Strategic Investment Management. Ready to see how this framework fits your specific goals? You can start a conversation with our team today to build your personalized plan.

How a Financial Consultant Optimizes Your Thai Income Strategy

Many investors believe they can manage a few bonds or stocks alone. However, creating a sustainable income engine requires more than just picking products. A professional financial consultant plays a critical role in navigating the shifting regulatory environment of 2026. Whether it's staying ahead of updates to the Foreign Business Act or managing the new quarterly reporting for BOI-promoted companies, having an expert eye ensures your strategy remains compliant. This professional oversight is what makes alternatives to fixed deposits for income in Thailand truly effective and sustainable over the long term.

One of the greatest benefits of professional advice is emotional stability. Markets fluctuate; it's their nature. When prices dip, the urge to sell can be overwhelming. A financial planner acts as a steady hand, preventing reactionary decisions that could derail your retirement. They handle the regular portfolio servicing and rebalancing necessary to keep your i12 investments aligned with your specific risk profile. This proactive management also reduces the friction often found when moving wealth between Thailand and Singapore. We ensure your capital is positioned in the most efficient jurisdiction to capture yield while maintaining accessibility.

Tailored Solutions for Expats and Locals

Tax efficiency is a major concern for anyone generating income outside of Thailand. A financial planner helps you structure your holdings to minimize unnecessary leaks from withholding taxes or cross-border transfers. This isn't just about today's income; it's about your family's future. We integrate your Thai-based assets into a broader strategy for Legacy Planning. This ensures your wealth protection efforts benefit the next generation without being tied up in complex probate. Think of us as your Modern Professional Guide. We prioritize human interaction and clear communication over institutional coldness.

Next Steps: Securing Your Future

The biggest risk in 2026 isn't market volatility; it's the cost of waiting. Inflation doesn't pause while you decide on a strategy. Diversifying your income now protects your purchasing power for the decades ahead. To prepare for a consultation, start by gathering your current asset statements and defining your monthly income goals. Do you need immediate cash flow, or are you building for a date five years away? Having these answers ready allows us to hit the ground running. If you're ready to move beyond fixed deposits, contact a financial consultant today. We're eager to start the conversation and grow alongside you.

Take Control of Your Financial Future

The days of relying on a simple bank book for growth are over. In 2026, protecting your purchasing power requires a shift from passive saving to strategic investing. By exploring alternatives to fixed deposits for income in Thailand, you've already taken the first step toward a more resilient retirement. You now understand how to balance local infrastructure yields with global stability through the i12 investments framework. It's about ensuring your capital works as hard as you did to earn it.

Navigating cross-border regulations and regional tax laws doesn't have to be a solo journey. As an authorized representative of finexis advisory Pte Ltd, we specialize in cross-border retirement planning across the SE Asia region. Our team provides the professional oversight needed to manage complex portfolios with quiet confidence. We're ready to help you bridge the gap between stagnant bank rates and institutional-grade income. Schedule a consultation with a Zenith Wealth financial consultant today to begin your journey. We look forward to growing alongside you.

Frequently Asked Questions

Are alternatives to fixed deposits in Thailand safe?

Safety isn't an all-or-nothing concept; it's a spectrum. While government bonds offer sovereign security, other alternatives to fixed deposits for income in Thailand like investment-grade corporate bonds provide a higher yield with manageable risk. The real safety comes from the i12 investments framework, which spreads your capital across multiple asset classes. This structure ensures that your portfolio isn't overly dependent on any single bank or economic sector.

How much tax do I pay on investment income in Thailand?

Individual investors typically face a 15% withholding tax on interest and a 10% tax on dividends in Thailand. These are generally considered final taxes, so you don't always need to include them in your personal income tax return. However, navigating tax efficiency for regional or global income requires specialized knowledge. A financial planner can help you understand how these costs impact your net returns and help you plan accordingly.

Can I invest in Singaporean assets while living in Thailand?

You can certainly invest in Singaporean assets while residing in Thailand. Singapore provides a stable, highly regulated environment for wealth management that many expats and locals find attractive. By including regional assets in your strategy, you gain access to institutional-grade products that offer a buffer against local market volatility. This is a key component of the i12 investments approach, helping you build a truly diversified and resilient income stream.

What is the minimum amount needed to start an i12 investments portfolio?

Minimum investment levels depend on your specific goals and the asset classes selected for your strategy. We don't use a one-size-fits-all approach because every client's income needs are unique. Instead, we focus on creating a customized roadmap through our investment management services. A financial consultant can evaluate your current assets and help you determine the most efficient way to begin transitioning your wealth into more productive income-generating assets.

How do Thai REITs compare to owning physical rental property?

Thai REITs offer a liquid and professional way to earn rental income without the headaches of physical property management. You don't have to worry about finding tenants, fixing leaks, or paying property taxes on individual units. REITs also allow you to own a piece of high-quality commercial real estate that would be impossible to buy alone. They provide a transparent, monthly or quarterly income stream that is often more predictable than individual rentals.

Is it better to keep my savings in THB or USD for income?

The ideal currency balance depends on your long-term spending plans. If you live in Thailand, you need THB for daily expenses, but holding USD or SGD offers a vital hedge against local currency fluctuations. Most investors find that a mix of currencies provides the best protection for their purchasing power. A financial planner can help you determine the right ratio to ensure your income remains stable regardless of how the Baht performs.

How often should I review my income portfolio with a financial planner?

We recommend a formal review at least once a year. Regular check-ins allow us to rebalance your portfolio and ensure your asset allocation still aligns with your life stage. If you experience a major life event, like a business succession or a change in retirement plans, you should reach out sooner. These sessions are vital for maintaining the health of your alternatives to fixed deposits for income in Thailand and adjusting to new market opportunities.

What happens if the Thai Baht devalues against the Singapore Dollar?

If the Thai Baht devalues, the value of your Singapore Dollar holdings will increase when measured in Baht. This currency gain helps protect your purchasing power against the rising cost of imported goods or travel. Regional diversification is a core part of our wealth protection strategy. It ensures that your lifestyle in Thailand isn't compromised by local economic shifts. By holding assets in stronger regional currencies, you create a more stable financial foundation.